“If pro is the opposite of con, does that make progress the opposite of Congress?” -famous quip

Back on January 3rd, to mark the swearing in of the 119th Congress, we shared seven risks to our bullish policy outlook. That was still 17 days before inauguration day. Now we’ve seen the new administration’s policies gel for a little over two months and we’ve learned a lot since then, so we thought it was time for an update.

Two quick items for context before we dive in. Keep in mind that our sole focus when discussing policy is its impact on markets. Markets aren’t the arbiter of good and bad policy, and our aim isn’t to evaluate policy broadly. In fact, if we tried to that, we think we would do our job less well. Letting politics influence investing decisions rarely goes well.

Second, while we’re focusing on policy risks here, we do think there still are policy opportunities. In general, lower taxes, deregulation, higher fiscal deficits, and (although at risk) lower interest rates are all policies that tend to have a positive impact on corporate profits, which in turn supports stock gains. The sequence of policy (tariffs and DOGE first) has pushed opportunities back. But there are deadlines that mean there will be a major push for a large fiscal package by the end of the year. Most key provisions of the 2017 Tax Custs and Jobs Act (TCJA) expire at the end of 2025 (although not the lower corporate tax rate), confronting Congress with the prospect of a fiscal cliff with mid-terms less than a year away. While new legislation will be complex and narrow majorities in the House and Senate leave Republicans little room for error, the legislation can be passed under the “reconciliation” process, which does not require a filibuster-proof supermajority in the Senate.

Overall, the balance between risks and opportunities has shifted since January 3 with risks rising and some opportunities fading. We underestimated the depth of the Trump administration’s commitment to tariffs, but it’s important to keep in mind that final policy is still evolving. DOGE was an unforeseen risk, and while we have been impressed with the energy to reduce government bloat, the process has at times seemed reckless and not even entirely aligned with achieving its stated goal. But perhaps most of all, we think the opportunity to unleash “animal spirits” has been largely squandered, as judged by consumer sentiment, business sentiment, and the markets themselves. We did see a post-election surge in sentiment (and markets), but that has since largely evaporated. At the same time, the change in sentiment has had little to no impact on hard data yet, including earnings. Sentiment matters only if it shifts behavior.

The divide between hard and soft data isn’t new. The Biden administration was also faced with waves of negative sentiment as inflation reached generational highs in 2022, but real GDP has averaged 2.9% annualized over the last 10 quarters and 3.2% over the last four years. That compares favorably not only to the first Trump administration (2.8% excluding 2020 to take out the impact of the pandemic) but also the Obama administration (2.0%) and the eight years under George W. Bush (1.9%). Whatever you think of Joe Biden’s capacity to lead, the Biden administration has been the steward of the best economy since Bill Clinton, although that’s far from saying they were responsible for it.

On to the topic at hand. Here is our reevaluation of potential policy mistakes that could undermine our bullish policy outlook.

Risk 1: Tariffs Push Inflation Higher

Change since January 3rd: Higher Risk

Risk Assessment: High

Immediate Market Impact or Slow Burn?: Immediate Market Impact

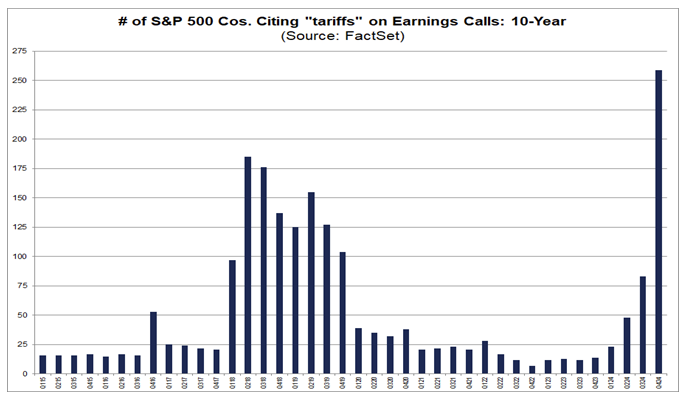

Tariffs are coming, but as we’ve already seen, the specific policy can change overnight and we still don’t know exactly what the policy will be so we still need to take a wait-and-see approach. Just take tariffs on Mexico and Canada. On January 20, (inauguration day) the president said tariffs would be implemented on February 1. Then it became February 4. Then they were delayed by another month. Then later another month to April 2, but the president then reversed course and said March 4. On March 3, Commerce Secretary Harold Lutnick said it’s possible the tariffs won’t go into effect, but the president then said they would that same day. Tariffs provisionally went into effect March 4 but were then delayed on March 6 to April 2. Have you followed all that? And that’s just Mexico and Canada.

