Alan Greenspan died on June 22 at the age of 100, just four days after Kevin Warsh chaired his first meeting of the Federal Open Market Committee. The timing is a coincidence, but a useful one. It bookends roughly forty years of monetary policy and invites a question savers rarely get a clean answer to: across all those chairs, all those cycles, who actually came out ahead by holding cash, and why?

The instinct is to grade the chairs. Volcker, the inflation-slayer, Greenspan, the Maestro, and then a more complicated cast after the Global Financial Crisis. But grading individuals turns out to be the wrong framing. The data tells a story about regimes, not really about personalities, and once we see it that way, today’s setup looks a good deal more consequential than the change of nameplate on the chairman’s door.

Two regimes

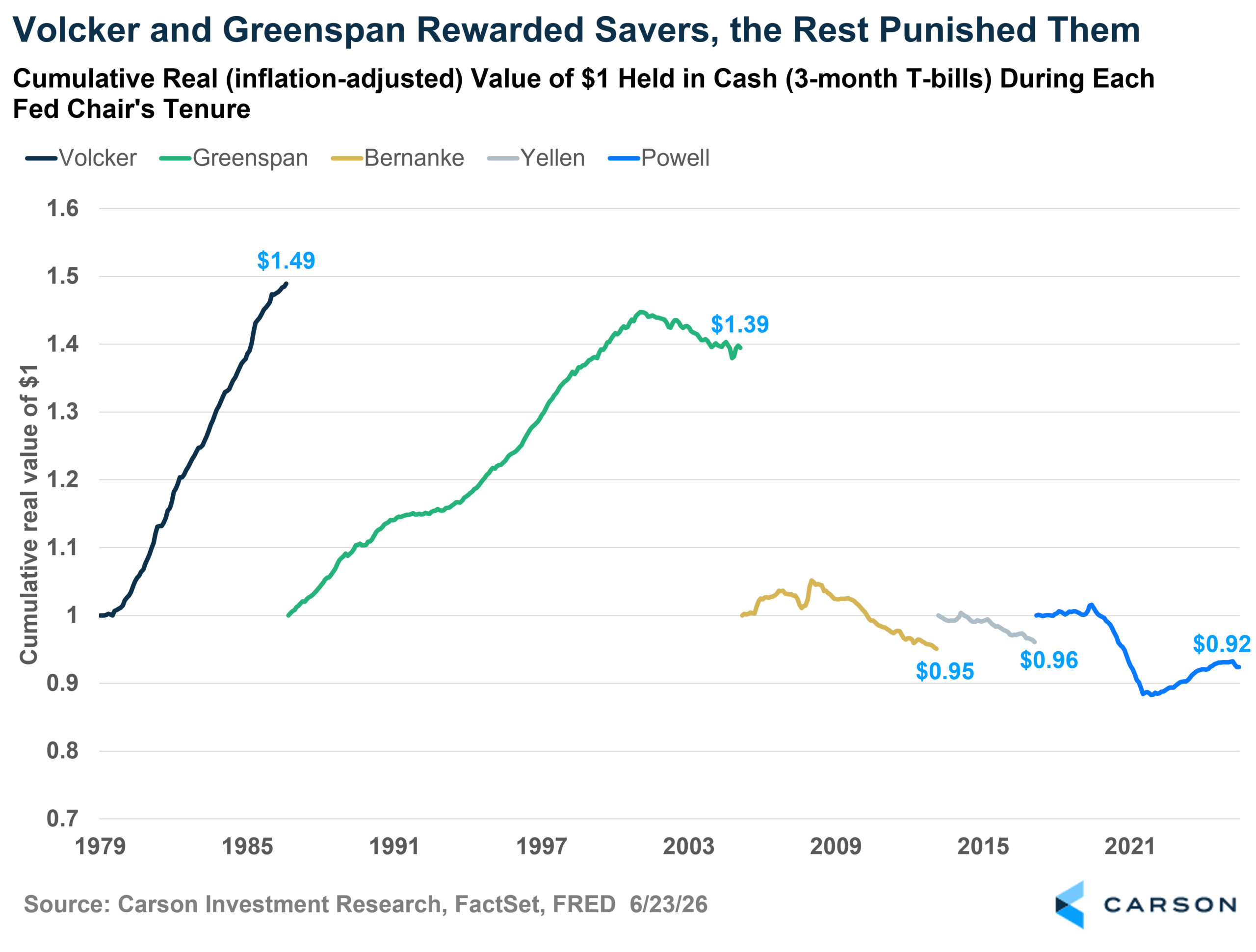

Let’s start with an easy measure of how savers fared: the cumulative real, inflation-adjusted value of a dollar parked in cash, proxied by 3-month Treasury bills, over each chair’s tenure.

