Every so often, the data throws a bit of a curveball at you, and that’s essentially what the June payroll report did. But that’s also a cue to take a step back and focus on the big picture. Right now, the big picture is that the labor market is in fine shape. That’s good for the economy, but it also sets the Fed up to focus on the inflation side of their mandate. Yet, despite the hawkish pivot in the Fed’s dot plot (the median official out of 19 projected a rate hike in 2026), I don’t think the votes are there for a hike right now (only 12 of the 19 members vote at any given meeting). A bare majority of the voting members are likely in favor of looking through inflationary pressures. However, that also means that monetary policy is relatively dovish, i.e. policy rates remain unchanged even as inflation stays elevated, and that’s a tailwind for stocks. All that said, let’s take a look at the data.

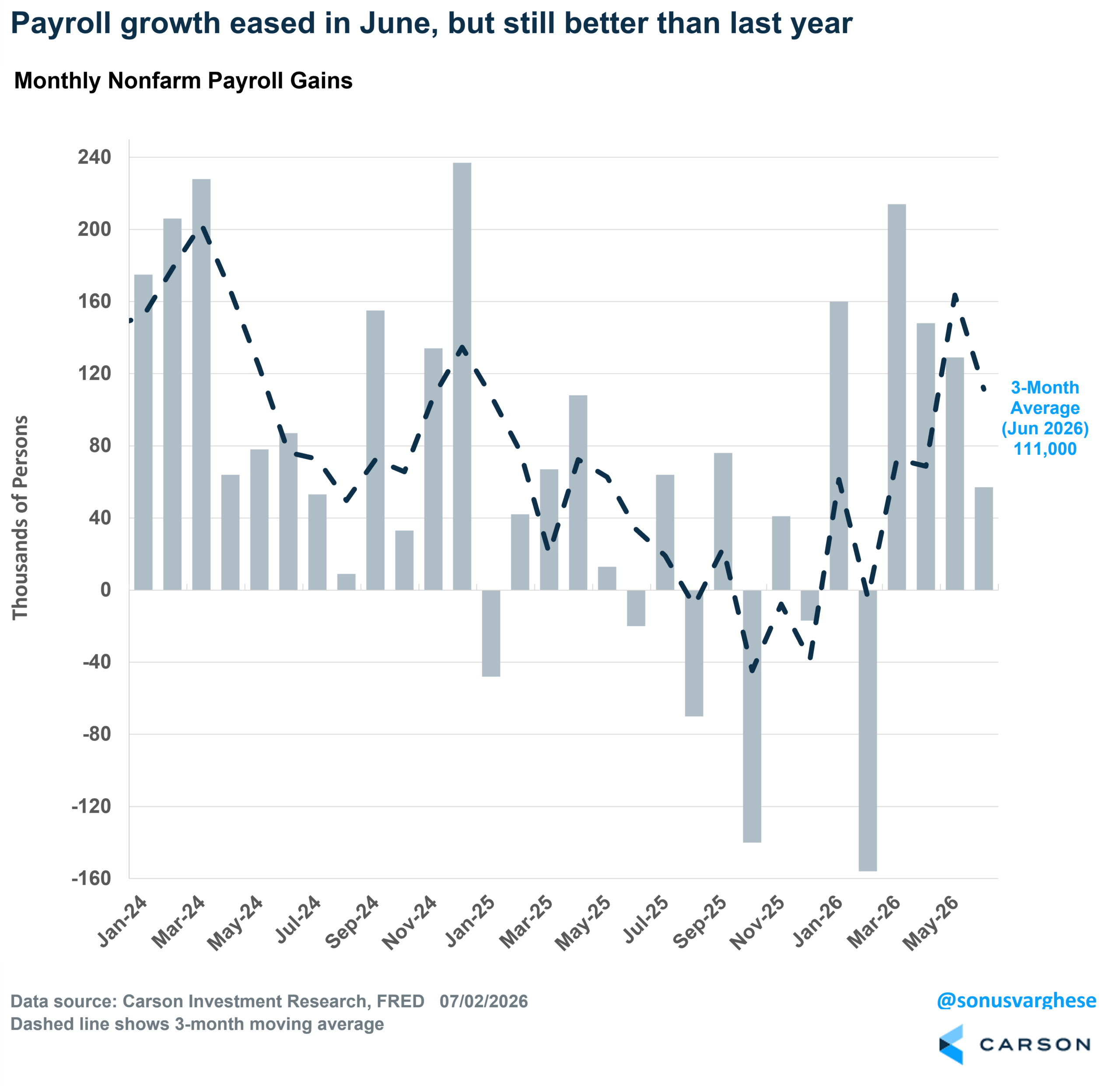

June payroll growth disappointed, with the economy creating “only” 57,000 jobs last month. I used the quotes because in 2025, monthly payroll growth averaged just 10,000. Perspective is everything. Of course, these numbers can get revised, and even in this report we saw big revisions: April payrolls were revised down by 31,000, from+179,000 to +148,000, and May payrolls were revised down by 43,000, from +172,000 to +129,000. That’s why the 3-month average is a better gauge of where things are, and right now it’s running at 111,000 (this would be for the second quarter). That’s a pickup from the first quarter average of 73,000 and the fourth quarter (2025) average of -39,000. Safe to say, things have gotten better.

