“In a very minor way, Berkshire shareholders have participated in the American miracle by foregoing dividends, thereby electing to reinvest rather than consume.” – Warren Buffett, Berkshire Shareholder Letter, 2025

The quote above is from Warren Buffett’s latest missive to Berkshire shareholders, and as usual, it does not miss. There are several nuggets of wisdom in there, but I wanted to highlight the area from which I pulled the quote at the top. One little part that is left unsaid in there is that Berkshire investors, by forgoing dividends, have also avoided paying the taxes on those dividends they would have otherwise had to pay. And in turn, there’s been enormous deferral value, and compounding, that’s worked on the money they avoided paying to the government.

The power of compounding is frequently mentioned when discussing investing, but all too often, that’s cast aside when dividends are brought into the picture (“we need income”), especially when those dividend-paying investments are in taxable accounts. But “income” (passive or not) hurts compounding, a lot.

The desire for income, instead of selling securities when funds are needed, is a relic from a bygone age when transaction costs were high. These days, it is more often (indirectly) a willingness to pay higher taxes simply to invest the way our grandparents might have invested.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

One quick reminder here that when a dividend is paid out, you’re not getting a higher return. The stock price adjusts down for the dividend, and so the total value of your investment remains the same—it’s just hard to see this in real time because stock prices are moving all the time, and dividends tend to be small (so the corresponding price adjustment is also small). Here’s an example: Say you own 100 shares of a stock that is priced at $100 a share. The total value of the investment is $10,000 (=$100 x 100 shares). Now say the stock pays out a $5 dividend per share in cash. Assuming the stock doesn’t move, it’s not like the value of the investment now increases by $500 (= $5 x 100 shares). Instead, if the price is $100 on the ex-dividend date, the price subsequently falls to $95. So, the total value of the investment is still $10,000 (= $95 x 100 + $5 x 100).

On top of that, you have to pay taxes on the dividend payment. Assuming a 20% tax rate on the dividend, that’s equivalent to $1, which is no longer available for long-term compounding. The total value of the investment falls to $9,900 (=$95 x 100 + $5 x 100 – $1 x 100).

