It’s the middle of October and that means being surrounded by Halloween themes. I put up Halloween decorations over the weekend – always a fun activity with the kids – and so being spooked was on my mind. And one doesn’t have to go far for that this year. The Wall Street Journal (WSJ) on Sunday had this article titled:

“Economists Now Expect a Recession, Job Losses by Next Year”

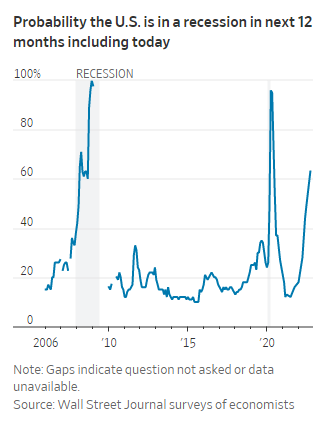

The WSJ regularly conducts surveys of more than 70 economists and asks them to assign a probability to a recession occurring over the next 12 months. In the latest survey, the average probability was 63%, up from 49% in the July version of the survey – the first time the average has gone above 50% since July 2020.

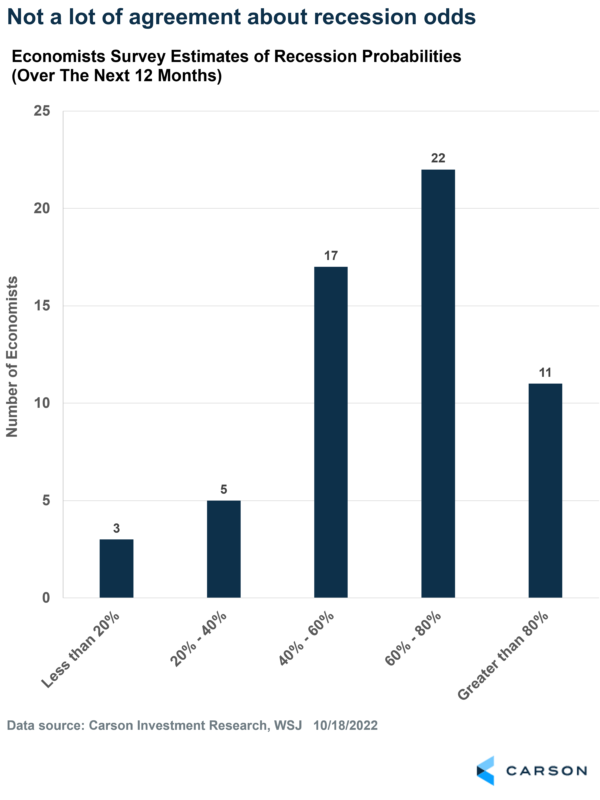

The WSJ helpfully makes the survey data available, and I decided to look under the hood. What’s interesting is that the 63% is just an average, and the views are quite varied. Only 11 out of the 58 economists (19%) who responded to the question are fairly certain of a recession over the next 12 months, assigning a probability of more than 80%. 22 of them were less sure, with probabilities between 60-80%. Another 17 put odds close to a coin flip (40-60%), and 8 of them were even below that.