A dollar held in cash through Volcker’s tenure grew to $1.49 in real terms; through Greenspan’s, to $1.39. Under Bernanke, Yellen, and Powell, that same dollar shrank to 95, 96, and 92 cents, respectively. The headline really writes itself: the first two rewarded savers, the next three punished them.

Except that framing flatters the early chairs and slanders the later ones. Volcker did not hand savers a 49% real gain out of generosity. He paid enormous real yields because he was strangling an inflation that had already gutted savers through the late 1970s. The “reward” was really the brutal aftercare because inflation ran rampant in the years prior. Greenspan, for his part, inherited and rode a twenty-year disinflation that did much of the work for him.

And the post-GFC trio did not set out to confiscate anyone’s savings. They priced money for the economy they were handed: a balance-sheet recession, a fragile recovery, and inflation that ran below target for the better part of a decade. Savers were not the target of that policy. Unfortunately, they were the collateral.

So the right way to read the chart is not as five performance reviews but as two distinct regimes. The first was a disinflation regime, in which keeping the real return on cash positive was the central task. The second was a zero-rate regime, in which a negative real return on cash was not a side effect but the goal the Fed sought to achieve.

Negative Real Rates as a Policy

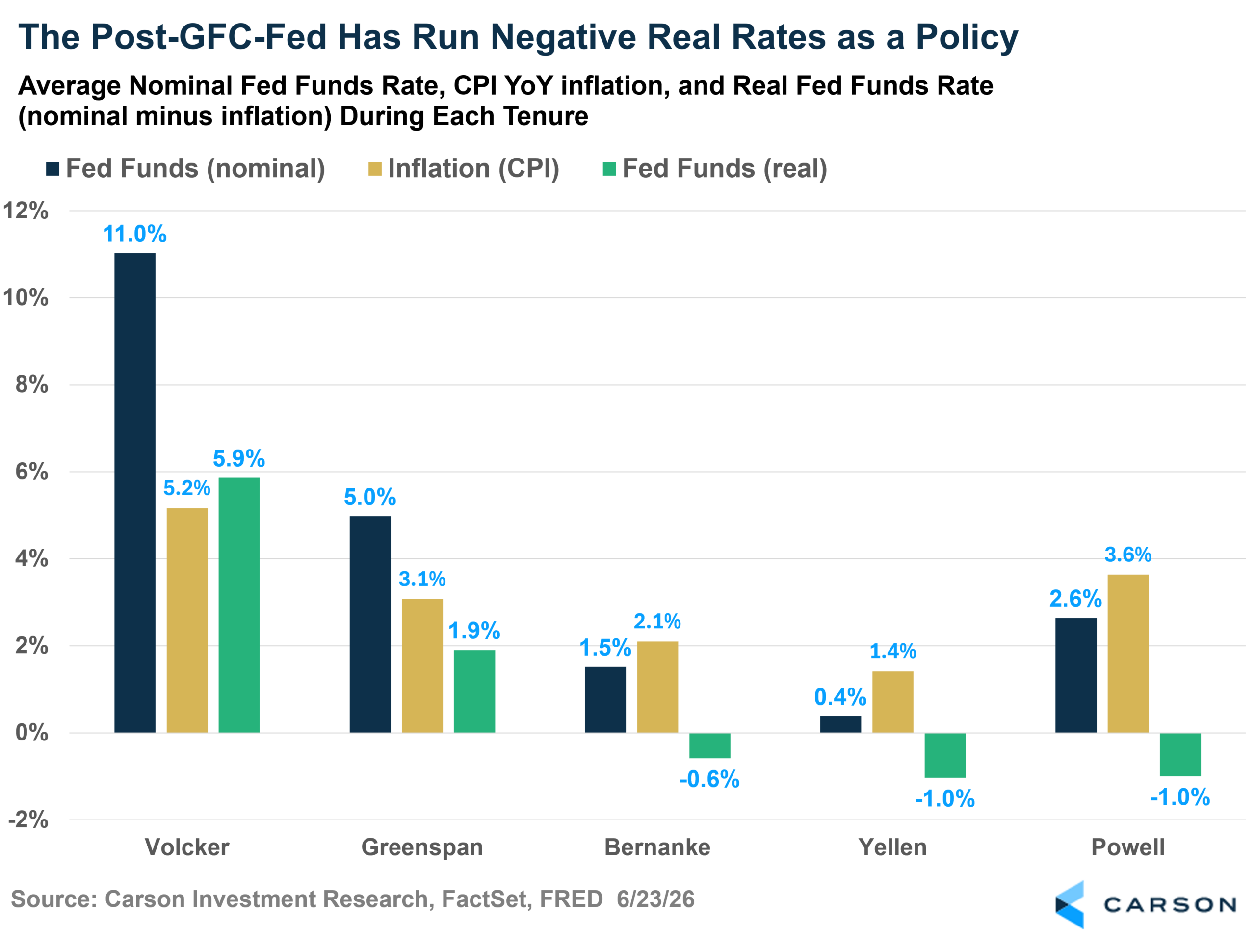

The idea that the post-GFC Fed deliberately ran negative real rates is the reason for everything that follows, so let’s take a look at the data below.

Here is the average fed funds rate under each chair, set against the inflation of their era, with the real policy rate as the result. Under Volcker, real policy rates averaged close to 6%. Under Greenspan, nearly 2%. Then the floor gives way: Bernanke, Yellen, and Powell each presided over average real policy rates below zero. For most of the past 15 years, the Fed deliberately set the price of money below the rate of inflation. That is a transfer from the people who hold cash to the people who borrow it, and it was deliberately chosen repeatedly.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

The Fed wasn’t trying to hurt savers. When rates sit below inflation, holding cash loses value. This pushes households and businesses to spend, borrow, and invest in riskier assets instead of sitting in savings, and you get growth and hiring moving again. The catch is that the same policy rewards those who already own assets or can borrow cheaply, and penalizes those trying to build wealth through savings, which is one of the forces behind the wealth gap that defined this era.

The number on the savings account tells you almost nothing on its own. The gap between that number and inflation tells you everything.

What Does the Regime Cost?

