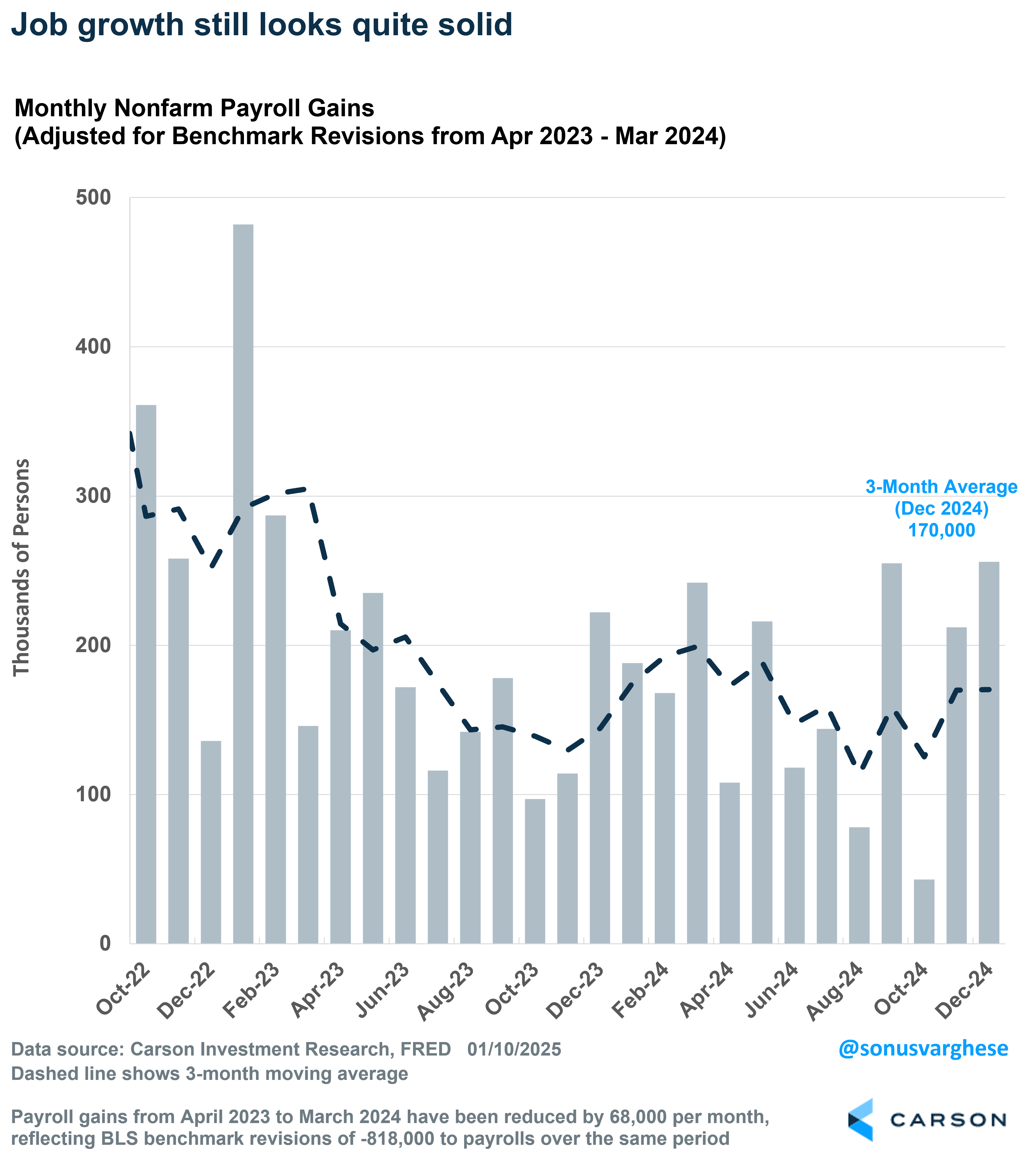

There have been a few signs that risks to the labor market are tilted to the downside, but the December payroll report went a long way towards easing them. The economy created 256,000 jobs in December, blowing past expectations for a 165,000 increase. Monthly numbers can be noisy and so a 3-month average is helpful. That’s running at a solid 170,000 per month, versus an average of 166,000 in 2019. The economy created over 2 million jobs in 2024, down from 2.4 million in 2023 but well in the ballpark of what we saw in 2017-2019 (2.1 million average per year).