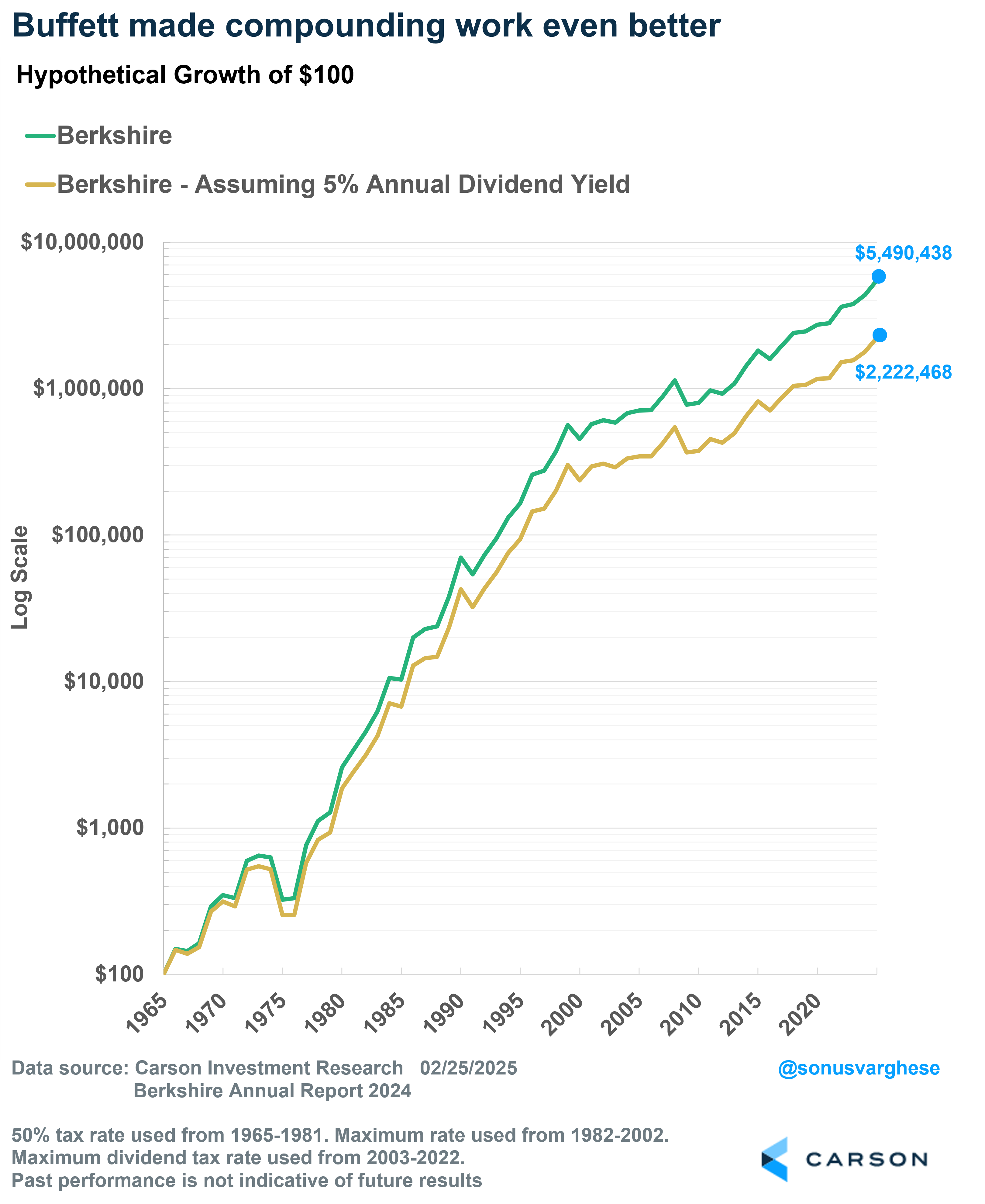

The long-term impact can be significant, which is something Buffett understands all too well. In fact, in his latest letter, he writes proudly that during the 1965-2024 period, Berkshire shareholders received only one cash dividend, a 10 cent distribution on January 3rd, 1967. He writes:

“I can’t remember why I suggested this action to Berkshire’s board of directors. Now it seems like a bad dream.”

He points out that for 60 years, Berkshire shareholders were able to continuously compound what would have been paid out in dividends. And the money was able to compound at the phenomenal annualized growth rate of 19.9%. $100 invested at the beginning of 1965 grew to $5,490,438 by the end of 2024 (versus $38,566 for the S&P 500).

If Berkshire paid a 5% dividend every year (and taxed at the prevailing maximum qualified dividend rate), the compounded annual return would have dropped from 19.9% to 18.2%. That doesn’t sound like a lot, except that the hypothetical $100 would have grown to “only” about $2,222,468 over the same period! Over $3 million lower than what it was without dividends paid out.

The fact that Buffett doesn’t pay out dividends doesn’t mean he never returns cash to shareholders. Instead, he buys back Berkshire stock, which is a much more tax-efficient way to pay out excess cash to shareholders.

