It’s not surprising that consumer sentiment has plunged over the last two months amid all the market volatility, and headlines around tariffs and layoffs (even beyond the federal government). Two popular surveys of consumer sentiment, from the University of Michigan and The Conference Board, have seen sentiment more than reverse all the gains made in the second half of 2024. As you can see in the chart below, the University of Michigan Index (dark blue line) is well below where it was amid Covid, and close to where it was back in 2008. It’s now as low as it was in 2022, when we had 40+ year highs in inflation, and the message here may be that households hate inflation, and the prospect of it. The Conference Board survey looks better in comparison (green line), and it tends to be more in tune with the labor market. Still, it’s well below where it was pre-pandemic, and the recent pullback suggests Americans are also worried about the job market.

Consumers Expect Stagflation

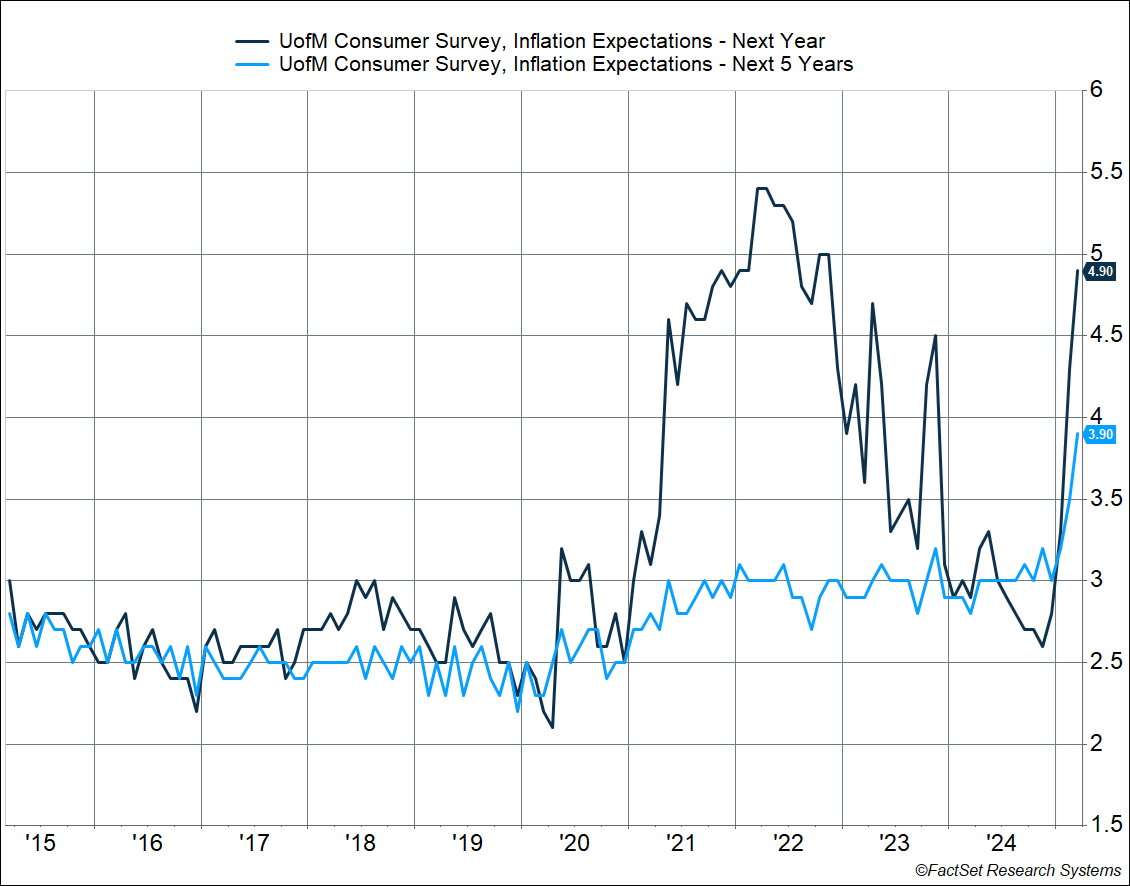

The dreaded notion of stagflation is in the air now. It is the economic environment when inflation and unemployment are high, similar to the 1970s (usually when one is high the other is low). Today’s it’s often more loosely used just to mean both inflation and unemployment are rising, but that’s incorrect and certainly not the same as what we had in the 1970s. The University of Michigan Survey saw an alarming surge in inflation expectations recently, with 1-year ahead expectations jumping to 4.9% and 5-year ahead expectations to 3.9%. 5-year ahead expectations typically should be more stable, but this is the higher than anything we’ve seen over the past decade, including in 2022 when inflation was actually running really hot. The increase in March was the largest month-over-month increase seen since 1993.

The increase in inflation expectations would typically be very concerning for the Federal Reserve, but other surveys don’t show a similar surge, including the New York Federal Reserve’s consumer survey and the Atlanta Fed’s business expectations survey—a big reason why Fed Chair Jerome Powell was quick to dismiss concerns about rising inflation expectations. The University of Michigan survey is also colored by politics:

- Democrats expect 1-year ahead inflation to be 6.5% and 5-year ahead inflation to be 4.6% (up from 2.7% pre-election).

- Republicans expect inflation to be non-existent, with 1-year ahead inflation at 0.1% and 5-year ahead inflation at 1.3% (down from 3.4% pre-election).