Also good news was the unemployment rate falling from 4.2% to 4.1%. That’s up from 3.7% a year ago, but we’re off the summer scare when the unemployment rate picked up to almost 4.3%. The prime-age (25-54) employment-population ratio, which is a way of controlling for demographic effects and labor force participation issues, is 80.5% — exactly where it was a year ago, and higher than at any point between May 2001 and December 2019.

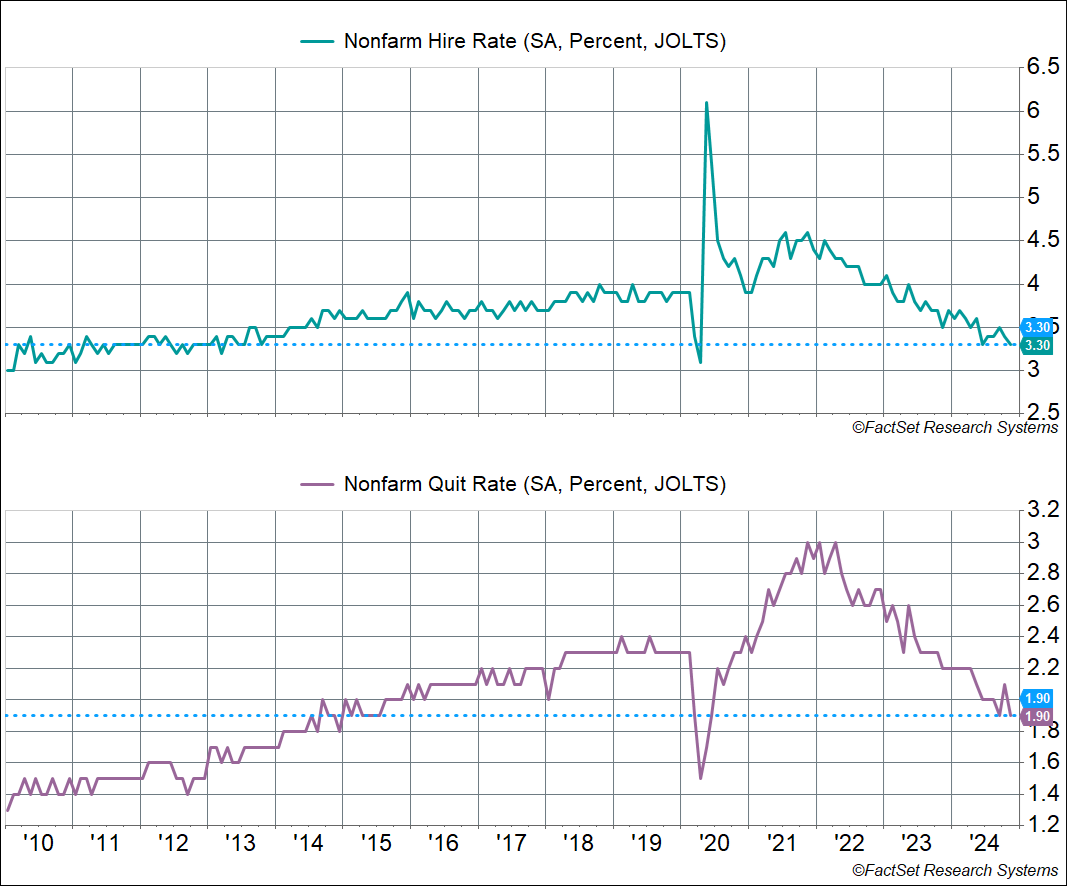

If the labor market stabilizes here, that’s a pretty good place. There are still some concerns though. Overall hiring has slowed a lot. The hiring rate, which is the number of hires as a percent of the labor force, has fallen to 3.3%, the slowest pace since 2013 (outside of the Covid months). But net hiring (which is what comes out of the payroll