Because of the government shutdown, government data on the labor market has been absent lately but the trend in job growth has been clear. Labor force growth has been slowing, and today we’ll take a look at some of the pieces contributing to that. But be careful with that sentence—slower growth is not the same as contraction and based on the available data the economy is muddling along just fine. And with rates coming down, deficit-financed fiscal stimulus on the way, an AI infrastructure boom, and still quite healthy household balance sheets we don’t see that changing. Also throw in that headwinds from tariffs have calmed (see thoughts on that here), and the risk of disruption of the status quo has come down as well.

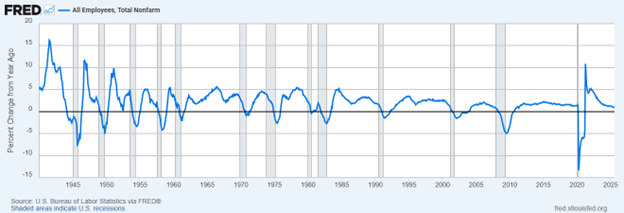

But back to the starting point: Job growth has slowed to a pace of about 29,000 per month over the last three months (June–August). The three months prior to that (March–May) averaged 99,000 per month. At the start of the year, job growth was running at about 125,000/month. Analysis from Goldman highlighted several drivers behind this, and it’s worth taking a look at the analysis, in part because it tells us if this slowdown is temporary or not. Payroll growth matters for the economy because even if the unemployment rate doesn’t go up, fewer new jobs are created and that means overall aggregate income growth is going to slow, which is the main driver of the consumer spending that makes up about 2/3 of the economy (at least until consumers take on a lot more debt but that’s not happening right now because of elevated interest rates).

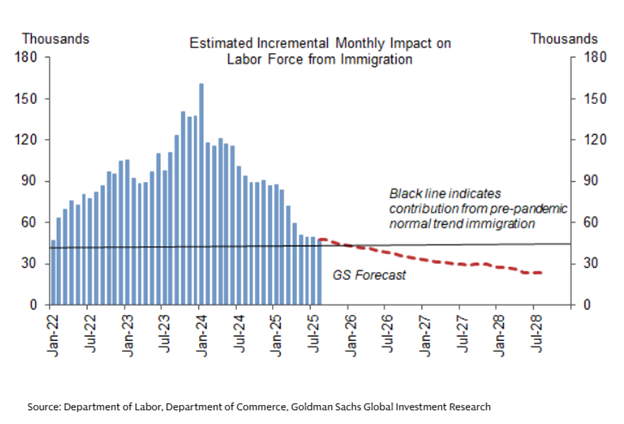

Driver #1: Immigration Slowdown

Net immigration is now running around 0.5 million/year, a big slowdown from the last two years. At its peak in 2023, it was three million. As a result, the contribution to monthly labor force growth from immigration has fallen from 90,000 at the start of the year to 40,000 in August. Goldman expects it to fall even further in the months ahead. (This isn’t an assessment of the policy decisions that have led to that decline, just the impact on job growth.)

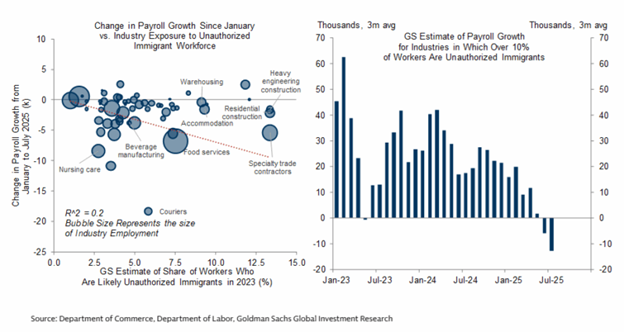

Corroborating this is the fact that industries that rely on undocumented immigrant workers have seen larger declines in job growth since the start of the year. Goldman estimates that employment growth in industries where unauthorized immigrants account for over 10% of the workforce has fallen from ~20,000/month in January to a decline of -10,000/month in July.

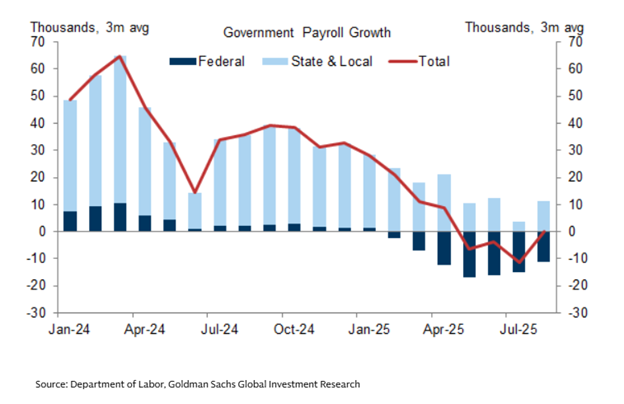

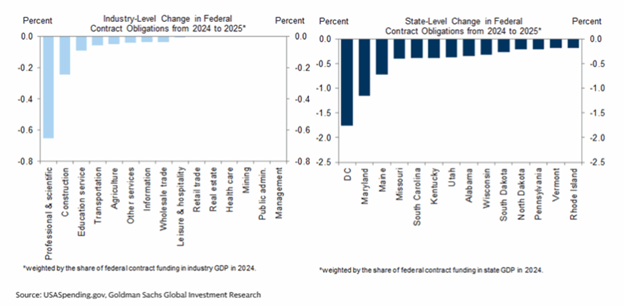

Driver #2: Reduction in Government Jobs

Another drag on payrolls is federal government job growth is now negative (again, not a policy assessment), while state/local government payroll growth has fallen from 30,000/month at the start of the year to 10,000/month in August. As you can see in the chart below, the big drag is from the state/local side (light blue bars), even if some of this may be a consequence of federal policy. (Keep in mind that state and local payrolls are about 7x the size of the federal payroll (not including the military.)