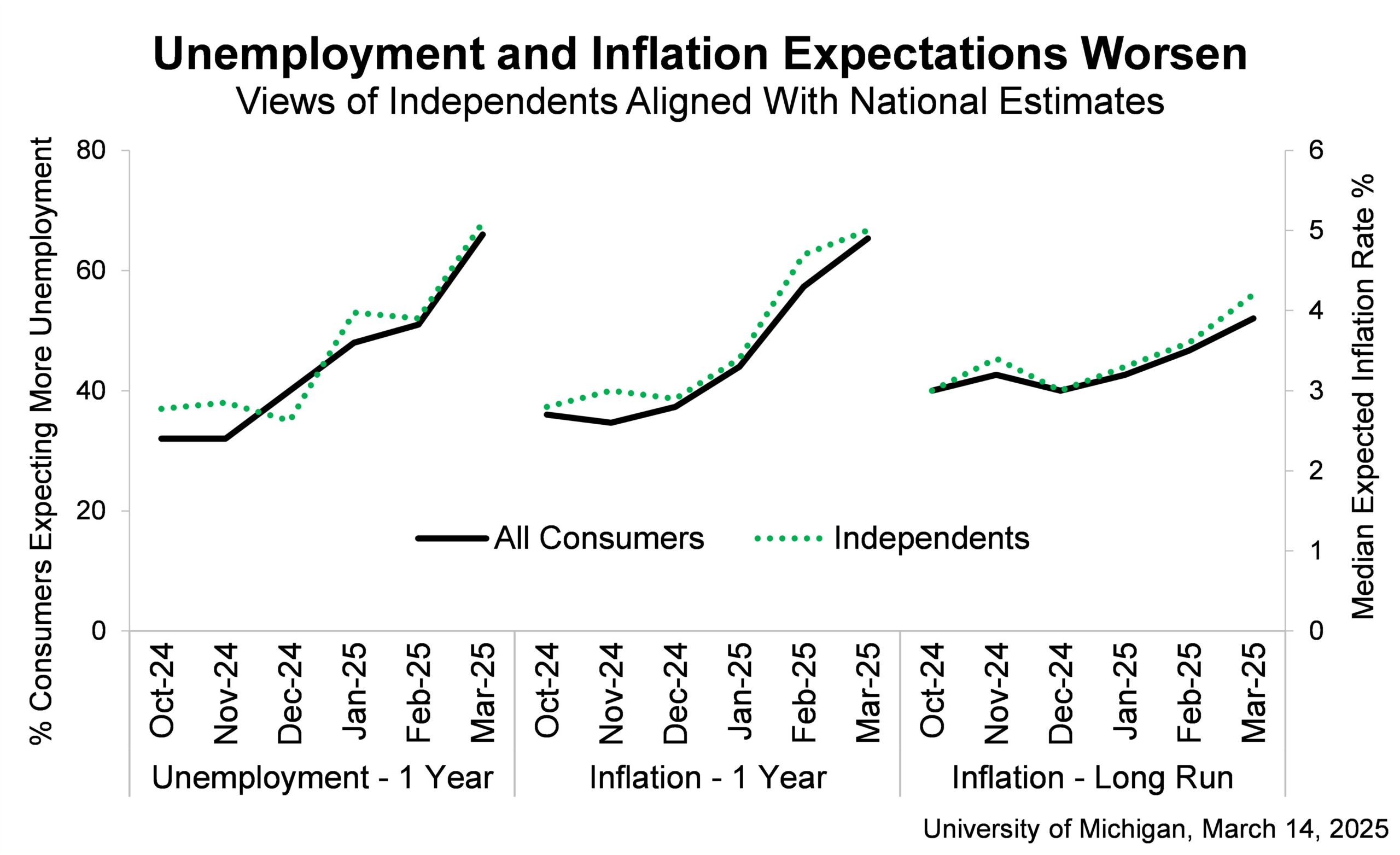

Beyond inflation expectations, consumer sentiment on the labor market also took a big dive in March. Our friend Neil Dutta at Renaissance Macro Research shared this chart, showing that the expectations about unemployment plunged to its lowest level since 2008. This typically tends to be correlated with payroll growth, and so the plunge is certainly alarming. Again, there’s probably an issue of this being colored by politics as well.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

There may actually be more signal if you just follow independents, but even there the numbers moved in a stagflationary direction. Amongst independents, 1-year ahead inflation expectations are at 4.4% and 5-year ahead expectations at 3.7%. And close to 70% of them expect unemployment to rise.

Folks, We Are Far from Stagflation

Let’s start with the inflation picture. Anytime the specter of stagflation comes up, or even a surge in inflation, there are a couple of key things I look at: oil prices and wage growth. Energy price shocks (like in the 1970s, or even in 2022) tend to drive upside inflation shocks and right now, we don’t have anything close to that. Oil prices are hovering at the bottom end of their 4-year range, with WTI crude oil prices near $67/barrel. That’s not what you’d expect to see if we were anywhere close to stagflation right now. Granted, energy price shocks are exactly that, a shock or surprise. But with crude oil production in the US running near record highs and OPEC doing away with production cuts, there’re no signs of an imminent supply reduction.