report) is still strong because separations are low. Workers are quitting their jobs less frequently. The quit rate has fallen to 1.9%, versus 2.3% in 2018-2019. By no means is a 1.9% quit rate a bad level but it’s the trend that’s concerning. It tells you that workers are wary of quitting their jobs because it’s probably hard to find another one that’s better.

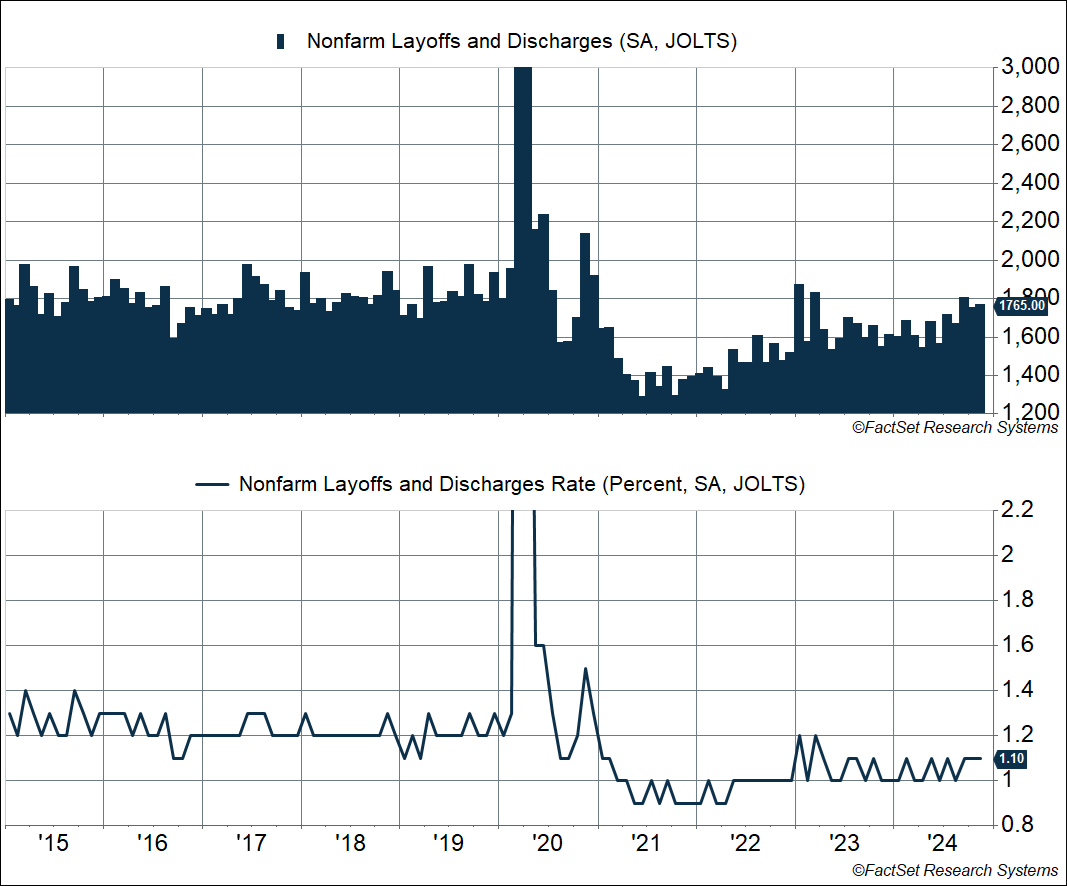

Separations are also low because layoffs are running low, around 1.77 million versus 1.8 – 1.9 million before the pandemic. But the labor force is also larger now. The layoff rate (layoffs as a percent of the workforce) is at 1.1% (versus 1.2-1.3% in 2018-2019). Companies clearly want to hold onto their workers, who have also become a lot more productive at their jobs. But they’re more judicious about hiring.