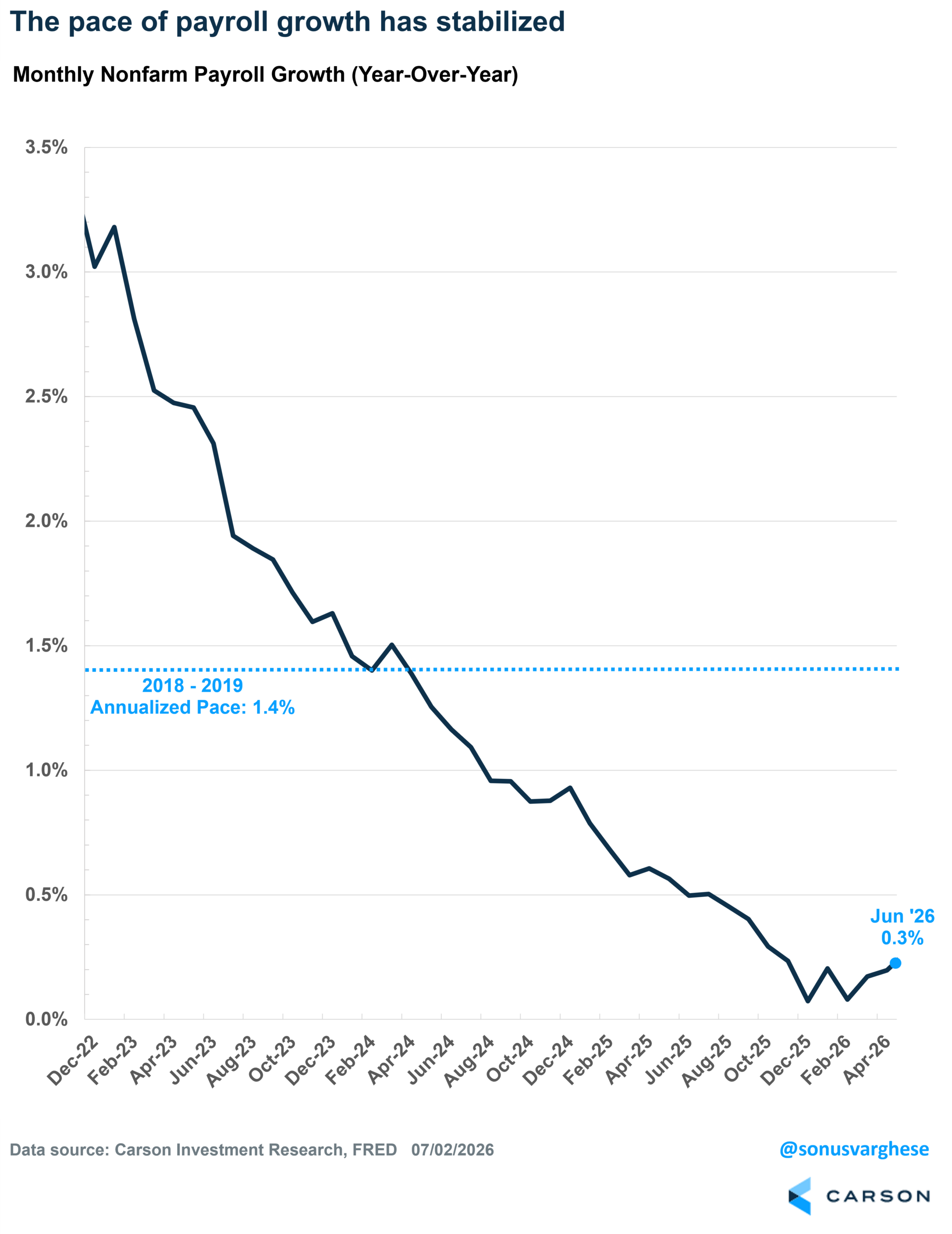

The revised April-May numbers, combined with the reduced pace of payroll growth in June, make more sense. Given the labor supply issues amid the immigration slowdown, the unrevised average of 176,000 jobs in April-May seemed a little too good to be true. It implied much more labor market re-acceleration than is likely the case. Another way to see the labor market stabilization in the job growth is to look at the year-over-year pace: payroll employment is 0.4% higher than a year ago. That is well off the pace from a couple of years ago and the 2018-2019 pace of 1.4%, but the good news is that the line is no longer falling. Things seem to have stabilized, albeit at a relatively low pace, but that’s probably because there’s a lower supply (so fewer workers are available to hire).

Other parts of the payroll report also point to a healthy labor market.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