Thus far, tariffs on China have been raised to 20%; a 25% tariff has been implemented on all steel and aluminum imports; the 25% tariff on Mexico and Canada right now is still scheduled to go into effect on April 2; and nebulously defined “reciprocal tariffs” are also supposed to go into effect April 2.

We know already that markets are sensitive to tariff news, as it was the main driver behind the February 19 – March 13 S&P 500 Index correction, although we’ve seen a nice rebound since. We also know that the policy uncertainty created by tariffs is having an impact on Federal Reserve policy and businesses.

At the same time, the lack of clarity on tariffs makes it hard to gauge the longer-term impact. We have seen increases in both actual measures of inflation and business and consumer inflation surveys. We’ve also seen a rise in imports (which is a negative in GDP calculations) as importers try to get ahead of tariffs (which has contributed to higher prices), but that particular negative impact is likely to unwind. It’s also important to keep in mind that tariffs have a one-time impact on price levels but do not directly contribute to prices continuing to climb higher, and in that sense don’t contribute to inflation. (Although we also know consumers are sensitive to price levels too.)

Overall, tariff policy remains a meaningful risk and more significant than we originally expected.

Risk 2: The Federal Reserve Keeps Policy Too Tight

Change since January 3rd: Higher Risk

Risk Assessment: High

Immediate Market Impact or Slow Burn?: Immediate Market Impact

This one is intimately tied to tariff uncertainty, which has handcuffed the Federal Reserve. The current median forecast by the Fed is for two rate cuts in 2025 while the market-implied expectation is just shy of 2.5. For an in depth look at last weeks Fed meeting see Carson’s VP, Global Macro Strategist Sonu Varghese’s excellent analysis in “The Fed Is Stuck Waiting, and That’s a Problem.” There was some market upside from the last meeting, but only in that the Fed raised their inflation expectations without lowering the expected number of rate cuts. At the same time, the Fed is not in a hurry to cut amid a lot of uncertainty, and that creates on-going stress that could weigh on growth for cyclical areas of the economy.

Remember, a fed funds rate target of just 2.25 – 2.50% nearly broke the economy in 2018 – 2019, something President Trump correctly pointed out at the time, and low rates, even after some tightening, were still a major tailwind. Well, right now the target fed funds rate target is 4.25 – 4.50%, two full percentage point higher. The economy has been incredibly resilient despite high rates, but cyclical sectors, including housing, small businesses, and manufacturing, have been under pressure and the labor market, while still strong, has exhibited some underlying risk, although it remains stable for now. Productivity growth, which is supported by a tight labor market and has been an important contributor to recent growth and may also be damaged by policy that is too tight if it leads to a rise in layoffs.

We think the current expected slower path of rate cuts is very unlikely to push the economy into a recession on its own, but it will make the economy more sensitive to other shocks.