The big picture is that the labor market is in a solid place and it looks to be stabilizing. I like this summary from labor economist, Guy Berger:

- This is good job market if you’re happy with your job, as wage growth is relatively strong and the probability of getting laid off is low

- It’s a not a great job market if you have a job but are looking for opportunities

- It’s a tough job market if you don’t have a job and are looking for one

But Wait, Is Good News Bad News?

The December payroll report was broadly positive from several angles. However, investors weren’t too happy. The interest rate on 10-year treasury notes jumped from 4.68% to about 4.75% and the S&P 500 pulled back by over 1.5% (and the small cap index, the Russell 2000, was off almost 2%). It’s typically not useful to read too much into market moves, especially short-term ones, but the immediate reaction is interesting and worth going into.

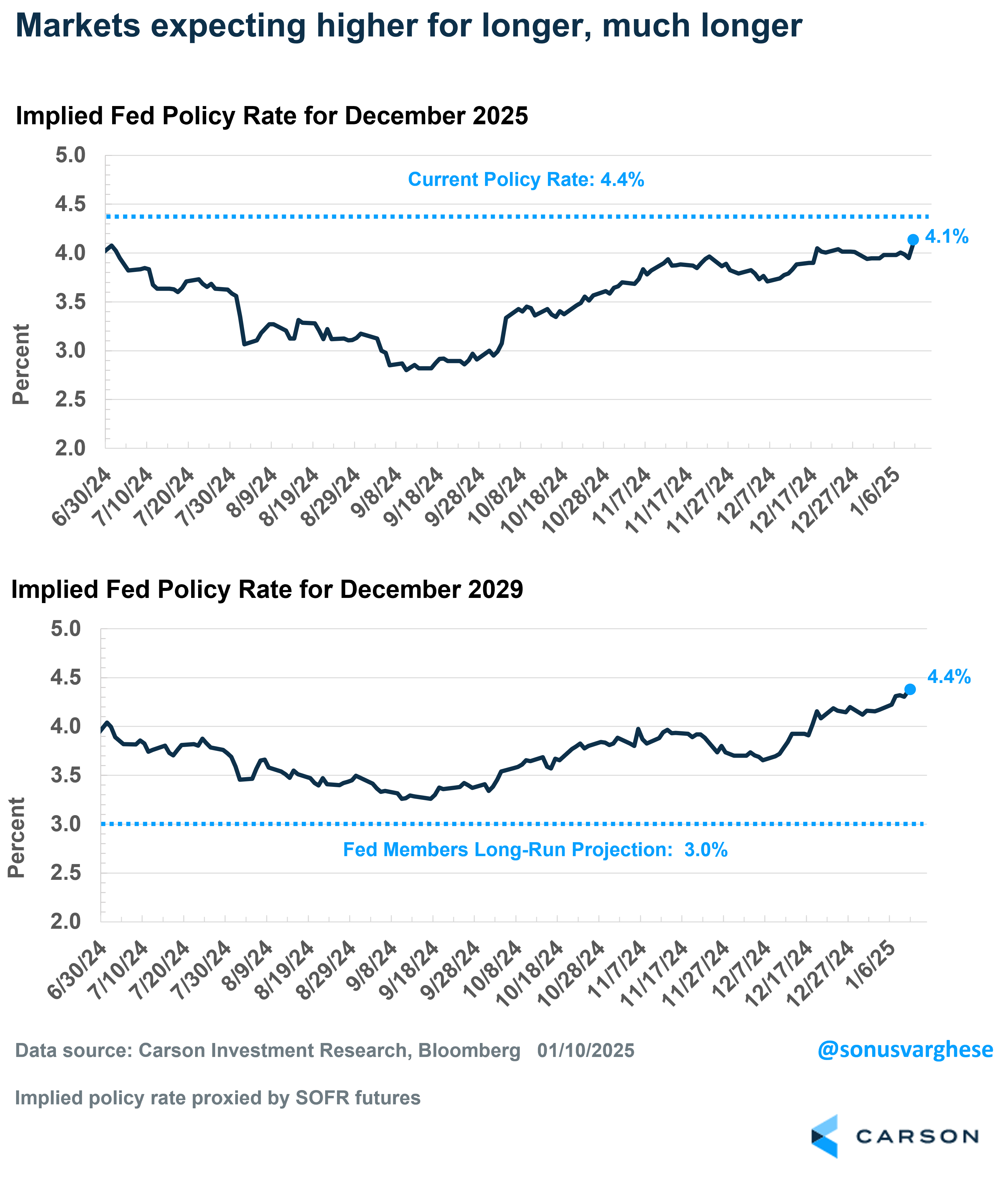

Interest rates are higher because the market likely thinks stronger job creation, and a stronger economy, will put more upward pressure on inflation, which means the Federal Reserve (Fed) will have to pause on rate cuts. Cue expectations for rate cuts in 2025, which moved significantly after the payroll report was released. Markets are now expecting just one rate cut in 2025 (with a probability of under 25% for a second one) and don’t expect it to happen before June. The 2025 policy rate is expected to be about 4.1% (currently at 4.4%). And markets don’t expect the Fed to cut any more after that. Long-term policy rate expectations have climbed to 4.4% (I proxy this using the expected 2029 policy rate). All of which largely explains why longer-term interest rates have surged as much as they have. As you can see, policy rate expectations have been creeping up since last summer, mostly as the labor market data has come in better than expected (along with other economic data).

Now, I wouldn’t put too much stock into what markets are pricing in by way of rate cuts. A year ago today, markets priced in 7 cuts (1.7% %-points total) for 2024, and then shifted it to just 1 cut by summer (0.25%-points), before setting on 4 cuts by year-end (1 %-point, which is what we got). Things can shift, by a lot.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

