The payroll report for the final month of 2025 stayed true to form, with the data all pointing in different directions. The big picture remains the same — a lot of people are working, but hiring is weak for a few reasons. Employers across industries appear reluctant to hire amid economic uncertainty and policy headwinds, and the workforce is also shrinking because of a collapse in immigration (so there are fewer people to hire).

The economy created 50,000 jobs in December, below expectations for a 70,000 increase. Moreover, October payrolls were revised down by 68,000, from -105,000 to -173,000, and the change for November was revised down by 8,000, from +64,000 to +56,000. That’s a combined downward revision of 76,000 over two months. That’s not good.

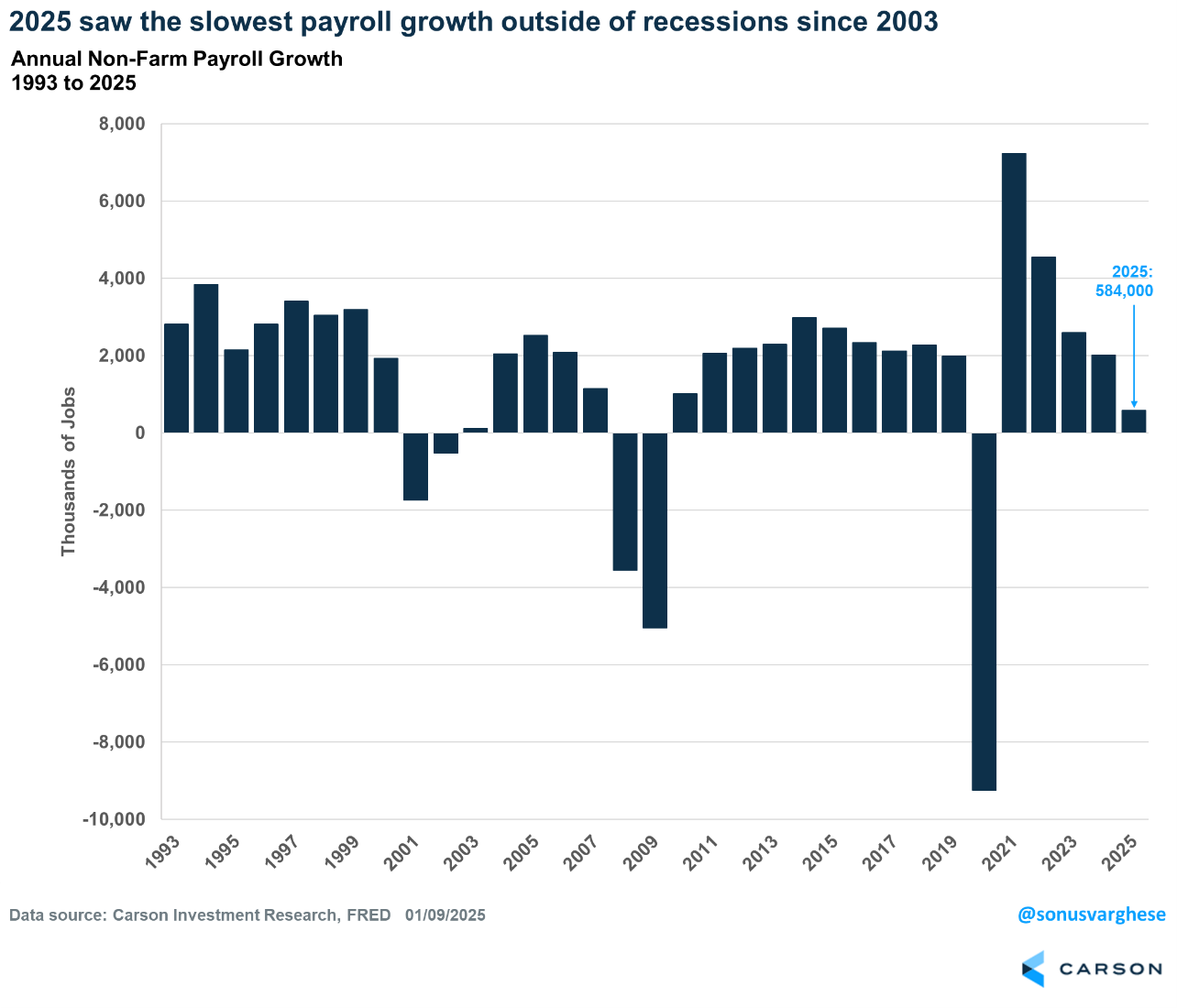

The economy created 584,000 jobs in 2025, the worst year outside of recessions (2008, 2020) since 2003. That’s a sharp slowdown from the last two years. Payrolls grew just 0.4% in 2025, versus 1.3% in 2024 and 1.7% in 2023. The pace was 1.4% in 2018–2019, another recent period when the job market was growing a solid pace (other than 2021–2024).

As you can see below, the real weakness has come after April (and Liberation Day) — payroll growth averaged just 12,000 per month over the last 8 months of 2025. Over the prior 12 months (May ’24 – Apr ’25), payroll growth averaged 150,000 (this will be revised lower, but it’ll still be several times higher than recent months).