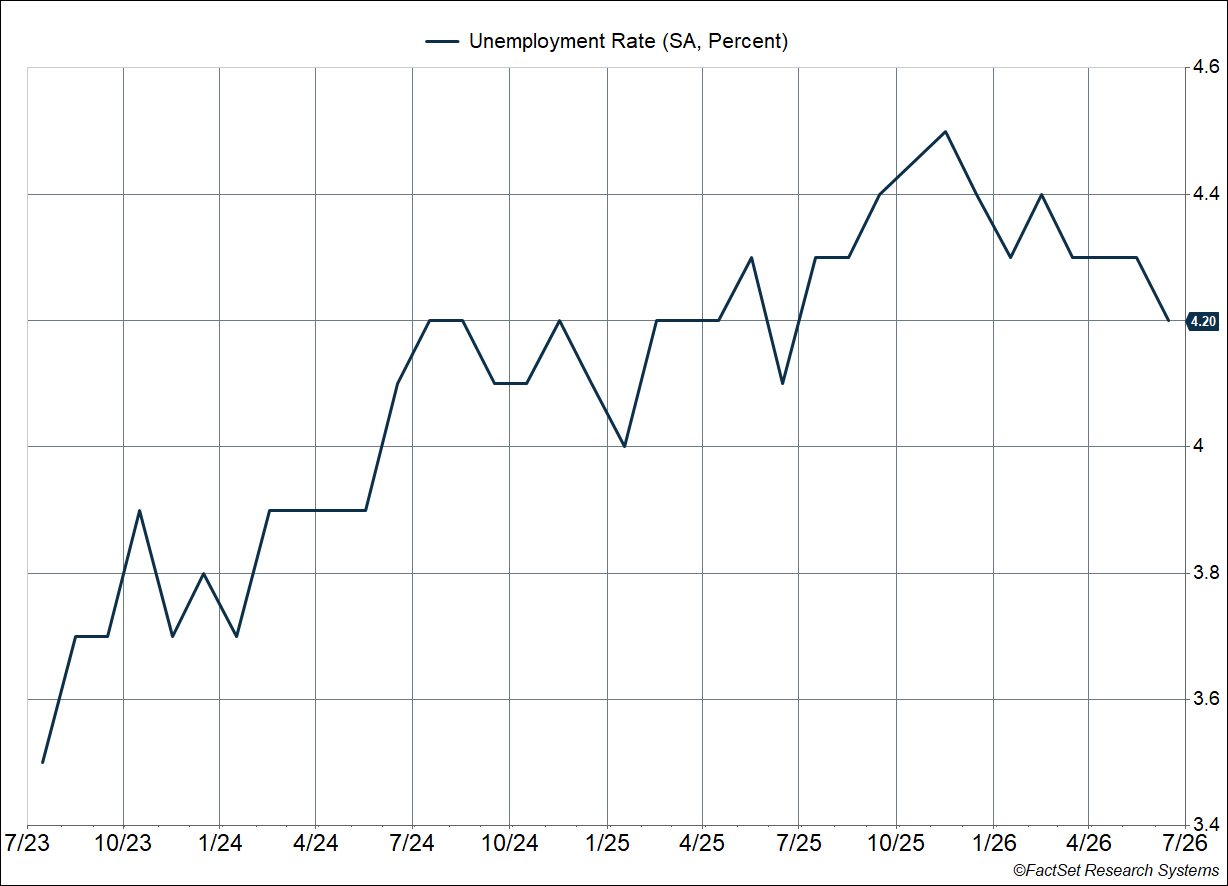

One of the best indicators for the labor market and the economy is the unemployment rate, and that eased to 4.2% in June. It’s the lowest level we’ve seen in the year, and as you can see from the chart below, the increase we saw in 2025 has been entirely reversed now. Keep in mind that an unemployment rate of 4.2% is near historical lows — it just looks elevated relative to recent history, when the unemployment rate plunged to 3.5% in mid-2023. What’s incredible is that the unemployment rate rose in 2024 but then stabilized (after a brief hiccup in mid-2025). Historically, when the unemployment rate starts to rise, it keeps going until we hit a recession.