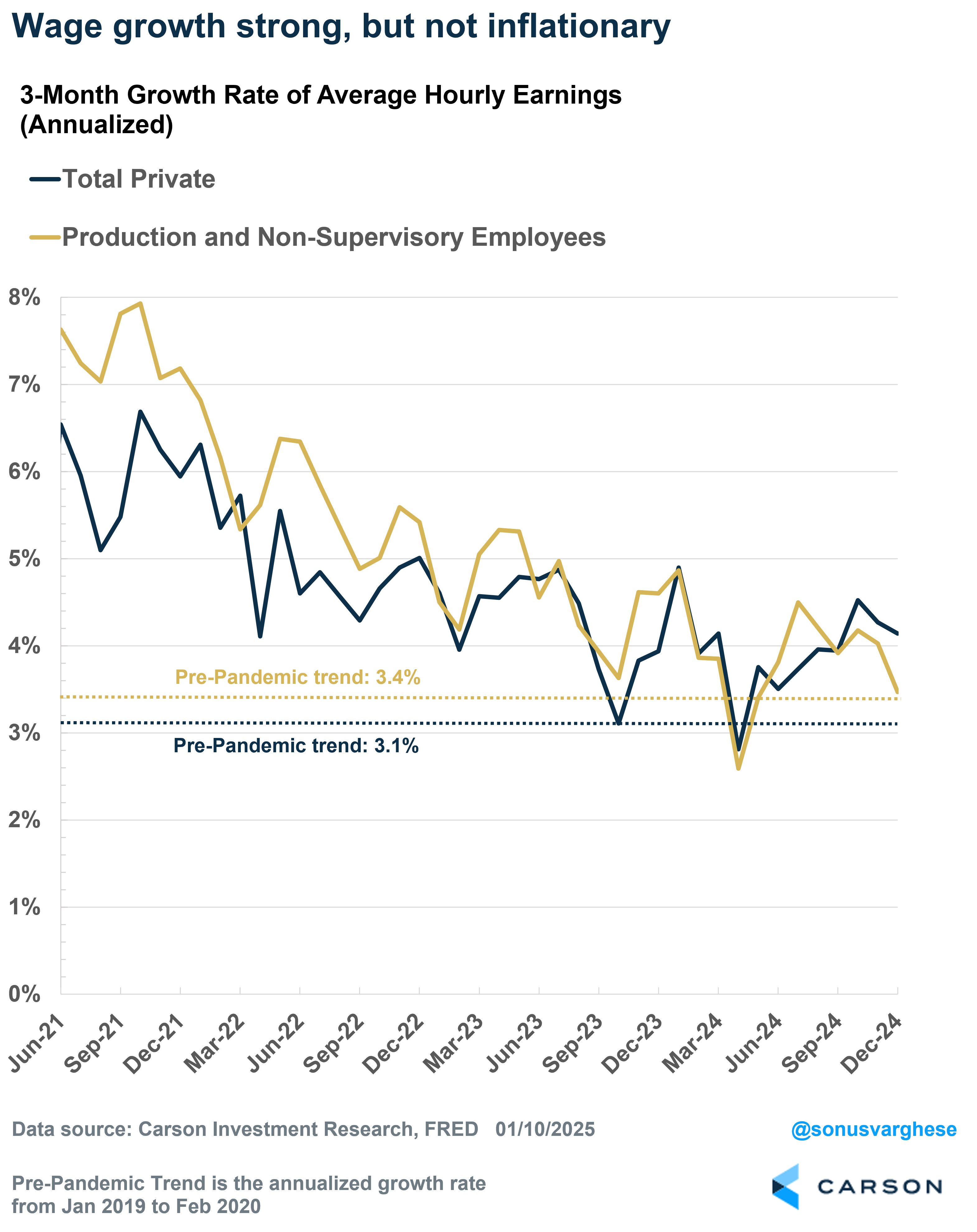

I do think we may be sitting on our hands waiting for the Fed to cut rates once again, even though I believe we’re likely to see the Fed cut 2-3 times in 2025. Ultimately, it comes down to the inflation picture. I’ve written a lot about this and the issues with lagged components of inflation data (like shelter, but also things like rising stock prices). Yet, the forward-looking picture still suggests inflation is running close to 2%. We got more data pointing to this in the December payroll report. Over the last 3 months, wage growth for private sector workers is running at a 4.1% annualized pace, and for production and non-supervisory workers (non-managers, who tend to spend more of their income), it’s at 3.5%. These are strong levels and suggest consumption should remain strong. But they’re also very close to what we saw pre-pandemic, telling us there aren’t any demand-side inflationary pressures in the economy.