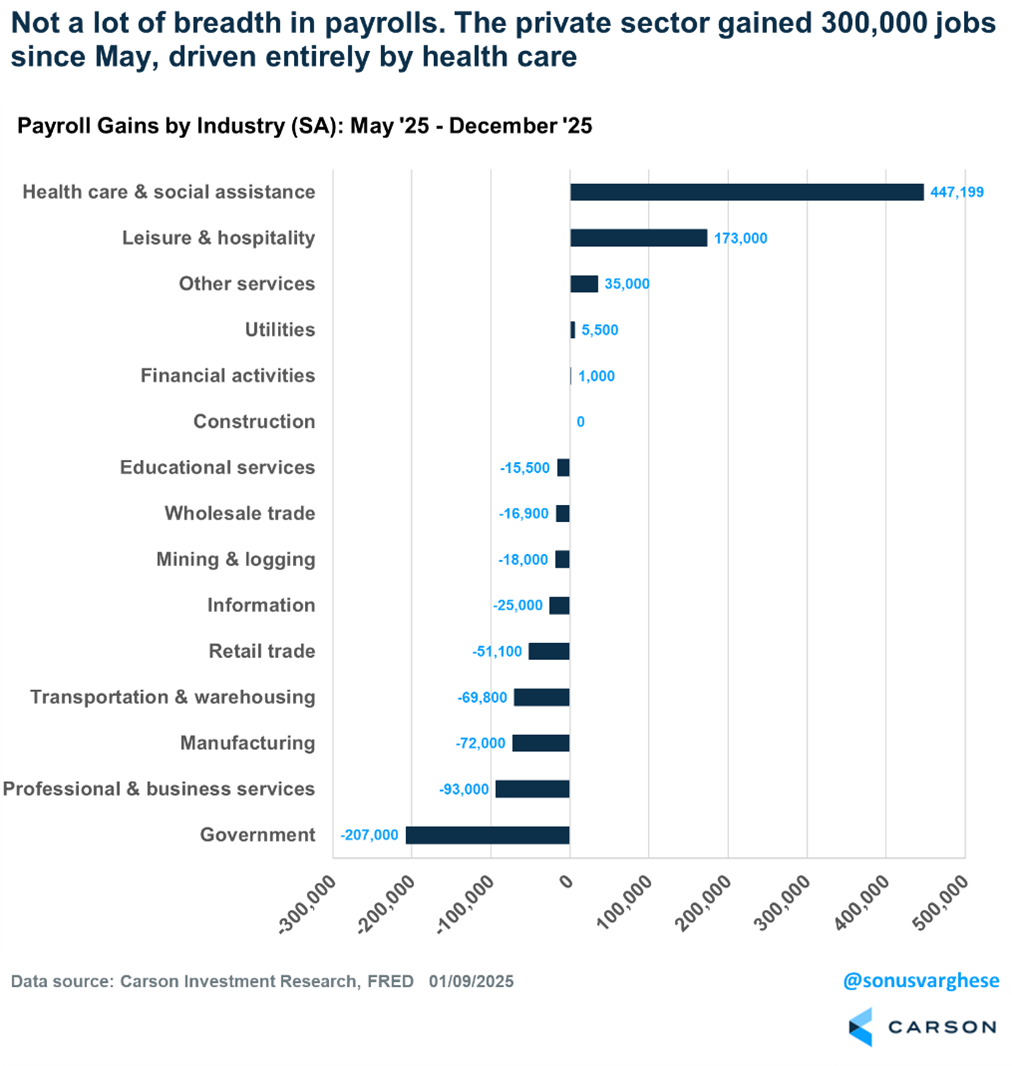

Note that the big drop in October was due to a 174,000 fall in federal jobs (as deferred layoffs took place), but even private payrolls rose by just 1,000 that month (not a typo!). Looking at the May – December period, the private sector added just 300,000 over this period (averaging just 38,000 per month), but as you can see below, it was driven almost entirely by a gain of 447,000 jobs in the health care industry. Leisure and hospitality, a cyclical area of the market, did gain 173,000 jobs, but a lot of other cyclical areas struggled. Manufacturing lost 72,000 jobs, retail another 51,000, and construction was flat.

There’s Good News Too

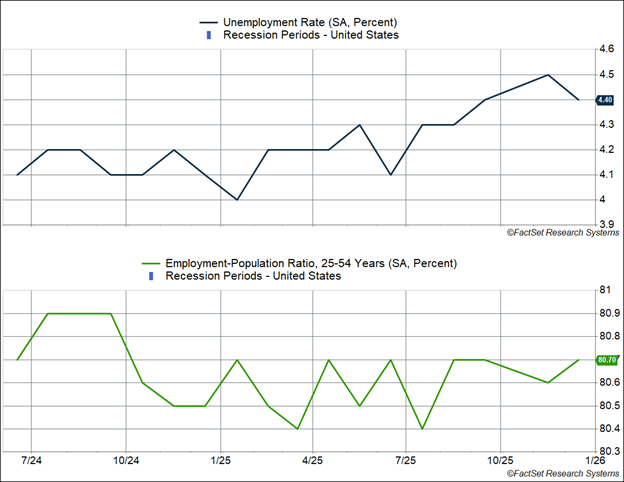

The good news is that a key barometer for the labor market, the unemployment rate, went the other way. The unemployment rate fell from 4.6% to 4.4%, which is a historically low level. The