Risk 3: Unpredictability Restrains Animal Spirits

Change since January 3rd: Higher Risk

Risk Assessment: High

Immediate Market Impact or Slow Burn?: Immediate Market Impact

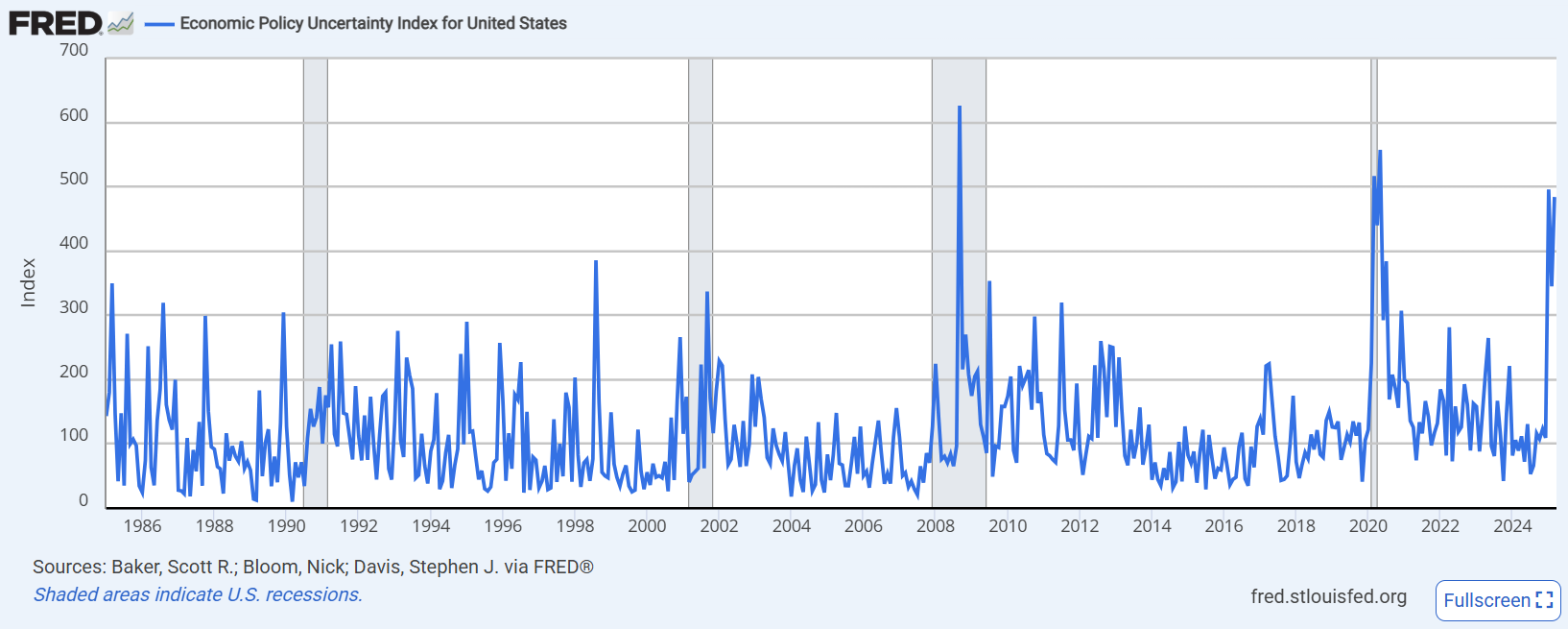

Unpredictability is part of Trump’s MO and he is capable of deploying it very effectively. But while unpredictability can be powerful when negotiating, it can create a difficult environment for businesses. We’ve already seen this come through in increased mentions of tariffs in earnings reports and surveys such as CNBC’s surveys of business CFOs. Companies put a lot of capital at risk based on expectations of future profits, and generally want policy clarity. Businesses also do not want a president who interferes with capital markets in a fit of pique. An uncertain policy environment can make it harder to do business, although sometimes it does also present opportunities. Initially viewed as a small risk, it’s clear uncertainty around some policies has weighed on business sentiment. Every policy environment has its element of unpredictability. But with the last Trump administration, for example, we did see tariff policy uncertainty weighed heavily on business investment in 2018-2019 and put a dent in the expected supply-side impact of the Tax Cuts and Jobs Act. The Fed has cited four areas of policy uncertainty weighing on its outlook, trade, immigration, fiscal policy, and regulation. Businesses are facing similar challenges. Some of these (fiscal policy, regulation) continue to have likely eventual upside for businesses, but the uncertainty still makes it hard to do business.

Note that policy uncertainty is often not a negative for markets because markets tend to be forward looking and high or peak uncertainty could occur near market lows. But the uncertainty represented here is more focused on the ongoing impact on the ability to do business that has not fully taken hold rather than the broad sense of uncertainty that has already led to economic disruption. September 2008 or March 2020, other times when uncertainty has been high according to a measure shared by the Fed, aren’t really analogous to the current situation. Where it may be somewhat analogous is that policy uncertainty is so high right now that the actual impact as unlikely to be as bad as expected.