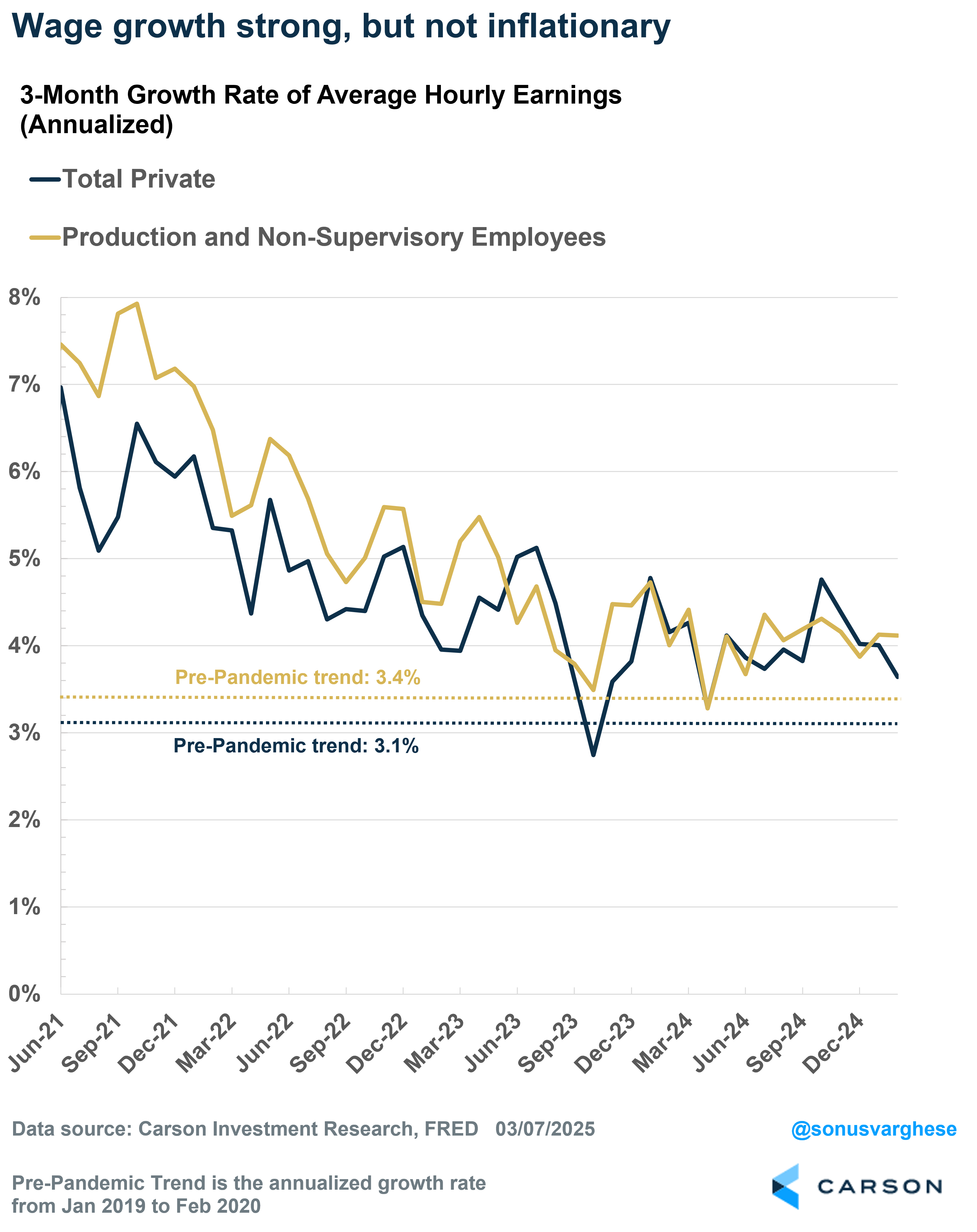

The other thing with a stagflationary scenario is that we’d expect to see wage growth running much hotter than it is. Instead, the latest payroll report showed wage growth running close to the pre-pandemic trend. Over the last three months

- All private workers: +3.6% annualized versus pre-pandemic trend of 3.1%

- Non-managers: +4.1% annualized versus pre-pandemic trend of 3.4%

Forget stagflationary levels of inflation, this pace of wage growth is consistent with 2% inflation. There’s a reason why Powell said that the labor market was not a source of inflationary pressure.