unemployment rate did increase from 4.1% to 4.4% over the course of 2025, but that’s not bad considering how weak payroll growth was. The fact that the unemployment rate didn’t rise even further tells you that the workforce has shrunk, amid a big pullback in immigration — the economy didn’t create a lot of jobs, but it created just about enough jobs to keep up with population growth, which is why the unemployment rate didn’t rise even more.

In fact, the prime-age (25–54) employment-population ratio ended the year at 80.7%, near the highs we’ve seen this cycle and higher than at any point from 2002–2019. Prime-age workers are as close to full employment as we’ve seen over the past two decades.

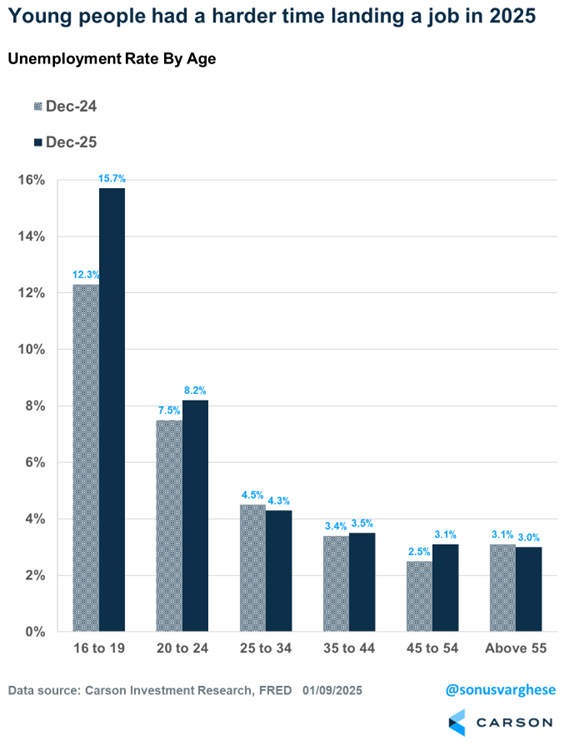

The higher participation rate for prime-age workers also underlines what happened in 2025: it was a tough year for young workers, especially those looking for new jobs.

