A little more than 10 years ago, on June 23 2016, United Kingdom voters went to the polls to vote in a referendum on whether or not to leave the European Union (EU). The next day, it was announced that the UK electorate had voted to leave the EU, 51.8% to 48.2%. The outcome was considered a surprise and, for some, a shock. Betting markets on the eve of the vote had the odds of “stay” winning at 70-75%. Forecasters on average had stay at about 2-1. Polls were even closer.

The vote was advisory rather than binding, but strong advocacy among some key political leaders and the weight of a referendum vote that expressed the will of the people made it binding from any practical perspective. Parliament authorized Article 50, the provision in the European Union’s founding treaty that allows a member state to leave, on March 16, 2017, by a vote of 498-114. Following the vote, there were also some efforts to find a path to enacting “Brexit lite,” but they made little headway. It was a messy divorce with a massive amount of legal, regulatory, trade, and bureaucratic issues to work through. More than four years after the initial vote, on January 31, 2020, the UK formally left the EU. There was still a transition period to work through, which ended December 30, 2020, and a new trade agreement to put in place, which was fully ratified on May 1, 2021.

Does Brexit Still Matter on Its 10-Year Anniversary? Well, for the Brits, most definitely. Brexit has had a meaningful impact on the UK economy, mostly for the worse, and that effect has some ongoing impact on the global economy and markets. But for the typical US investor at this point, that probably doesn’t matter much. It also has a symbolic impact as one of the most important geopolitical events of the last decade, and for its role in the narrative around rising populism. But it may matter most for lessons learned.