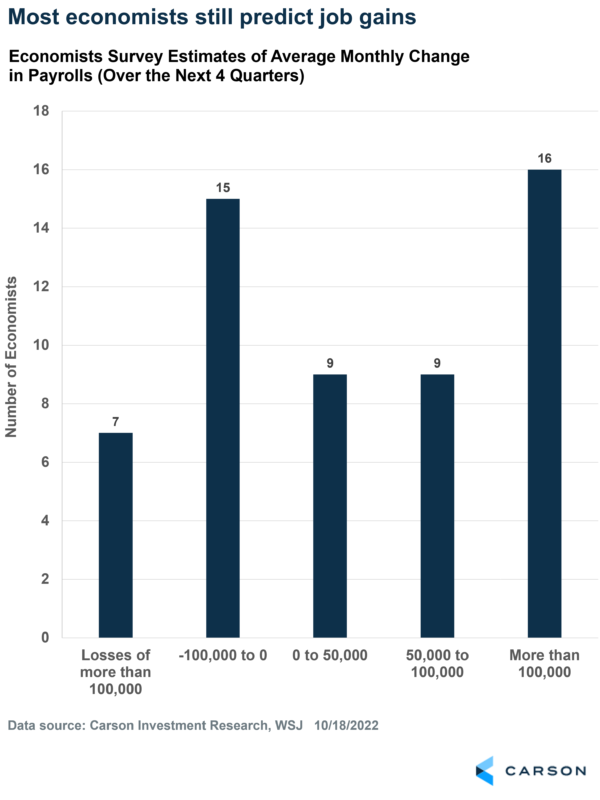

What is interesting are the payroll growth forecasts that 54 of the surveyed economists made. 16 of them predicted gains averaging more than 100,000 per month over the next 4 quarters. This is certainly a far cry from the recent average of 372,000 (July-September), but it would be unrealistic to assume such a robust pace of job creation going forward. Coming back to the survey, another 18 of those surveyed see average job gains of less than 100,000. So altogether, 61% see job growth over the next year. 39% of those surveyed see job losses, with just 13% (7 economists) predicting average job losses of more than 100,000 a month!

What’s driving the wide range of forecasts

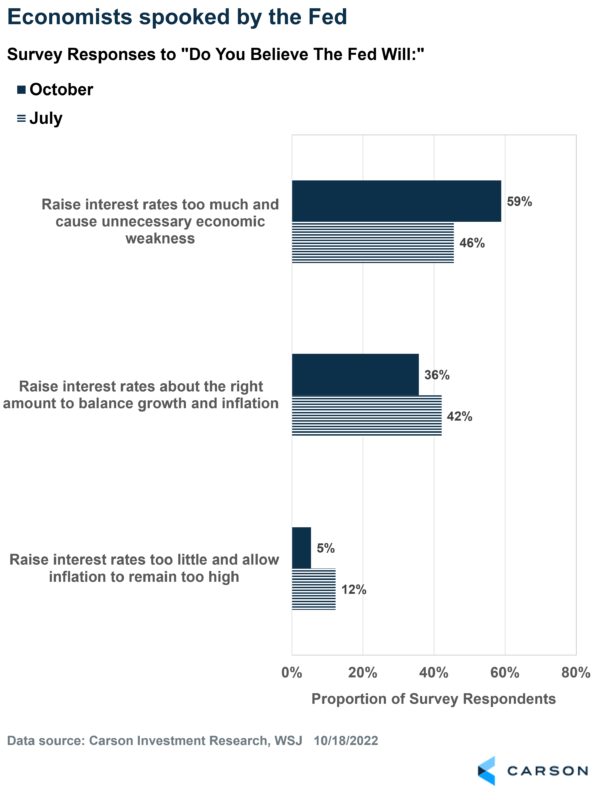

In short, the Fed. Or rather, expectations for potential impact of the Fed’s aggressive rate hikes on the economy (especially if there’s more to come). 59% of the surveyed economists now believe the Fed will raise interest rates too much and cause unnecessary economic weakness, up from 46% in the July survey.

There are so many subjective judgements baked into these answers, including 1) how far they think the Fed will go with aggressive rate hikes, 2) the impact of those potential rate hikes on the economy, and 3) the timing of the impact (which could take up to 2 years for peak impact).

Obviously, there is a lot of uncertainty around this stuff and that’s something to keep in mind. It helps to focus on what’s happening now to understand what’s happening with the economy, and continuously update that view as new data rolls in.

Who isn’t spooked?

Aggressive rate hiking by the Fed is certainly something to be worried about. But one person who doesn’t appear to be worried, at least based on what he’s seeing, is JPMorgan Chase & Co Chief Financial Officer, Jeremy Barnum.

To give you some context, Jamie Dimon, the bank’s CEO has been warning for several months of impending recession, and last week he put a timeline on it: 6-9 months. The bank just had their quarterly earnings call late last week (in which they beat estimates across the board) and in the Q&A session, Dimon was asked to add to his comments, and whether consumers (i.e. their clients) are feeling economic pain from inflation and higher rates. Before he had a chance to respond, his CFO stepped in, and it’s worth quoting him in full:

“The short answer to that question is just no. We just don’t see anything that you could realistically describe as a crack in any of our credit performance. I made some comments about this in the prepared remarks on the consumer side, but we’ve done some fairly detailed analysis about different cohorts and early delinquency bucket entry rates and stuff like that. And we do see, in some cases, some tiny increases, but generally, in almost all cases, we that’s normalization, and it’s even slower than we expect.”

Dimon went on to add that consumer spending is very strong, balance sheets are very good for consumers, credit card borrowing is normalizing (not getting worse). “So, you can go into a recession, you’ve got a very strong consumer”.

So. there you have it – the largest bank in the US isn’t seeing any cracks, yet.