In fact, private payroll growth has also been selectively hit due to a drop in government funding. There’s been a sharp pullback in private payroll growth in professional and scientific services, construction, and private education services industries, and in Washington DC and Maryland (where many federal workers live) since the start of the year.

Driver#3: AI Adoption

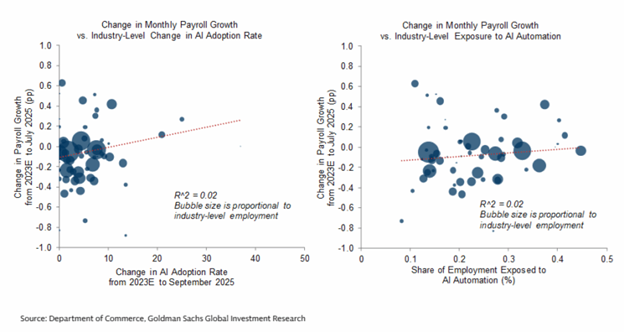

There is an active debate around whether AI is currently destroying jobs (and an even more active debate around what the future holds). The analysis from Goldman suggests not. They tested whether a higher AI adoption rate or a larger share of workers specializing in tasks that are more susceptible to automation by AI technology within an industry is associated with a more significant decline in job growth. And the tests don’t really show much correlation.

In other words, there’s not much evidence from industry-level data that AI exposure is currently leading to slower job growth.

Drivers #4 and #5: Tariffs and Macroeconomic Uncertainty

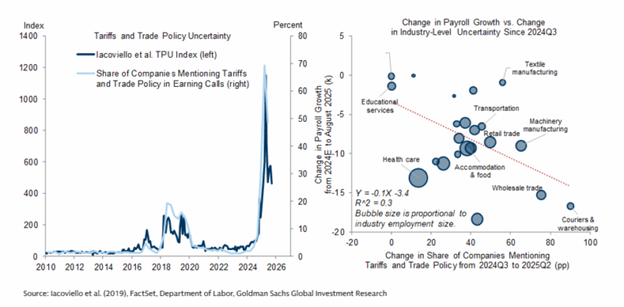

I’ve been skeptical that tariffs have directly resulted in job losses (mostly because we’re nowhere near the worst case scenario, or even the pre-Liberation Day base case scenario for tariffs). Still, Fed surveys point to companies saying they are reducing hiring as one of several cost-saving strategies to cope with tariff costs. But the direct impact of higher tariffs on hiring appears limited. The 30 goods-producing industries most negatively affected have reduced job growth only slightly this year. Goldman finds larger increases in tariff uncertainty since last year have been associated with declines in job growth across affected industries. Though again, this doesn’t have a huge aggregate impact, like say, the decline in immigration. Even in the right panel below you can see change in healthcare payroll growth declining relatively more than other industries, and that’s not directly a result of trade uncertainty. (Federal contract funding may play a role.)

There’s general macroeconomic uncertainty, especially with recession calls and consensus GDP forecasts being really low. But the outlook has improved since May, not least because a lot of the tariffs have been rolled back. But June-August is when we saw a marked slowdown in payrolls, and I’m skeptical that macroeconomic uncertainty is a big driver, at least not much more than generally is the case.

Altogether, slower immigration, reduced government hiring and federal contract funding, and elevated uncertainty have contributed about 100k to the recent job growth slowdown. There’s some evidence that AI adoption and tariff-related costs have had a localized impact in a few industries, these effects look fairly small so far.

But to close where we started, is the impact from these factors just temporary? Uncertainty, as we’ve seen, has already proved temporary. The AI impact we’ll leave as a known unknown, but for now if you include job growth from the AI infrastructure buildout you can argue that it’s actually been a net contributor given low job loss from AI replacement. With government jobs, it depends on whether we see further cuts (including funding cuts), including what’s happened during the shutdown. The effect might not be over yet but it’s winding down. And uncertainty around tariffs has stabilized.

That leaves us with immigration. Setting aside questions of what the level of immigration should be and how to implement policy (very complicated questions, granted), the impact of immigration is likely still on going. Part of that is because there’s still potential for additional policy escalation. Part of that is because a dollar of income corresponds to a dollar GDP and to the degree that income is exported (and not replaced by other workers, which is what we seem to be seeing), GDP slows and along with it labor demand. On top of that, policy can also create a chilling effect on future immigration, creating a larger labor pool deficit—flows matter. Then you can add in that some jobs immigrants do are hard to replace, whether because they are difficult and low paying (think agricultural workers) or require specialized skills that are in short supply (think technology).

We think robust labor growth in the current environment is very unlikely. But what we think is entirely feasible is avoiding the snowball effect that often happens as the labor force slows, supported by the factors listed up top. Yes, the president is pushing policy (deficit-financed stimulus, lower rates) that usually only starts happening in a sharp economic decline, but when that decline starts to happen it is often too late and the economy has clearly slowed from the near-3% growth we had in 2023 and 2024. Further, any policy debate aside, what’s unambiguous is these are policies that markets tend to favor, at least until the data starts moving in a compellingly negative direction. But even in the middle of a government shutdown data gap, the numbers we’ve seen are far from compellingly negative. That might be damning with faint praise, but when stimulus is flipped on that’s usually good enough for market.

Thanks to Barry Gilbert, VP, Asset Allocation Strategist, for his help with this blog

For more content by Sonu Varghese, VP, Global Macro Strategist click here

8534427.1.-23OCT2025A