- The unemployment rate for 16–19 year olds rose from 12.3% to 15.7%.

- For 20–24 year olds, it rose from 7.5% to 8.2%

But every other age group didn’t see significant increases. In fact, the unemployment rate for the oldest cohort of workers (55+) fell from 3.1% in 2024 to 3.0% in 2025. Note that this data can be quite noisy but the trend is clear.

This also gets to another related phenomena that happened in 2025. Despite weak hiring, output held steady. Real GDP growth across the first three quarters rose at an annualized pace of 2.3%, which is not far from the 2010-2019 trend (though lower than the near 3% pace in 2023-2024). That’s a strong sign of productivity growth (producing the same amount of goods and services with fewer people).

Productivity growth clocked in at an annualized pace of 2.3% in 2025. It continues the positive productivity growth story from 2023-2024 (2.7% average), and over the last three years, productivity growth has run at an average of 2.5%. That’s well above the 2005-2022 pace of 1.5% and is reminiscent of the above-average productivity growth from 1996-2004 (though that was higher still, averaging 3.1%).

It’s easy to attribute this to gains from artificial intelligence (AI), but while that could be a story for 2025, it wasn’t the case in 2023 and 2024, when productivity growth was even higher. Instead, the productivity gains are probably related to the dynamics we’re seeing in the labor market.

Companies likely over-hired workers in the 2021-2023 period and have now curbed hiring, especially in 2025, amid economic uncertainty and policy headwinds (like tariffs). Many firms cut costs by curbing their workforce by attrition by not replacing workers who left their jobs. This by itself leaves the existing workforce much more experienced, and productive (since new hires take a while to get up to speed, and that’s a “cost,” at least temporarily). It also explains how firms continued to expand margins in 2025, in addition to raising prices even more than their input prices went up (which is why inflation remained elevated). Note that margin expansion also boosted the stock market last year.

But there’s a problem at the aggregate level, even if not for individual companies. Companies can squeeze workers only so much. At some point they have to pay higher wages and hire more workers. Historically productivity growth is accompanied by strong real wage growth for workers (wages adjusted for inflation) — this happened in the late 1990s and even 2023-2024. But 2025 was odd because we got strong productivity growth and weak real wage growth (nominal wage growth eased and elevated inflation took a big bite out of it). That can continue for only so long. Weak real wage growth can ultimately lead to weaker consumption and that’ll drive revenues and profits lower. Instead, I think we’ll see a pickup in both activity and hiring as 2026 gets underway (rather than a drop in consumption and a much weaker economy).

Brace for a long pause?

We may have just seen the last cut by a Powell-led Federal Reserve, back in December. A labor market that looks less shaky, especially with an unemployment rate that is historically low and strong participation (at least for prime-age workers), is not one that is likely to push Fed members to advocate for more cuts in the immediate future. In their summary of economic projections from December, the median Fed member expected the unemployment rate to end up at 4.5%. It ended the year at 4.4% (which is their projection for 2026).

Still, as I discussed above, the labor market is not sending an “all is well” signal. Moreover, President Trump is likely to continue pushing for more cuts, which means he’ll nominate a new Fed chair (Powell’s term ends in May) that is in favor of rate cuts, a lot of them. Of course, the Fed Chair is just one vote of 12 on the committee and so there’s likely to be a tug of war between a dovish faction and a hawkish faction after May.

Markets still expect two more rate cuts in 2025, taking the Fed policy rate to the 3.00-3.25% range, but the first cut is expected only after May. That’s our base case as well, with a Fed that eventually tilts toward the dovish side.

We wrote about this in our just released 2026 Market Outlook: Riding the Wave. Give it a read to see how we expect the economy, policy, and markets to evolve the rest of this year. (here’s the link).

Ryan and I also discussed it on our latest Facts vs Feelings episode.

For more content by Sonu Varghese, VP, Global Macro Strategist click here

8703235.1.-09JAN26A