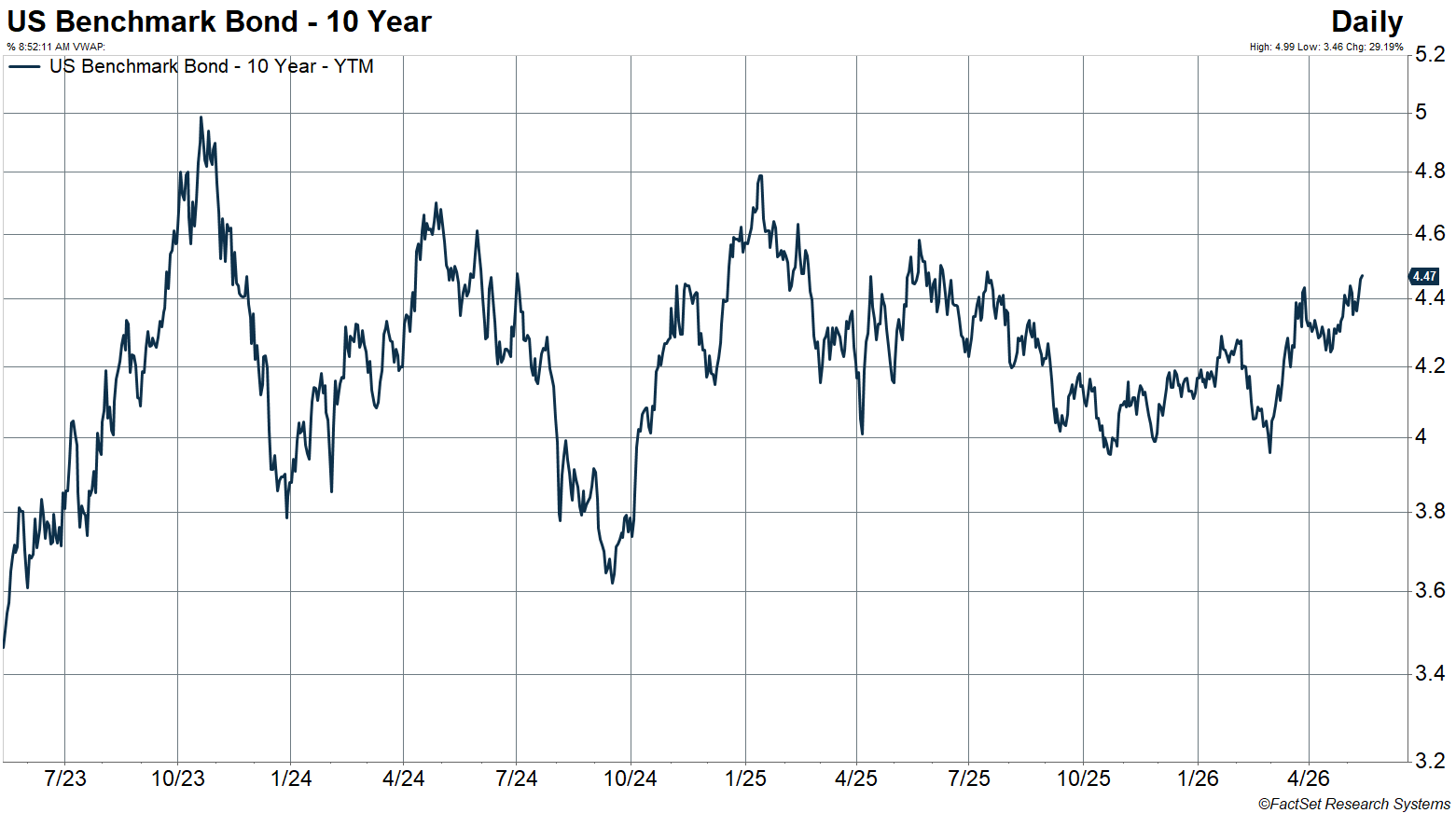

Yields have been on the rise for the last few months. On February 27, the day before US hostilities with Iran began, the 10-year Treasury yield was 3.96%, just 0.01% above its low dating back to early October 2024. Since then, the 10-year yield has climbed nearly 0.50%, closing at 4.47% on May 13, the highest level since July 2025.

Because starting yields were high this year, that hasn’t done too much damage to broad core bonds. The Bloomberg US Aggregate Bond Index, an index of investment-grade bonds, is down 0.1% year to date as of May 13. While this isn’t positive territory, it remains near flat thanks to high starting yields. At the same time, the Bloomberg 1-3 Month Treasury Bill Index looks better at a +1.3% return year to date with much less volatility. This return environment squares with our recommendation in our 2026 Outlook to keep about 1/3 of fixed-income allocations in short-maturity bonds.