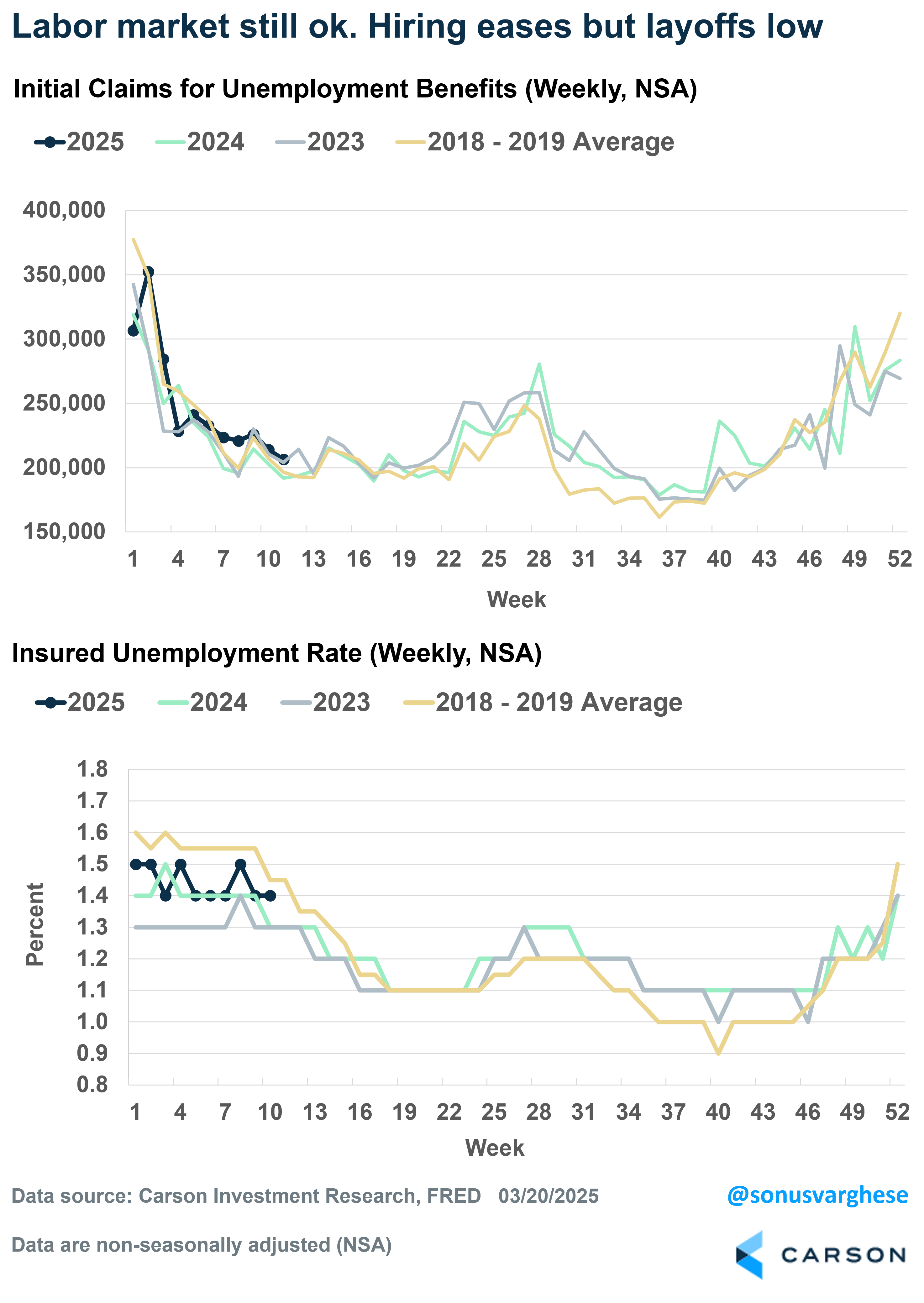

On the employment side, the labor market is still looking fairly healthy. The unemployment rate is at 4.1%, which is near historical lows. Now, the hiring rate is running near levels we last saw in 2013 (not exactly weak, but not perfectly strong either). But the unemployment rate is as low as it is because layoffs are running low. Overall layoffs are running lower than where they were before the pandemic, and even if you normalize for the large workforce we have now, the “layoff rate” is 1%, below the 1.2-1.3% range we saw prior to the pandemic (which was already on the lower side). More timely data, like initial claims for unemployment, also indicate no surge in layoffs. Last week, initial claims for unemployment benefits were running close to levels we saw during the same week in 2023 and 2024, let alone 2018-2019. Continuing claims for unemployment benefits are running slightly above where they were in 2023 and 2024, but below 2018-2019. It tells you that hiring has eased relative to the last couple of years, but not overly so. The big picture of the labor market is that if you have a job you’re in a reasonably good place, but if you’re unemployed and looking for a new job, it’s gotten a little harder.

These are all some important reasons why we just don’t see stagflation as a big risk. Of course, that doesn’t mean conditions may not change, but that’s something we monitor closely. And we’ll talk about it, including every week on our Facts vs Feelings podcast that Carson’s Chief Market Strategist, Ryan Detrick and I put out. Take a listen to the latest one below:

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

7769446-0325-A