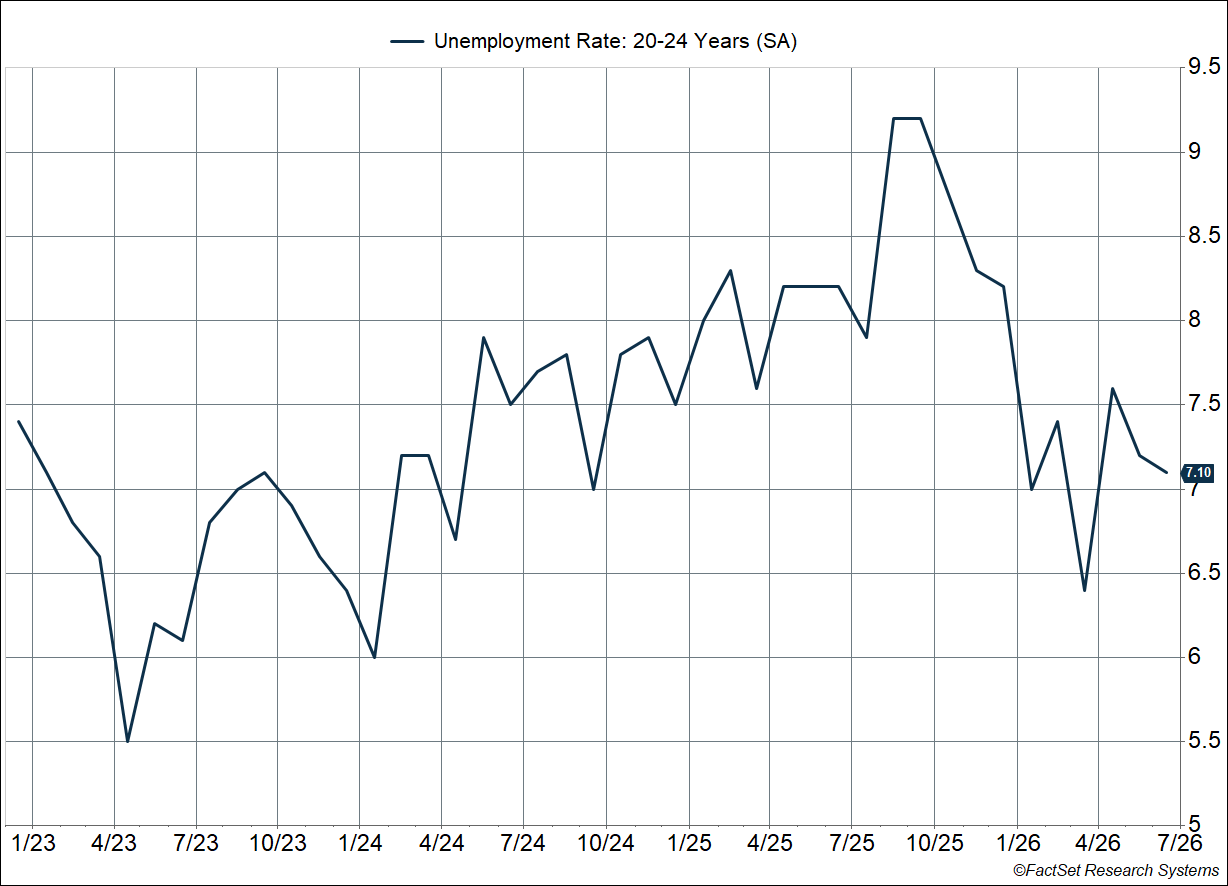

Another piece of good news is that AI doesn’t seem to be impacting job prospects of young workers just yet. The unemployment rate for 20-24 year olds eased from 7.2% to 7.1% in June, well below the recent peak of 9.2% we saw last fall, and in line with what we saw back in 2023 when the labor market was running hot.

