Today, we tackle a topic that we don’t write about a lot relative to its importance—municipal bonds.

Why are munis important? A basic principle of investing (and one of the most ignored), Investment outcomes potentially should not be evaluated on returns but on the returns that you keep—returns after taxes. This is where municipal bonds become attractive. Most municipal bonds are exempt from federal taxes (and state taxes in the state where they were issued). Note that Treasuries are exempt from state taxes, so in high-tax states, the advantage of municipal bonds versus Treasuries may shrink when using a diversified portfolio of municipal bonds from multiple states. You can address this by emphasizing municipal bonds issued by the state in which you reside.

I’ll add a comment here that, while often ignored or given insufficient attention, Carson pays close attention to after-tax returns, both in our investment management and in how we deliver financial advice. Using municipal bonds the right way is just the starting point. If you want to learn more about what Carson can do around taxes, I recommend following Debbie Taylor, Managing Partner and Chief Tax Strategist at Carson Wealth.

Back to our topic, when investment professionals compare the yield on munis to other fixed-income vehicles, especially Treasuries, they often look at the munis’ “tax equivalent yield” to compare apples to apples. In truth, I believe this is something we should consider with every investment decision, because it makes a big difference. Looking at munis as an option is a good starting point.

Here’s where it gets complicated. Federal tax rates vary from person to person, ranging from a marginal tax rate of 0% to a top marginal tax rate of 37.0% + 3.8% for net investment income tax (“NIIT”), or 40.8% all in. That means the value of the tax benefit you get from munis will vary depending on your tax rate.

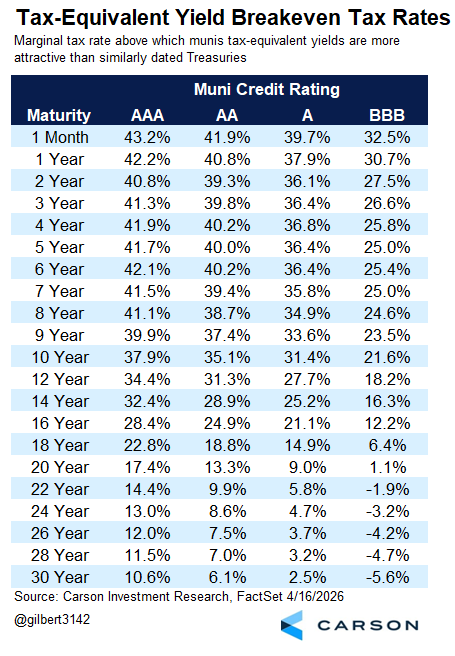

So here’s a table we built to look at the “marginal tax rate” breakeven for munis versus Treasuries (ignoring the state tax component). This is the rate above which the tax-equivalent yield for munis is more attractive than similarly dated Treasuries. While the data here are framed as “breakeven tax equivalent yield,” the lower the number, the greater the tax-equivalent yield of munis relative to Treasuries, and the larger the after-tax yield advantage of munis. The more attractive breakevens do come at a cost, discussed more below. As you move down the chart, you are taking on more interest rate risk (but so are comparable Treasuries). As you move to the right, you assume greater credit risk.

Two things stand out on this table. First, it’s not a surprise that tax-equivalent yield breakevens are more attractive as credit risk rises. But it’s also important to recognize that credit risk doesn’t mean the same thing for municipal bonds as for corporate bonds. Historically, corporate bond default rates are an order of magnitude higher (read: more than 10x higher), and recovery rates (what you get when there is a default) are lower for corporates. Also, keep in mind that Treasuries have lost their AAA rating (the highest rating) and are now AA, although I don’t think that’s actually an accurate assessment of their credit risk, and that Treasuries are still the best proxy we have for what traditionally gets called the “risk-free rate,” although this only refers to default risk.

Second, breakeven tax rates right now aren’t great at short maturities but improve rapidly as you move to longer maturities. That’s a double-edged sword. Breakeven yields become more attractive, but you have to take on more rate risk.