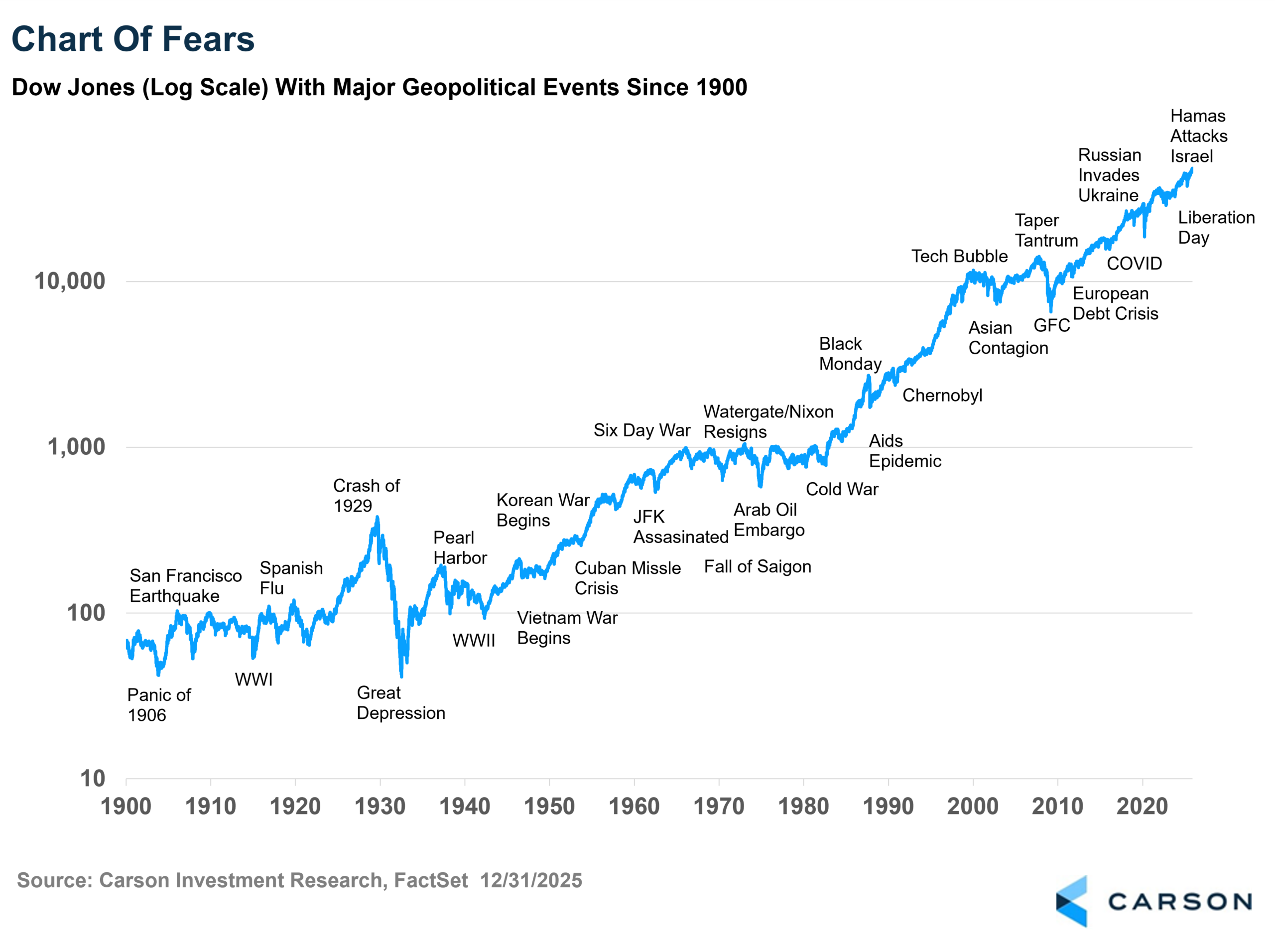

Geopolitical Events Happen

Even within the relatively short span of the last decade, I wouldn’t rate Brexit in the top 3 geopolitical events. Covid dominates everything else. Russia’s invasion of Ukraine probably comes next. And while not an event, I would put the US-China trade war and strategic rivalry third. But it was an event that has impacted some segments of the market and had meaningful macroeconomic consequences. But on a larger scale, markets have a strong history of powering through geopolitical events. There’s something of an exception for events that are a large enough shock to cause a recession, but even in those cases, equity markets have been able to consolidate, reset, and move forward.

Be Careful What You Wish For

The UK had a lot of legitimate gripes with the EU and did win greater political autonomy by leaving the EU, no small thing. But be careful what you wish for. Often, it’s very easy to see negatives in policy (and even easier to campaign on them) while missing benefits that might have become so everyday they’re almost invisible until you lose them. (See trade and inflation.) A National Bureau of Economic Research study estimates that the UK economy is 6-8% smaller than it would have been without Brexit, investment is 12-13% lower, employment 3-4% lower, and productivity 3-4% lower. The difference isn’t just academic — it has been experienced on the ground. Take single surveys with a grain of salt, but a YouGov UK survey taken this month saw 57% of participants saying the decision to leave the EU was a mistake, while 30% said it was the right move. That 27%-point spread is significant.

An Early Chapter in the Populist Narrative

“Populism” as a term gets so bandied about now that it’s become almost meaningless. Does it belong to the right or the left? Most political orientations, including a populist wing and populist positions, can cross traditional party lines. Both FDR and Donald Trump could be called populists, with qualifications, and most politicians in a modern democracy must have at least some populist appeal.

The high-profile political victories most commonly called populist over the last decade or so have occurred on the right, but there are populist movements on the left as well. Definitions are loose, but it’s often characterized as prioritizing the wants and needs of the broad populace against the priorities of the elite, sometimes framed as the establishment. The more cynical perspective is that populism is a broad strategy of pandering to the broad populace to make them more amenable to authority. It’s an old strategy and in practice, is usually some combination of principled and pandering.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Brexit was the real launch of the current populist narrative arc. It did not in any way cause later populist successes, but it was a sign of what was coming and has changed the political tone. And populism has had a more meaningful impact on the political framework that has leaked through to policy and markets, but mostly on the bond market side. Populists almost always raise deficits and take a more protectionist approach to trade, both long-term policies that put upward pressure on interest rates. Predominantly on the right, it is often heavily nationalist, but sometimes on the left as well.