Wage Growth Not Keeping Up With Inflation, but Consumers Still Spending

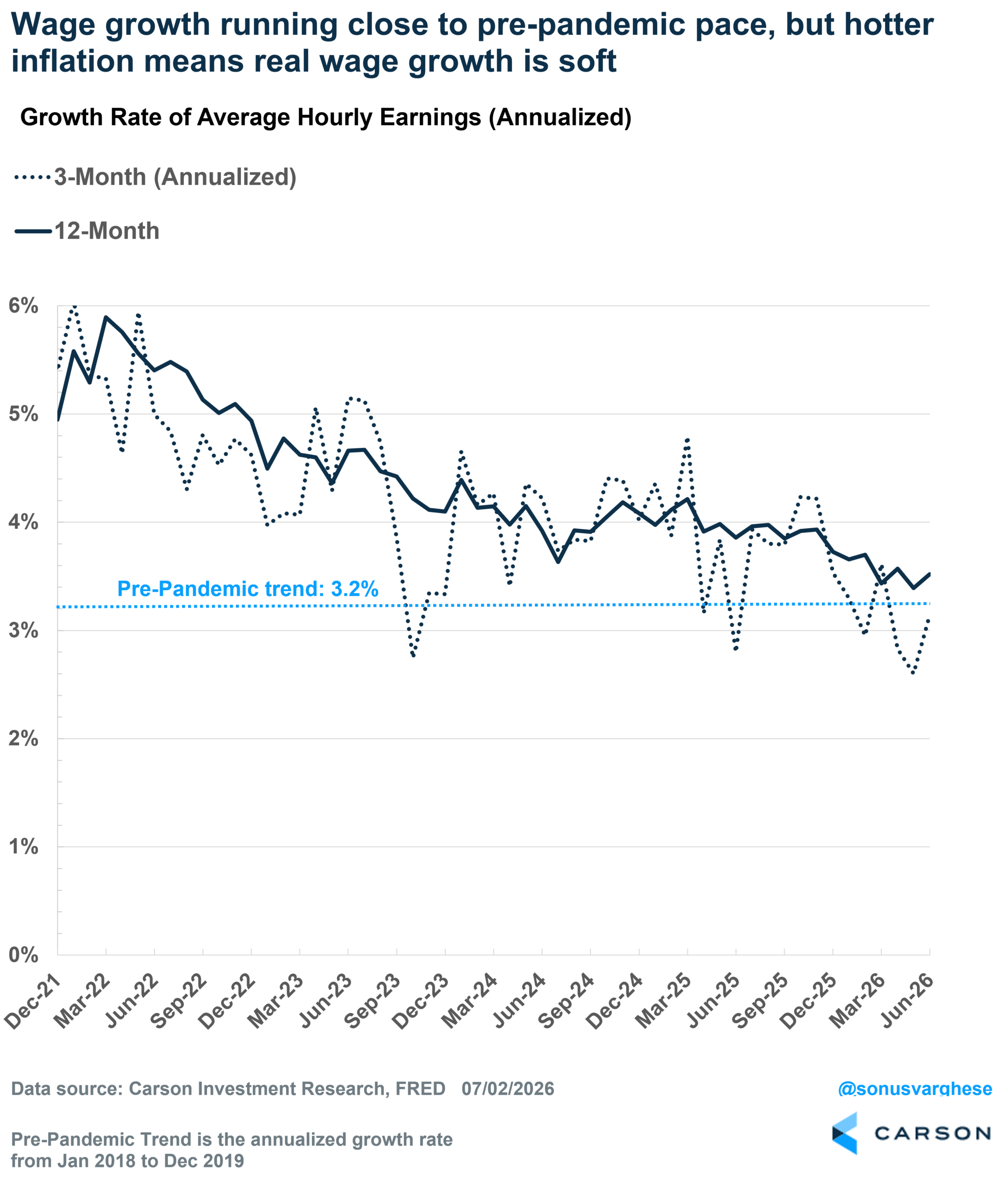

The wrinkle in the data is that wage growth (as measured by average hourly earnings) is running on the softer side. Wages are up 3.5% from a year ago and rose at an annualized pace of 3.1% over the last three months (Q2), more or less similar to the 2018-2019 trend of 3.2%. The problem is that inflation is running hotter now. Headline inflation (using the personal consumption expenditure metric) is up over 6% annualized over the recent three months through May. Easing gasoline prices will help, but even core inflation (excluding food and energy) is running near 3.5%. All this to say, households aren’t seeing any “real” (inflation-adjusted) wage growth.