Hopefully Nothing Breaks While We Wait for the Fed

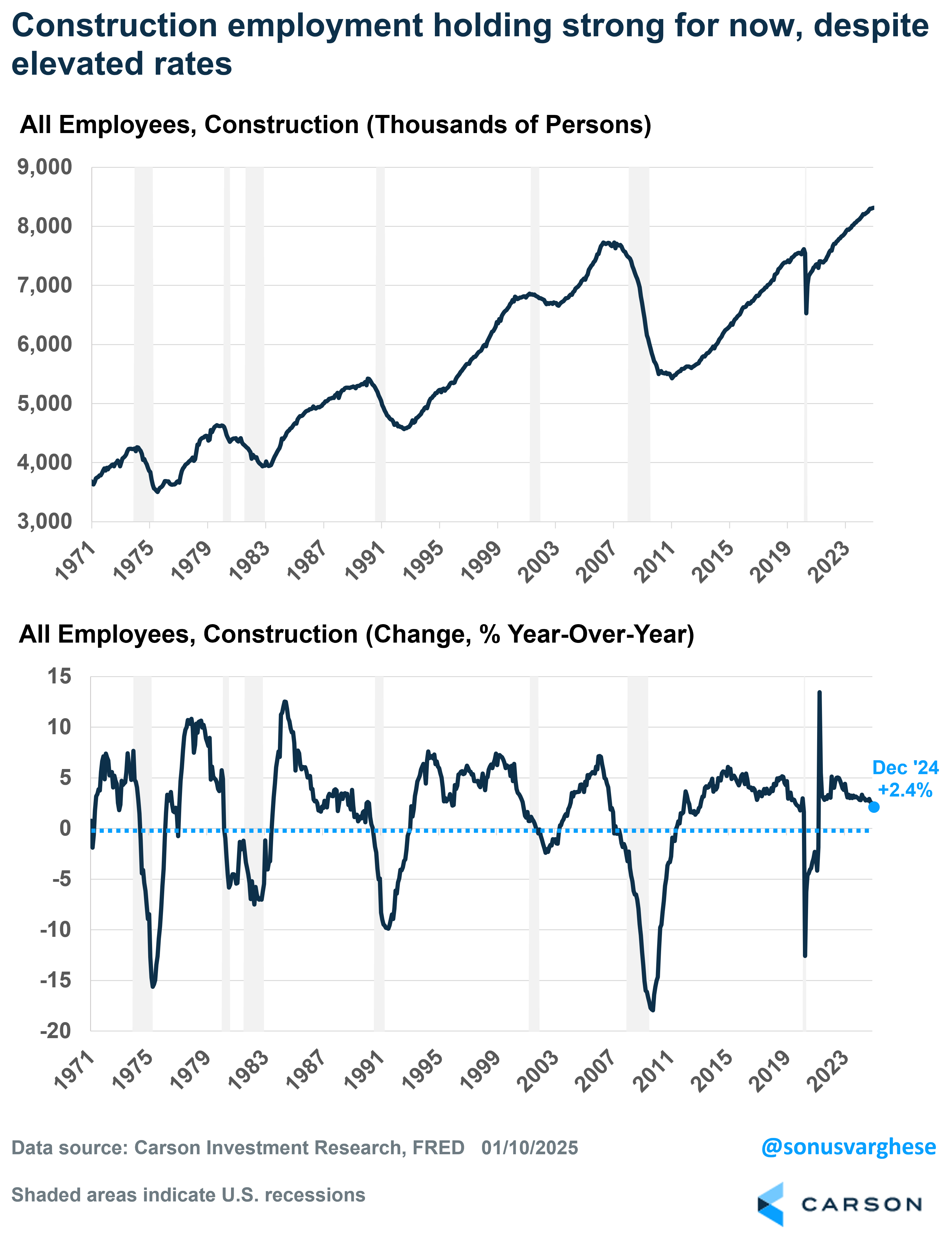

While we wait for rate cuts, the hope is weakness in rate-sensitive parts of the economy doesn’t creep into other areas. Housing is really the key here. Mortgage rates are running around 7.3% right now, and at that level, it’s tough times for housing. Mortgage applications and refinancings are down 20% from November, and the latter are down 65% from September. If mortgage rates stay elevated into the spring home-buying season, that’s a potential drag on the economy. For now, the only relief is that housing weakness has not crept into construction employment. It was strong even in 2022 and 2023, which was another clue that a recession wasn’t imminent. Historically, construction employment has foreshadowed further weakness across the labor market (and recessions), which makes sense because elevated interest rates (and tight monetary policy) has preceded past recessions. If housing remains weak due to elevated rates, we could see construction employment start to pull back. For now, construction employment is rising at a 2.4% year-over-year pace — still healthy, especially relative to the 1.8% increase in 2019 but the current pace is down from 3% a year ago. The downward trend is something we’ll be keeping a close eye on for the next several months.

Keep an eye out for our Outlook 2025, in which we discuss a lot of the strengths the economy has going for it, but also potential risks. It will be released on Tuesday, January 14th. Without giving too much away, Ryan and I gave some hints of what’s coming in our latest Facts vs Feelings episode, even as we discussed what we got wrong and what we got right in 2024. Take a listen.