*NEW*

Risk 4: DOGE Inadvertently Breaks Something

Change since January 3rd: Higher Risk

Risk Assessment: Moderate

Immediate Market Impact or Slow Burn?: Slow Burn

From a market perspective, it’s hard to gauge the economic impact (and eventual market impact) of DOGE. While some cuts have been dramatic, given the scale of an entire economy it’s really the knock-on effects that would cause a true economic disruption. There are areas of the economy that are more vulnerable, for example the Washington, DC area and industries that rely most heavily on research grants (e.g. medical research). There’s also some risk, for example, of challenges in the disbursement of Social Security or other disruptions to the smooth functioning of government that can have an impact on people’s lives, but again that’s unlikely to matter a lot compared to the scale of the entire economy. Really, in itself the political risk is larger than the policy risk. But the aggressive cuts do introduce “known unknowns” that require some caution and add to the general environment of policy uncertainty.

Risk 5: Internal Division within the Republican Party Delays or Limits Policy Implementation

Change since January 3rd: Unchanged

Risk Assessment: Moderate

Immediate Market Impact or Slow Burn?: Immediate Potential Impact but Not Until Later

This is a policy risk that has a positive side. We noted during the election that markets tend to like mixed government. The spirit of compromise tends to get us better policy and helps avoid the ideological excesses of both parties. But we won’t have mixed government in 2025 and ideological excesses are making themselves felt.

However, the majorities in Congress are narrow. Republicans hold a 53-47 majority in the Senate, as well as the tie-breaking vote by Vice President Vance. Republicans currently have a 218 – 213 majority in the House with four seats vacant, two formerly held by Republicans and two formerly held by Democrats.

While we did not get divided government in November, there are some ways in which narrow majorities keep at least some of the spirit of divided government. Republicans will need their own moderates AND their most hardline conservatives to vote yes to pass policy. There could be a cushion should Freedom Caucus members hold up a bill, since some Democrats could be pulled on board to support a bill if they believe it is in their interest, but it would require some compromise.

Narrow majorities keep more checks and balances in place, but they also increase the possibility of legislative chaos and will make it more difficult to pass any bill that doesn’t have broad consensus among Republicans. Significant delays that disappoint policy expectations could lead markets to become impatient with Congressional infighting. The key date here is the end of the year deadline when major provisions of the TCJA sunset. Republicans are also well aware that the president’s party has lost House seats in mid-term years in 20 of 22 mid-term elections since 1938.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Risk 6: Immigration Policy Stunts Economic Growth

Change Since January 3: Unchanged

Risk Assessment: Moderate

Immediate Market Impact or Slow Burn?: Very Slow Burn

In my view, this is the most underrated risk but still secondary to those listed above it when it comes to the absolute level of risk. Clearly there are some genuine problems with current immigration policy. But the extent to which the resilience of the US economy depends on its ability to attract and absorb global labor is often underestimated. In fact, I would say the two key factors that have led to the structural advantage the US has over other developed economies is a more business-friendly overall policy environment, including labor market flexibility, and its history of acting as a destination of choice for immigrants.

It’s hard to determine the level at which tighter immigration policy becomes a genuine risk, and before it becomes a risk there certainly may be areas where reforms would provide benefits. The aim here is not to determine what the right immigration policy should be, but just to highlight that at some point tight policy can start to impact the economy and markets.

Thus far, the rate of deportations seems to have accelerated only modestly from the Biden administration, although the Trump administration has raised the media profile of deportations and some disputes in the courts have received a lot of attention. However, the numbers are difficult to gauge because the Trump administration has ended the regular reporting on deportations by ICE and the Department of Homeland Security.

However, net immigrant in-flows have fallen dramatically according to estimates from Goldman Sachs, from an annualized pace of 1.7 million to 0.7 million based on data from December and February. That will have an impact on job growth, but it will also lower the job growth needed to keep the unemployment rate steady because immigrants also contribute to unemployment. But even with a steady unemployment rate, fewer jobs added will mean slower aggregate income growth, which is the primary driver of US economic growth.