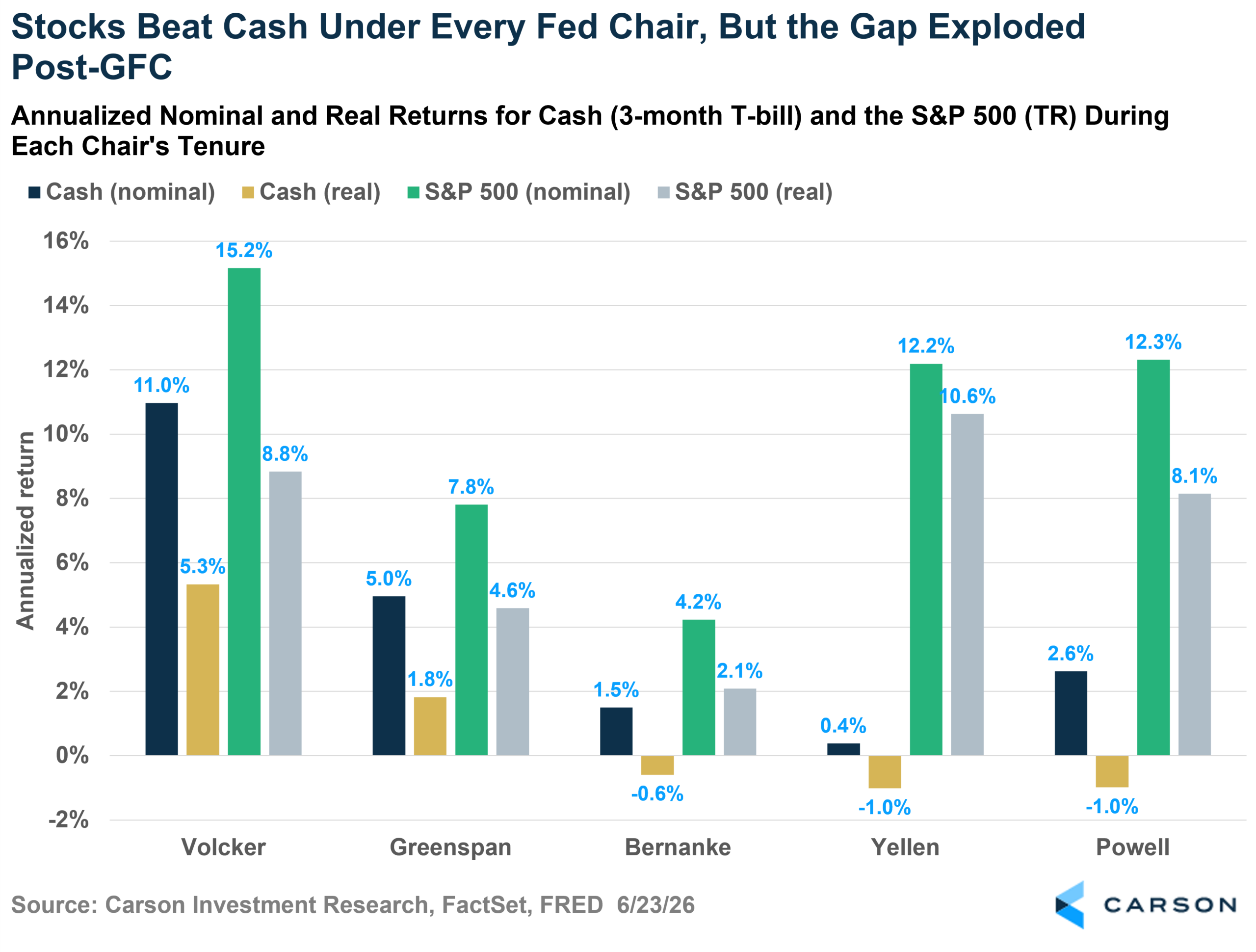

The cost of the zero-rate regime to anyone sitting in cash was not only the slow real erosion. It was also the opportunity given up by being invested in equities.

Stocks beat cash under every chair, which is unremarkable over long horizons. What changed post-GFC was the size of the gap. Under Volcker and Greenspan, cash at least earned a positive real return while stocks earned more. Under Yellen and Powell, cash lost ground in real terms while equities compounded at double-digit real rates. The penalty for safety widened drastically.