In my opinion, the best way to handle rate risk is to be a strategic investor and understand that, if you hold a bond to maturity (and it doesn’t default), you know the bond’s price at maturity no matter what rates do. Prices only move in the opposite direction of yields in the short term (defined here as under a bond’s maturity). Over a bond’s maturity, they are entirely indifferent—the bond’s price will be at par at maturity no matter what. That movement toward par is baked into the yield (along with the coupon payments), so the yield is a very strong estimate of the bond’s return over its lifetime. The movement to par is a very slow but very powerful force that, over the life of a bond, dominates rate risk as traditionally understood.

That means, over the short term, short-maturity bonds have low interest-rate risk (sensitivity to rate changes), and the risk grows steadily as maturities increase. But over the lifetime of a longer-maturity bond, short-term bonds have a lot of return uncertainty because they have to be regularly rolled over into new bonds as they mature, and you don’t know what future rates will be. For longer maturity bonds, the price at maturity is known.

Keeping this in mind, here are three behaviors that I believe are very important for being an investor in longer maturity bonds:

- Pay close attention to the yield going in. Don’t buy a long-term bond whose yield is unattractive because that yield is about what you’re going to get. Short-term investors can speculate on the price movements of longer maturity bonds, but that’s not the point here.

- Don’t treat bonds as a momentum instrument. If you’re holding to maturity, the higher yields you get after bond prices fall make them more attractive. The lower yields you get after bond prices rise make them less attractive. This was a mistake many investors made coming out of 2020, when bonds were a spectacular diversifier during the Covid market crash, but yields were ultra-low. Even many investment professionals I worked with at the time made this mistake, including the head of the department I was in, who actually made a rule limiting our portfolio managers’ ability to mitigate interest rate risk by using shorter maturity bonds. Needless to say, the timing of that decision wasn’t good. The point isn’t to cast blame but to highlight that even seasoned investment professionals can struggle with the distinct characteristics of bond investing.

- If you own longer maturity bonds at an interest rate that meets your needs, you absolutely have to be patient. Don’t expect much more than the yield when you buy. Don’t expect much less. And keep firmly in mind that you know what the bond will be worth when it matures, no matter how much the price may drop in the short term. You just need to ignore the path to getting there.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

One More Risk To Keep In Mind: Inflation

An additional thing to potentially keep in mind is inflation risk. As we’re written several times over the past few years, we believe we’re currently in a higher inflation regime with more inflation volatility – which is not to say we predicted the energy shock from the current Middle-East crisis, but it’s just another one in a series of inflationary shocks over the past few years (Covid supply-chain crisis, Russia-Ukraine energy shock, tariffs, and the immigration stall culling labor supply).

From the end of 2020 through March 2026 (5 years and 3 months), inflation as measured by the Fed’s preferred inflation metric, the personal consumption expenditure (PCE) index, has averaged 4.1% (annualized). Over this period:

- The Bloomberg Aggregate Bond Index had an annualized return of -0.4% (pre-tax)

- The Bloomberg AMT-Free National Municipal Bond Index had an annualized return of 1.1% (after-tax)

- The Bloomberg Municipal Short-Term Bond Index had an annualized return of 2.2% (after-tax)

As you can see, none of these bond-market baskets “beat” inflation. Obviously, that’s because of the low starting yield in 2020 and the surge in inflation after. The picture looks better if you start the clock in January 2023 – inflation have averaged 3.0% since then (3 year and 3 months), which is still hot. But bond market returns have exceeded inflation:

- The Bloomberg Aggregate Bond Index has had an annualized return of 4.3% (pre-tax)

- The Bloomberg AMT-Free National Municipal Bond Index had an annualized return of 4.0% (after-tax)

- The Bloomberg Municipal Short-Term Bond Index had an annualized return of 3.2% (after-tax)

So where are we today? There’s a chance inflation runs around 3-3.5% over the next few years. So, balance that with potential starting yields (the “yield-to-worst”) for these bond baskets:

- Bloomberg Aggregate Bond Index: 4.5% (pre-tax)

- Bloomberg AMT-Free National Municipal Bond Index: 4.1% (after-tax)

- Bloomberg Municipal Short-Term Bond Index: 2.7%

As you can see, the longer duration muni bond index looks relatively more attractive, both from an after-tax yield standpoint and relative to expected inflation as well. Of course, as I noted earlier, you are taking on interest rate risk, and so you have to be patient.

For more content by Barry Gilbert, VP, Asset Allocation Strategist, click here.

8879858.1. – 16APR26A