What may seem like a singular holding in your portfolio may be held twice, three times, or more unintentionally.

In portfolio construction today, allocations are becoming more prevalent to feature ETFs, rather than simply relying on single stock choices. Not only is the usage of ETFs growing, but they are constantly being created by asset management companies and investment firms who are bundling and repackaging new products that often have a significant overlap with what is already currently on the market. In these new products, as well as what are the cornerstones of the ETF markets that track their respective indexes, more options do not always mean more diversification. True diversification is susceptible to becoming diluted and may not be as effective as one intends to create, which demands that the importance of minimizing concentration risk is reaffirmed to hedge the vulnerabilities to this risk that we are exposed to.

It seems simple, but a different name on a security highlighting a different sector or index that is being tracked would presumably lead an investor to perceive this investment to be substantially different than the other investments they may already hold. The underlying holdings of an ETF may be an afterthought for an investor after simply looking at the fund names, but they may not be what you expect them to be. A great example of this was detailed by Blake Anderson on our team, who showed that the State Street Financial Select ETF (XLF) does not solely align with traditional banking activity and has added allocations that have heavy tech influence since 2023. If you did not look at the underlying holdings of XLF prior to your investment and thought you would only be gaining diversification to the financial sector, that line of thinking would not be fully accurate. This concept is not unique to XLF, but a more relevant example to the investor in the current market is the overlapping holdings they are experiencing between ETFs that they choose to target varying sectors, indices, and thematic goals in their portfolio to achieve diversification.

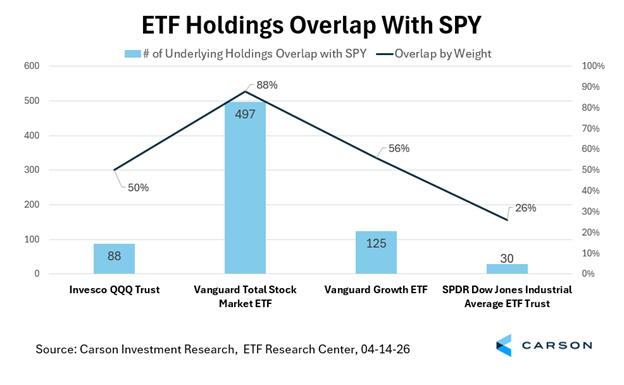

When there is unintentional overlap between indices in holdings, there is increased portfolio volatility (since the same market movement may impact both funds) and minimized diversification. As shown below, the chart illustrates how common index ETFs measure in the number of overlapping holdings as well as the allocation weight of those holdings compared to the most common index tracked in portfolios, the S&P 500, which can be best analyzed from an ETF standpoint via the ticker symbol SPY.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

If you were to choose to purchase an additional ETF for varying exposure in addition to your holding in SPY, there is a possibility that your money could be directed in the same way between both funds if you selected one with overlap. Looking at the chart above, if you were looking to add a holding that tracked the Nasdaq and did so via QQQ, you would have 88 holdings that overlap between SPY and QQQ, with 50% overlapping by weight between the funds. When comparing a new prospective purchase to your current ETF holding, overlapping weight is a critical metric and one that should be treated with more consideration over the raw number of shared holdings. High-weighted overlap adds unnecessary complexity and results in unintentional overallocation in holdings you technically already possess.

A major trait between index tracking ETFs that causes this weighted overlap is the Mag 7 holdings that are consistent between varying indexes and ETFs. Currently, the S&P 500 derives roughly 35% of its weighted makeup from the Mag 7 positions, additionally the Nasdaq receives an even higher influence from the Mag 7 with a weighted contribution of roughly 65%. Zooming in on the Mag 7 specifically, you realize that you are becoming more concentrated in those holdings if you were to passively purchase ETFs tracking these indices. This risk can compound and become an even greater issue if your portfolio already has a concentrated single Mag 7 stock position, which can induce greater concentration risk if you continue to purchase index ETFs without fully accounting for the exposure you are taking on.

In an investing landscape that is continually having new ETFs and products added for investors to choose from, to achieve true exposure diversification, selected allocations need to be intentional. If ETFs are passively chosen, without the underlying holdings being reviewed, the desired diversification you sought to achieve will be forfeited. Understanding the makeup of what you are purchasing and adding to your portfolio seems like a “no-brainer”, but with the constant repackaging and bundling of the same securities, most of which are the Mag 7, it is even more prevalent to minimize your portfolio’s concentration risk and be cognizant of the holdings you are taking on.

By Joel Riha-Aldrich, Analyst, Investment Research

8895376.1. – 24APR26A