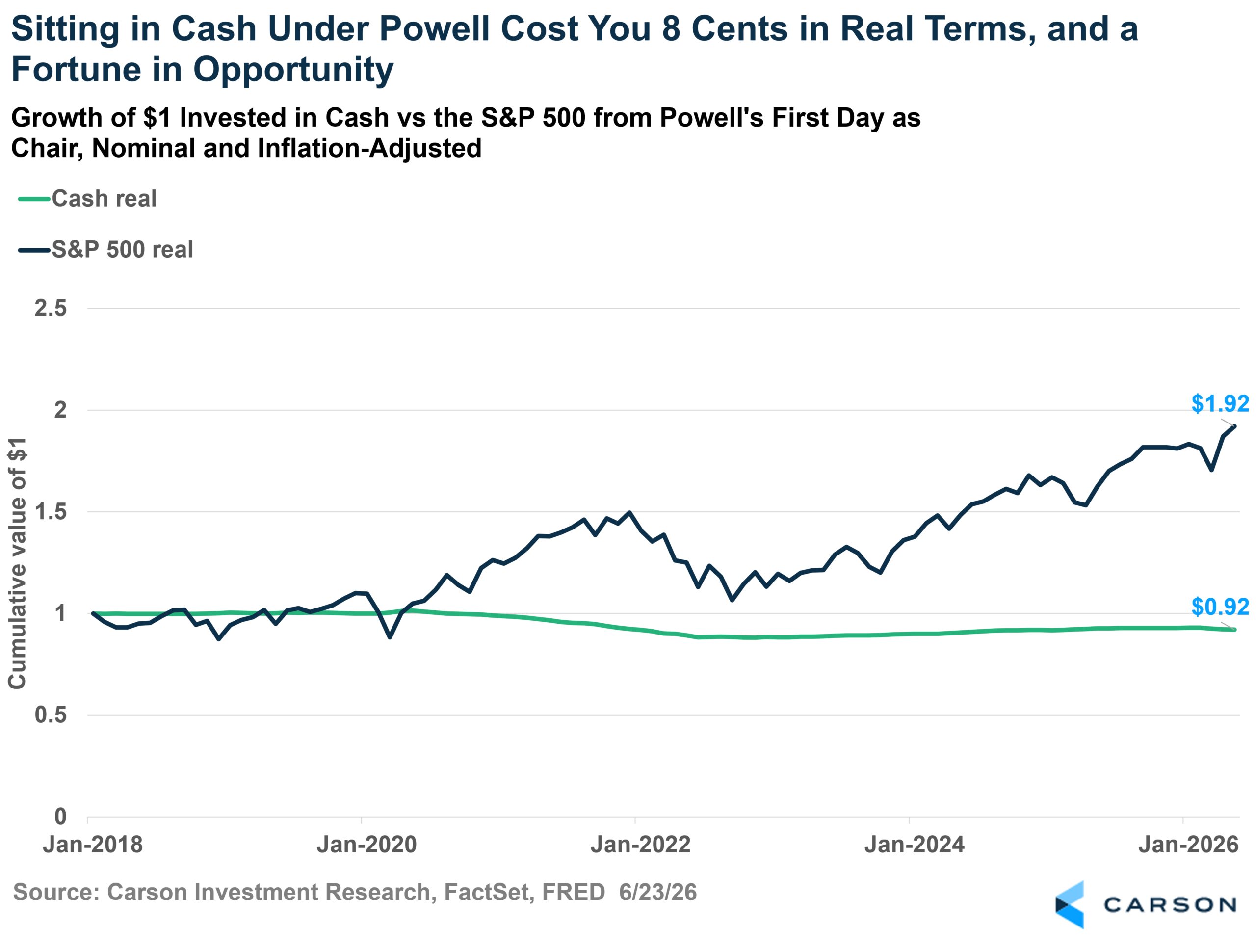

Narrow it to Powell’s tenure, and the divergence is incredible: a dollar in cash drifted down to 92 real cents while a dollar in the S&P 500 became $1.92 in real terms. Eight cents lost outright, and a near-doubling forgone.

None of this means the lesson is simply to get out of cash and into stocks. Two things can be true at once. Cash has been a poor place to store real wealth under the past Fed. But the towering equity returns of the same era were themselves partly a product of zero rates, and there’s no guarantee they repeat once the rate backdrop changes. With equity valuations and momentum near their richest levels since the late 1990s, betting that the next fifteen years look like the last fifteen is a leap the data here doesn’t justify. Cash has eroded real purchasing power for a very long time, and savers should at least know that’s the cost of “safe.”

Which regime is Warsh Inheriting?

This all brings us back to the handoff. The question savers should care about is not whether Warsh is a hawk or a dove by temperament, but which regime he is steering into, and whether he intends to defend their real return.

Many of the following numbers and analyses come from Sonu Varghese on our team. Read more about his analysis here. At his first meeting, the FOMC held rates in the 3.50–3.75% range, and the dot plot turned hawkish: the median 2026 projection shifted from one cut to one hike, and the committee’s own core inflation forecast for 2026 jumped from 2.7% to 3.3%. Yet with the policy rate near 3.6% and