Here are just a few of the reasons immigration policy could pose a risk from an economic perspective:

-If the current level of flow of earners falls due to immigration policy and the chilling effect on new immigration, there’s a direct impact on GDP. A dollar of lost income is a dollar of lost GDP. Policy that leads working immigrants to leave the US, or choose not to come in the first place, is the economic equivalent of exporting U.S. GDP growth to the rest of the world.

-There is a steep implicit regulatory burden on business from tight immigration policy, both by restricting their access to workers and making the cost of labor higher. Elon Musk’s and Vivek Ramaswamy’s initial support for expanding H-1B1 visas due to their contributions to US technology leadership was poorly received in some MAGA circles.

-A more restricted labor pool also has the potential to drive wages higher, posing some additional risk for inflation. This effect may be stronger with the prime age participation rate already near a record high. We think this risk is fairly small, but not non-existent.

Immigration reform is a positive goal, but also comes with some risks. How high those risks are depends on actual policy. It would take a fairly large mistake to have enough of an impact on the economy to weigh on markets, but the potential for a large mistake is non-trivial.

Risk 7: Fed Independence

Change Since January 3: Unchanged

Risk Assessment: Low

Immediate Market Impact or Slow Burn?: Immediate if it were to occur

I would consider this a very small risk, but with the consequences of a misstep potentially large. Trump has already put some pressure on the Federal Reserve to lower rates, although I would say he’s been fairly restrained. Comments on Fed policy in and of itself aren’t a problem. There are mechanisms that help maintain Fed independence. But if there is an effort to overstep or to appoint a loyal and partisan Fed chair when Jerome Powell (himself a Trump appointee) steps down in May 2026, markets will respond. This one is unlikely to be a slow burn. If Trump oversteps, I would expect the market response to be unmistakable. If Trump floats test balloons that cause market jitters but can easily be stepped back, it’s not an issue. But a genuine threat to Fed independence that cannot be walked back could be a problem. This may also arise through efforts to call into question the constitutionality of independent agencies, which is a potential stepping stone to removing Fed independence.

Interestingly, Fed policy (although not necessarily Fed independence) is a place where Trump’s inclination (lower rates) is most directly in conflict with Project 2025, which wanted more emphasis on the inflation side of the Fed’s dual mandate and in fact recommended removing the “maximum employment” mandate altogether. There are other areas where they are more aligned, including potentially limiting Fed independence, but I would characterize Project 2025 as generally hawkish on Fed policy while Trump is quite dovish, especially when he’s in office.

*to be removed*

Risk 8: Deregulation Clashes with the Supreme Court’s Chevron Reversal

Change Since January 3: Lower

Risk Assessment: Low

Immediate Market Impact or Slow Burn?: Very Slow Burn

If I kept this one, I would expand it to slowing policy implementation more generally. But even this I don’t see as a risk directly to markets. Trump has been testing policy limits so actively that the courts have been busy, and making the implications of Chevron central in that context was short sighted. Still, the net effect of policy working its way through the courts typically has little to no immediate market impact, since it’s part of the normal functioning of the federal judiciary to take up these kinds of questions. There are some potential issues that could be market moving if they found their way up to the Supreme Court (for example Fed independence or election-related decisions). But outside of that or a genuine constitutional crisis, I doubt what happens in the courts will have a direct takeaway for markets. Should we review all these policy risks again in the future, this one is coming out.

There you have it, seven policy risks that we’ll be watching for in 2025, with tariff unpredictability and the Fed’s rate decisions still the most meaningful, but a few others to keep an eye on as well. Our view on policy and “animal spirits” in our Outlook 2025 was that there was the potential for there to be an added tailwind from animal spirits, but our overall view was not dependent on it. The opportunity for the potential tailwind has not been entirely lost, depending what happens with the tax bill, but it hangs by a thread and disruptions have been larger than expected. We have informally downgraded our GDP expectations with the potential upside we saw likely off the table. We are probably looking right now at something more like 2% GDP with risks more to the downside (but not recessionary) for 2025 versus something more like 2.5% with risks to the upside when we made our initial assessment. But we will continue to monitor both risks and opportunities for how they are playing out.

For more content by Barry Gilbert, VP, Asset Allocation Strategist click here.

7785646-0325-A