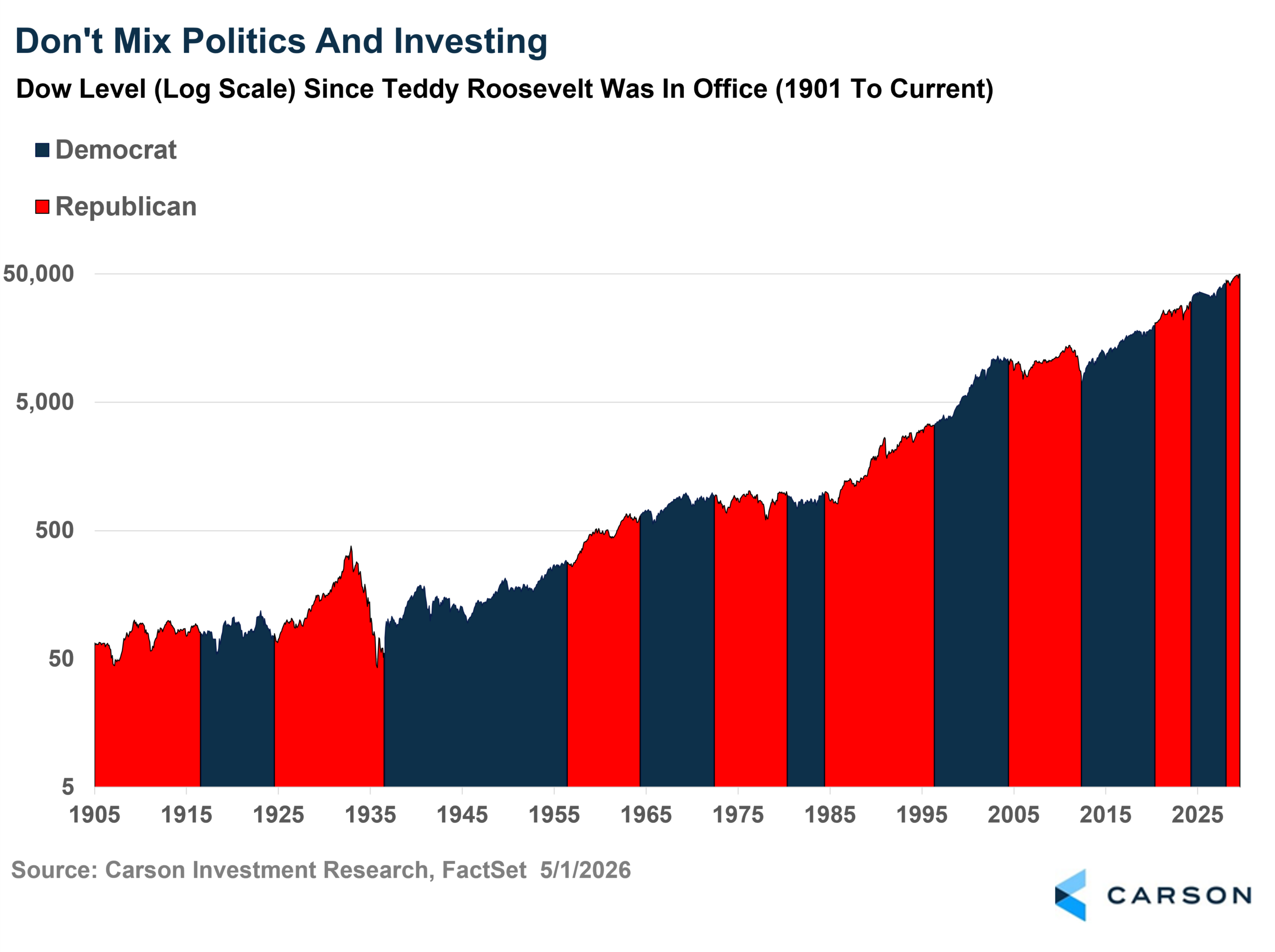

Political Risk Is Slow Moving

It is a basic principle of investing for me and my colleagues that mixing market views and political views typically leads to poor investing decisions. It’s all but impossible to make a statistical case that Democrats or Republicans are better for markets. There’s a small but meaningless statistical edge for Democratic presidents and a Republican or mixed Congress. One reason may be that a priority Republicans and Democrats share is a tilt toward policies that pull forward growth and pump up the economy. They have different approaches to achieving that goal, but the intent is the same.

Markets generally respond to what they think will happen over the next six months and then over the long run. Neither is a timeframe that is easily exploitable from a market perspective. Policy self-corrects, either within an administration (tariffs, Iran war for the current administration), through political checks and balances, or finally in the electorate’s ability to throw the bums out if they’re not doing a good job. That doesn’t mean that policy doesn’t matter. It just means it happens over a timeframe that is hard to exploit.

Pulling it all together, Brexit was a significant macroeconomic event that signaled a shift in global politics. It had an immediate impact on markets, but it was not easily investable, if investable at all. It had a longer-term impact on some markets that may have been predictable, but at most might have led to a prudent shift in positioning. The best approach may have been to avoid overreaction, focus on policy only to the extent there is a real connection to markets, keep the analysis apolitical, and take an incremental approach because the connections are there, but tenuous. Want to see how we do that? Watch for our Carson Investment Research’s Midyear Outlook, coming to you in just a few weeks.

For more content by Barry Gilbert, VP, Asset Allocation Strategist, click here.