Bloomberg reported this week that the number of listed, actively managed ETFs now exceeds passive ETFs for the first time, although assets in active ETFs remain significantly lower. This milestone comes as the “ETF as a share-class structure” gains traction, potentially paving the way for even more active strategies to enter the market. There are many benefits to the ETF wrapper that hopefully the industry is well aware of today, but I believe the biggest benefit propelling the growth of active ETFs is unquestionably taxes. I will illustrate this in a couple of ways.

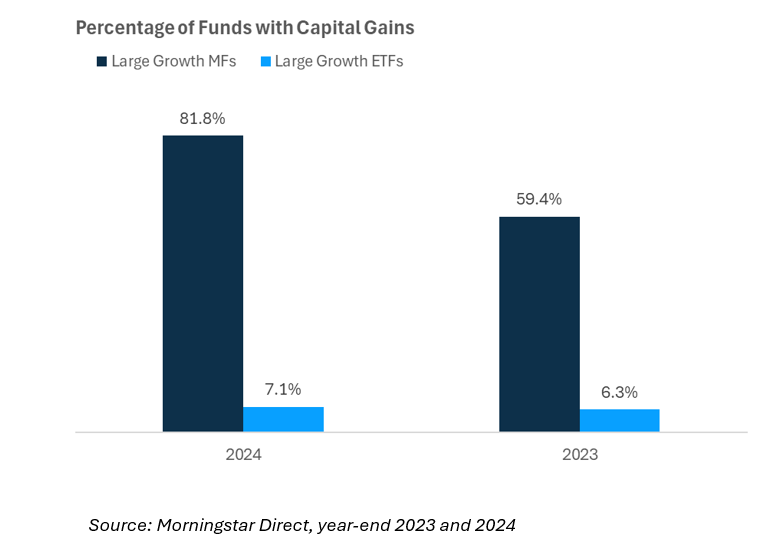

One of the starkest illustrations of the tax benefits of ETFs—particularly active ETFs—is the sheer number of mutual funds paying out capital gains as compared to ETFs. The chart below shows this visually for the Large Growth category. A whopping 82% of large cap growth mutual funds (there were more than 285 funds live in 2024) paid out a capital gain of some kind last year. For the same category of ETFs, only 7% of products issued a capital gain and many of those were small or had some type of special situation (reorganization, closure, etc.).

Illustrating this further, we can look at an example of one of our favorite strategies in the large cap growth space. Distributions for the past couple of years from the mutual fund are shown below. Despite sizable inflows into the mutual fund (large outflows typically lead to large capital gains), there were significant distributions from the fund on two different dates in 2023 and 2024. Why are we talking about taxes in June? This is why! Not every fund has a fiscal year that corresponds with the calendar year, and many will try and spread out their capital gains payments if they know of large distributions that need to be passed through. In this case, a 5.4% distribution was paid in September, followed by another 0.82% distribution in December with part of that as short-term capital gains (even more tax inefficient). This is on top of dividend payments, although these tend to be small in the large growth category.

While the ETF version of the strategy is not an exact clone of the mutual fund, there’s a 1.0 correlation between the mutual fund and the ETF, yet they have very different tax results. The ETF version has never paid a capital gain since inception in 2020. As a result, while more than 1% of the mutual fund’s return has been lost to taxes (tax cost ratio), the tax cost is just rounding error for the ETF. Those differences add up and compound over time for taxable accounts.

ETF’s ability to redeem shares in kind consistently (mutual funds can do it as well but the logistics are much more complex) gives them a significant tax advantage. That being said, ETFs are not a tax panacea and will distribute capital gains from time to time. This is particularly true if the ETF is seeing significant outflows and the issuer is smaller and doesn’t have the necessary trading contacts to consistently fund outflows in kind. This is where certain aspects of our due diligence process can avoid fund closures and capital gains potential, amongst other issues.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

In the same vein, ETFs do distribute income in a number of ways just like any pass-through vehicle (1940 act or otherwise), and those distributions should be understood from a tax perspective. Here is a quick review of the main types of distributions from the ETF wrapper:

- Ordinary income – Corporate bond income, options-based income, non-qualified dividends, and any potential short-term capital gains are all passed through the ETF wrapper. These products should be held in qualified accounts to avoid the full taxation of distributions.

- Qualified dividends – Certain dividend and preferred stock ETFs will distribute income at the lower long-term gains rate. Preferred stocks will generally see 50-90% in qualified dividends (QDI) depending on composition.

- Return of capital – MLPs, REITs, and some options-based income products will distribute income that is return-of-capital (ROC). These distributions are not taxable in the year they occur, but rather lower the cost basis of the position you own and defer the taxes. If the basis is exhausted (i.e. you hold the position long enough to reduce the basis to zero), the distributions then become taxed at long-term gains rates.

Despite it being mid-June (already), taxes are always an important part of the investing picture. ETFs make the conversation a lot easier and generally avoid the unpleasant surprises that come alongside the majority of traditional mutual funds. However, proper use of income-generating ETFs is a very important part of a client’s overall asset allocation.

8087773.1.-6.18.25A

For more content by Grant Engelbart, VP, Investment Strategist click here