As Barry wrote about yesterday, bonds have had a volatile year so far, and the payoff for the volatility we have seen is a barely positive return for the year for the aggregate bond market, including interest. Rates have moved higher across the yield curve, credit spreads have widened slightly, and bonds fell alongside equities during the early year swoon. Let’s dive into each of these observations and see what it means for bond investors going forward.

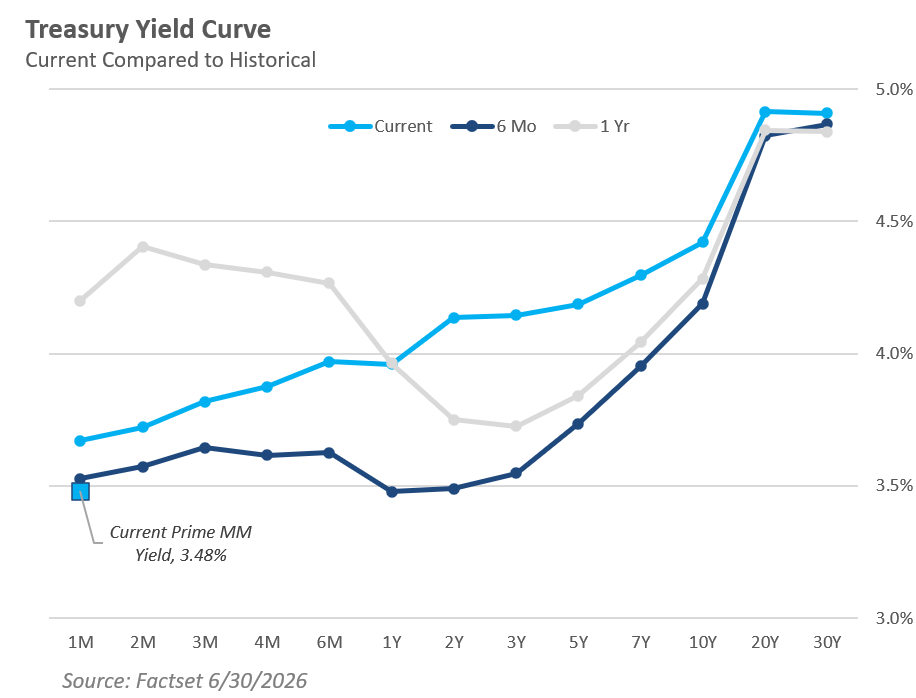

One. The Yield Curve Is Closer to “Normal”

Yields have shifted higher across the curve so far this year, as the short end has readjusted to the prospect of no interest rate cuts (and potentially even hikes), and the long end of the curve is reflecting a still worsening national debt outlook. Still sticky (and even accelerating) inflation in some areas has also pushed the entire curve higher. While this has hurt (or at least not necessarily helped) bond investors this year, it has shifted the yield curve closer to a traditional “normal” shape – one where investors are compensated more for taking on interest rate and inflation risk. Even as recently as the beginning of the year, the curve had a flat to even slightly inverted portion inside of five years. A year ago, this was even more pronounced, when an investor in a 3-year Treasury was compensated significantly less than T-bill investors lending the government money for tenors less than a year.

A more normal yield curve is beneficial in a couple of ways. First, a steeper yield curve results in a “roll down” effect, where bond investors benefit from higher long-term rates. As those bonds get closer to maturity, the market calls for a lower interest rate – resulting in capital gains for the investor as the bond rolls down. Second, it creates more dispersion across duration levels (duration is a measure of interest rate risk), in particular in the short-term space. Current prime (which has credit risk) money market fund yields are nearly 0.50% below those of 1-year Treasuries. Investing in the ultra-short (<1 year) and short-term (1-3 year) bond space – or at least utilizing funds able to take advantage of this opportunity set – can yield strong results. Hint: we have strategies in these areas.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