Dividends, Qualified or Not, Are a Big Drag

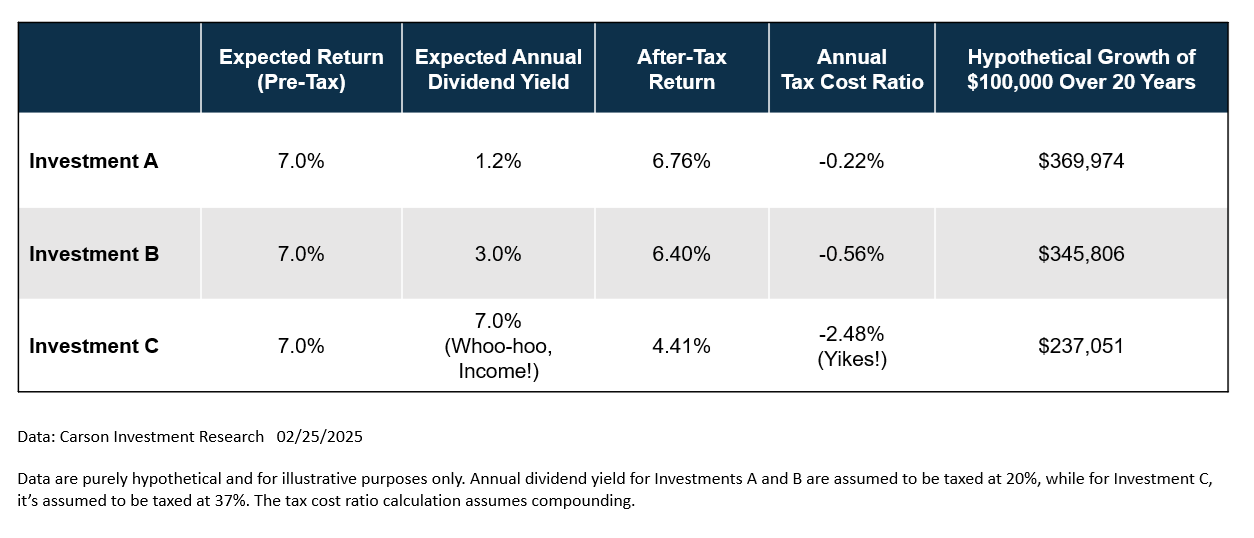

Let’s consider a more general example, which gets to the tax drag of dividends. Assume three different investments, with the same annual expected return of 7% but with different dividend yields.

- Investment A: A dividend yield of 1.2%, similar to the S&P 500’s current yield. Assume these dividends are “qualified,” which means they’re taxed at the preferential rate (assume 20%).

- Investment B: A dividend yield of 3%, replicating popular high dividend strategies that give you “passive income.” Assume these dividends are “qualified”, which means they’re taxed at the preferential rate (assume 20%).

- Investment C: A dividend yield of 7%, replicating a very popular ETF that gives the investor “attractive income” (via call option premiums). Assume these dividends are “ordinary,” which means they’re taxed at the ordinary income tax rate (assume 37%).

Here’s a table showing the after-tax expected return, tax cost ratio for the three investments, along with hypothetical growth of $100,000.

As you can see above, the annual tax cost for Investment A, which has “only” a 1.2% dividend yield is 0.22%. I would argue that even this is quite significant. (Imagine an investment manager you use raising fees by that amount.) The tax cost more than doubles to 0.56% for Investment B, which has a 3% dividend yield. For perspective, the asset-weighted average equity mutual fund fee was 0.42% (though the distribution problem is arguably even worse for mutual funds. Please don’t put them in taxable accounts for this reason).

But taking the cake (quite literally) is Investment C, which touts its attractive income characteristics. But the tax cost is a whopping 2.48%! Imagine losing that every year to Uncle Sam. In fact, if you used a 60-40 portfolio with an expected return of 6% instead of an all equity high income strategy, the expected after-tax return would be higher at 5.2%, assuming 60% invested in stocks with a 7% expected return (1.2% dividend yield taxed at 20% annually) and 40% invested in bonds with a 4.5% expected return (all of it taxed annually at 37%). Color me confused as to how these “income-producing” investments are as popular as they are, unless they’re all being used in tax-deferred accounts (though even then, you’re taxed at the higher ordinary income tax rate when you take distributions).

None of this is to say that you should avoid stocks paying dividends. (Warren doesn’t!) Dividend paying stocks have traditionally been thought of as “quality” and “value,” and there’s a place for them in portfolios. And regular dividend payments can force management to be self-disciplined. However, things may look different when you consider after-tax returns. One way to mitigate the tax cost is to place higher dividend stocks in tax-exempt accounts (like a Roth IRA) and lower dividend stocks in a taxable account.

Of course, if you do need income from a taxable account, consider just taking it out of “total return” as and when you need it, taking long-term capital gains first, which get taxed at the preferential lower rate.

Maximizing after-tax returns is something we think deeply about on the Carson Investment Research Team. And we believe that’s one of the few enduring sources of “alpha” in investing and wealth management. Step one is just to stop chasing products with “attractive” income characteristics. Instead, take a cue from the greatest investor of all time, Warren Buffett.

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

7674004-0225-A