core inflation already around 3.5%, the real policy rate today is near 0.1%, and negative relative to headline inflation. That is well below the roughly 1.1% real rate the Fed itself considers neutral. On the metric that matters most to savers, policy is still loose, even as inflation projections climb.

Warsh has also stepped back from the role’s traditional job of explaining how the Fed will react to incoming data, declining to publish his own rate projection and leaning instead on a set of forthcoming internal reviews. For savers, that ambiguity is its own cost. When the chair won’t say how the Fed will respond to rising inflation, the burden of guessing (and the volatility that comes with it) shifts onto everyone else.

Put the pieces together, and the resemblance is not the Volcker setup, where a chair got out ahead of inflation and paid savers handsomely to wait. In my opinion, it is closer to the late 1960s: inflation drifting upward while the central bank, for its own reasons, declines to lean hard against it. Historically, this methodology treats most harshly those holding cash: rising prices met by a Fed content to keep real rates low.

Savers do not have a chair problem; they have a regime problem, and the chair merely decides which regime they live in. Watch the real rate, the gap between what cash pays and what inflation takes, because “safe” money is only safe when the Fed chooses to keep that gap positive. Right now, by its own numbers, it is not choosing that.

By Harry McDonald, Analyst, Investment Research

8994872.1. – 25JUNE26A