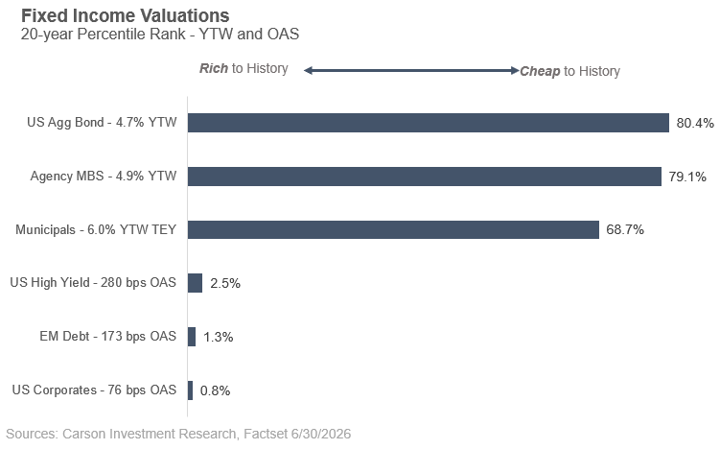

Two. Credit Is Still Expensive

A quick look at fixed income valuations, using both spreads and absolute yields where spreads are less applicable, shows a similar story to what we’ve seen in recent time periods. High-quality bonds remain attractively valued relative to their history, while credit spreads are still very tight despite widening this year. While credit spreads remain tight, this also highlights continued demand based on solid fundamentals, low default rates, and economic resiliency. Absolute yields remain relatively high across high-quality and credit asset classes given they are priced off the aforementioned Treasury curve. This yield advantage delivers better income than in the past, and also helps cushion against interest rate changes. Using selective active management can potentially be an effective way to manage credit risk.

Three. Bonds Diversify…When Inflation Isn’t a Concern

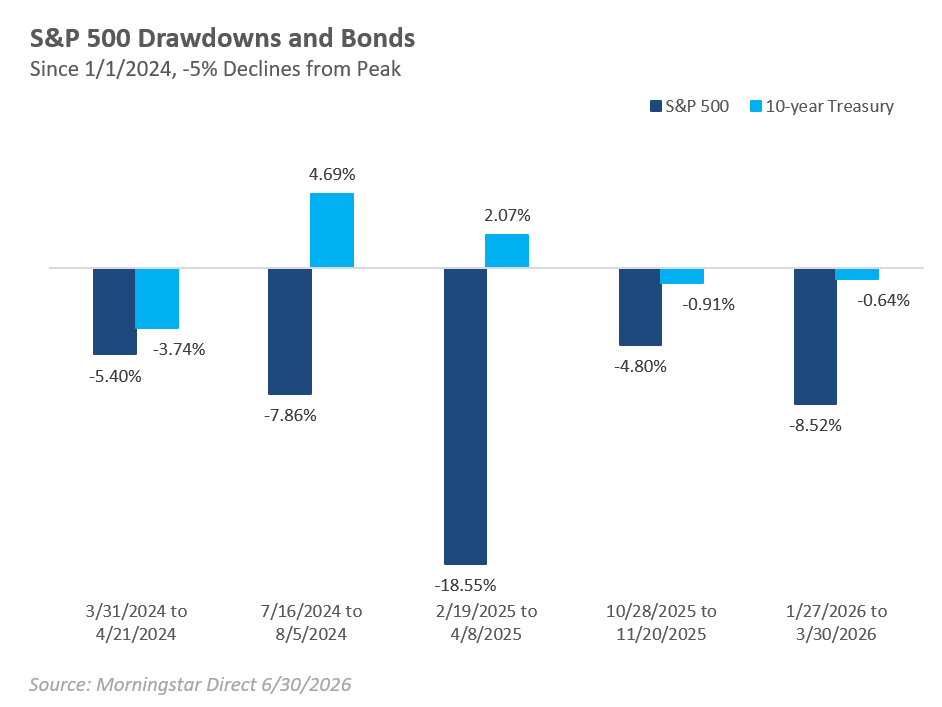

Bonds provide income, with starting yields being the consistent driver of returns over time. Bonds can also serve as a ballast in portfolios, if they maintain a low correlation to stocks. Over the past two years, the jury is still out on how consistent this has been. Looking at the most recent S&P 500 drawdowns of at least -5%, bonds (as measured by the 10-year Treasury total return) were positive during two of those periods, which also happened to be two of the steepest declines. In other drawdowns, all else equal, bonds fell alongside stocks, and in each of these periods there was a corresponding inflationary concern that hit bonds (tariffs, oil prices, Iran, etc).

This keeps us interested in non-bond diversifiers, particularly those that can react positively to inflation shocks.

\

\Taken together, there has been no shortage of excitement in the (public!) fixed income space this year. Allocating to fixed income today requires a thoughtful approach and proper portfolio construction to both take advantage of opportunities while also building resilience.

For more content by Grant Engelbart, VP, Investment Strategy & Research, click here.

9002605.1. – 7JULY26A