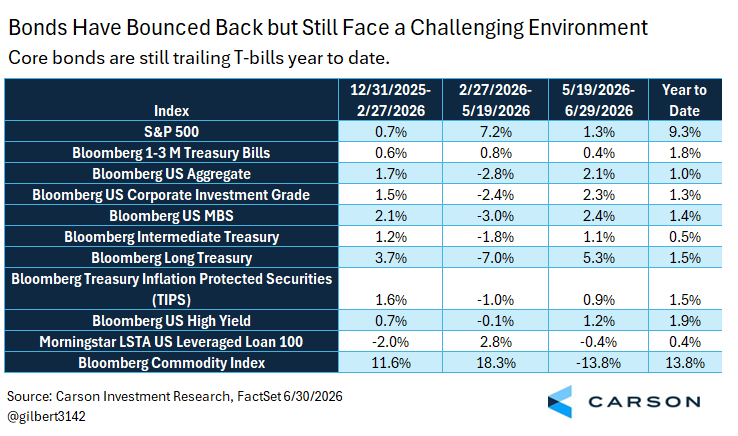

Bonds have made a modest comeback lately as rates have retreated amid slow progress in negotiations with Iran and the start of some movement through the Strait of Hormuz. The 10-year Treasury yield peaked at 4.66% on May 19 and now sits at 4.37%, not far off from the median of 4.29% since the start of 2025. That move has helped the Bloomberg US Aggregate Bond Index (“Agg”) move from a year-to-date return of -1.06% on May 19 to +1.03% as of yesterday’s close. But you would still have done better if you had just been in ultra-short Treasuries. The Bloomberg 1-3 Month US Treasury Bill Index is +1.80% year to date, with much less volatility than core bonds. But that fits with our forecast in our 2026 Outlook that cash would do a little better than bonds this year.

Bonds have really been a story of three phases this year, all within an overall context of rising rates: before the Iran conflict (start of year through February 27); the conflict and continued heightened tensions (February 27 to May 19); and negotiations and preliminary détente (May 19 to present). The three periods saw rates fall, rise, and then fall again, with a net move higher. Despite a higher 10-year yield year to date, major bond sectors have seen advances as strong starting yields have compensated for rate-influenced price declines. We aren’t in the world of ultra-low rates anymore, where yields provide no cushion.

We did tactically shift meaningful cash exposure to bonds in mid-May just before yields hit their peak. Of course, a large part of timing like that is luck. The actual declines were aligned with our reason for making the change, but we expected it to be a thesis that would play out over time, not one that would time the bond bottom within a few days. That said, our basic orientation on bonds hasn’t changed. We still have a decided preference for equities. The yield advantage of bonds over cash makes it more attractive from a strategic perspective, but there are more ups and downs to tolerate. Tactically, if bonds get far enough ahead of cash, we could very well shift some bonds back to cash. While reducing our cash allocation, we remain somewhat defensive on rates, continuing to place a strong emphasis on bonds with lower rate sensitivity, including some floating-rate debt. Beyond interest rate positioning, we are also still committed to looking for equity diversifiers beyond the bond space, holding some exposure to natural resources, managed futures (a trend following strategy that can have long or short exposure to multiple asset classes), and even lower volatility equities.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Big picture, our outlook for rates remains fundamentally tied to our forecast for inflationary growth, with the Fed allowing the economy to run hot relative to inflation. That means when the cycle eventually ends, we believe the more likely path to a recession will be a Fed forced to raise rates aggressively to control inflation before cutting. The less likely alternative, in our view, would be an immediate shock that would send the economy into a disinflationary recession with no intermediary stage of aggressive rate hikes. In our view, the current economy remains resilient to shocks that could lead to a disinflationary recession; it has already avoided a recession during three major shocks, none of which we thought would lead to a downturn despite many forecasts to the contrary. Those three shocks were the most aggressive rate-hiking campaign in decades in 2022–2023, the tariff shock, and the Iran War shock. The economy has become somewhat less resilient over time, but strong corporate and household balance sheets, deficit-financed stimulus, a steadying job market, and tremendous capex spending on artificial intelligence still leave plenty of cushion. That doesn’t mean the economy can overcome any shock, but it has proved itself able to absorb some fairly large ones so far.

For more content by Barry Gilbert, VP, Asset Allocation Strategist, click here.

9001180.1. – 30JUNE26A