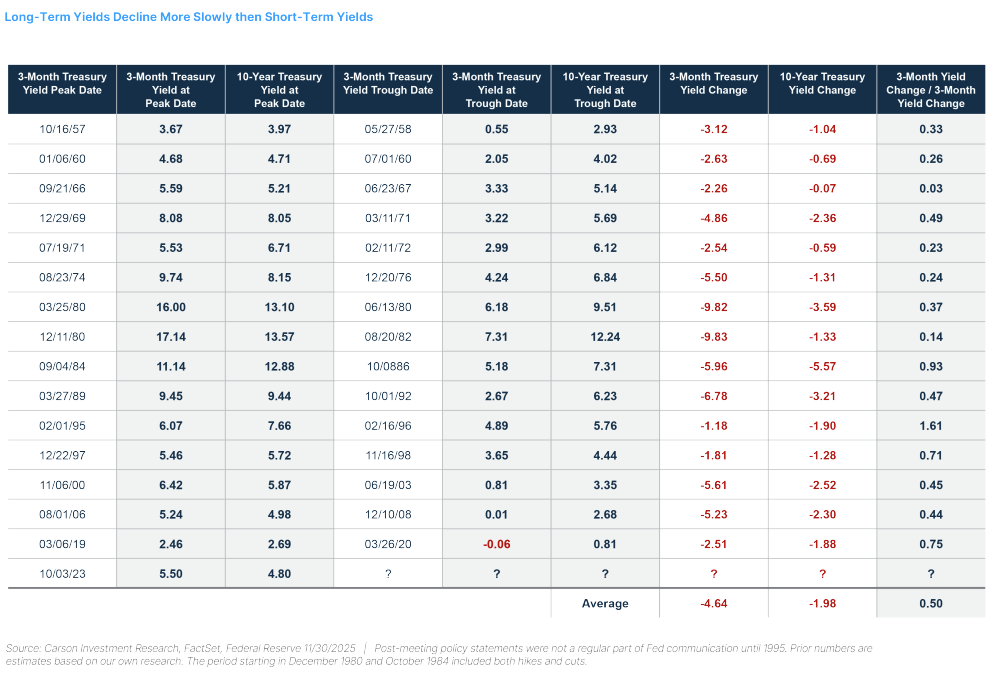

In our 2026 Outlook, our view was that even if the Fed cut rates, we didn’t expect the 10-year Treasury yield to show its historical sensitivity to lower short-term yields. (Historically, over full major rate-cutting cycles, the 10-year Treasury yield has dropped about half the amount of the three-month Treasury yield, as shown in the table from our Outlook below.) In fact, despite the expectation for one or more rate cuts, we said we expected the 10-year Treasury yield to actually climb modestly, targeting around 4.25%.

The inflationary expansion that drove our 4.25% yield target has largely played out as expected, but there are some important new circumstances to reckon with. The conflict in the Middle East was not priced into anyone’s expectations heading into 2026. If the conflict had been brief, its impact on rate expectations would have been minimal. But the length of the conflict and Iran’s closure of the Strait of Hormuz have shifted expectations while leaving the basic framework unchanged. Our starting point is still inflationary growth, but with inflation expectations higher and growth expectations somewhat lower. A tailwind from the Fed cutting rates has become unlikely, and some fiscal stimulus has been offset by higher costs, for energy in particular. On the other hand, investment in artificial intelligence has outpaced expectations, and the labor market has seen some recovery.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

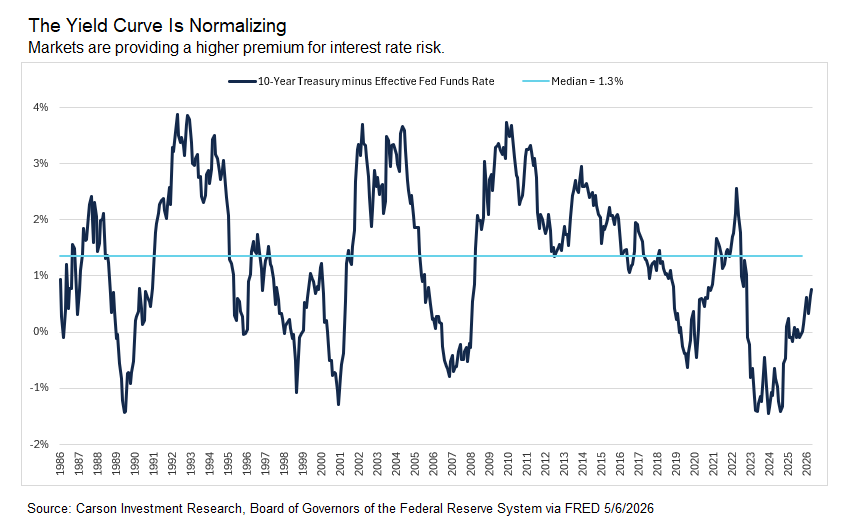

This has helped the yield curve, the difference between long-term and short-term rates, normalize, making considerable progress toward the long-term average of a 1.3%-point spread between the 10-year Treasury yield and the effective fed funds rate. A steeper yield curve means that the extra compensation for taking on interest rate risk is rising. That compensation is partially justified—investors should demand a higher premium when inflation uncertainty increases (read more about that here). But it does make intermediate- to longer-maturity bonds more attractive in the long run, since yields are the main driver of bond returns. But there is still potential for more bond volatility in the near term.

Given our already cautious view on rates, we wouldn’t adjust our 10-year target much from our view in the Outlook. Much of what we’ve seen is markets catching up with our view, although not entirely through the mechanism expected. It does make sense to change the year-end target for the 10-year Treasury to 4.5% with a bias toward lower outcomes over higher. But even if we see progress in the Middle East, inflationary pressures are likely to get worse before they get better. Since markets are forward-looking, some of that is already priced in. Just based on normal volatility, it wouldn’t be at all surprising to see the 10-year yield press higher before settling back towards its end-of-year level.

Put it all together, and it means that for those who have been meaningfully underweight bonds relative to cash, it makes sense to begin adding core bonds back to a portfolio opportunistically. If the 10-year yield were to breach 4.6%, we would consider moving more aggressively. But this should be viewed from the perspective of an environment that we think will continue to favor stocks over bonds and “diversifying diversifiers,” such as natural resources, managed futures (a trend-following strategy that can provide exposure to different asset classes, including commodities), and some lower-volatility stocks. But given these views imply a bond underweight, we think targeting the weight in core bonds with a high-quality bias makes sense, rather than our 2026 Outlook view of about 1/3 of the bond allocation in cash-like short-maturity instruments.

For more content by Barry Gilbert, VP, Asset Allocation Strategist, click here.

8929432.1. – 14MAY26A