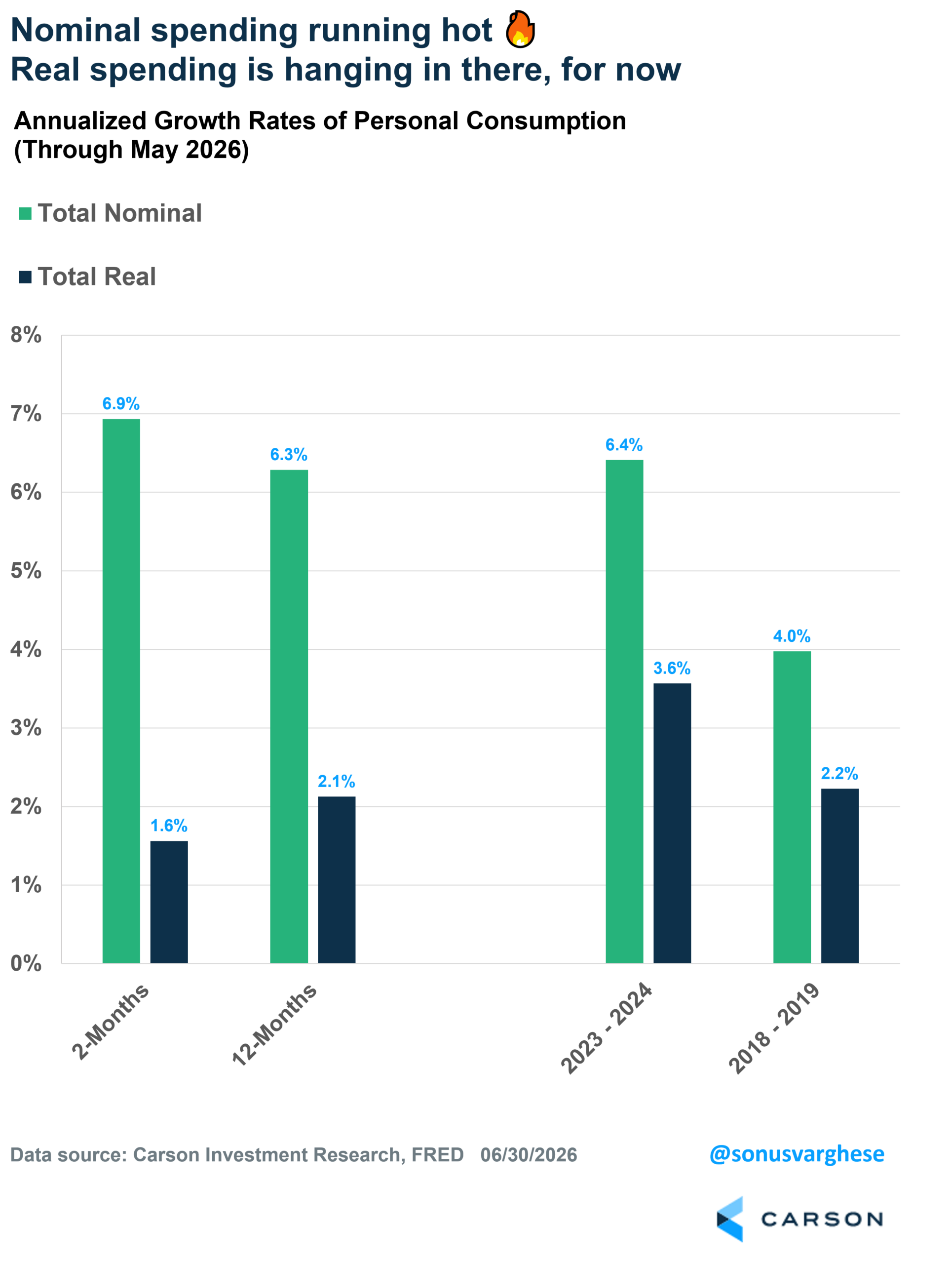

What’s interesting is that despite inflation eating up wage gains, consumer spending is still strong. Personal consumption surged at an annualized pace of 6.9% over the recent two months for which we have data (April-May), above the 2023-2024 trend of 6.4% and well above the 2018-2019 pace of 4.0%. Of course, that’s in large part due to higher prices, but it gets to the fact that consumers are willing to pay up. Once you adjust for inflation, “real” consumption is still up 1.6% annualized over the past two months. That’s below the robust 3.0% pace we saw in 2023-2024, but not far below the 2.2% trend we saw in 2018-2019.

Real spending is what matters for real GDP growth, but we live in a nominal world, and nominal spending (along with nominal GDP) is what matters for company revenue and profit growth. In fact, higher prices are partly a result of companies expanding margins to boost profits. That’s not great for consumers but good for the stock market. The fact that consumers are willing to boost consumption, partly by saving less, tells you that households believe their personal balance sheets are in good shape. Of course, a rising stock market is a big part of that, and for now, it looks set to continue.

For more content by Sonu Varghese, Chief Macro Strategist, click here.

9005638.1. – 2JULY26A