“Only when the tide goes out do you discover who’s been swimming naked.” – Warren Buffett.

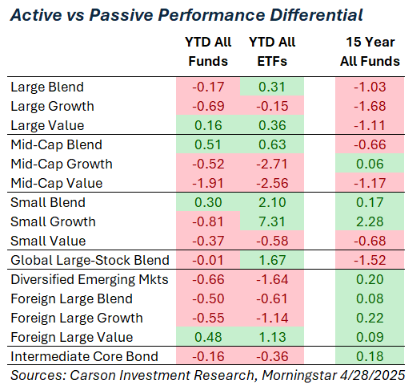

An apt quote at this part of the year, as we head towards the Berkshire annual shareholder meeting to pay homage to one of the best active managers of all time. The first four months of this year have revealed (pun intended) a lot about how investment managers have been positioned and managed risk. There are many ways to measure this, but one simple check-in is to look at the broad set of active managers in a particular category versus their passive peers. Not all of those passive peers track the same index, and some may even use a factor or smart beta approach – raising the bar even higher for active managers to outperform. The table below shows major Morningstar categories and the year-to-date performance of the active managers versus passive. A green number indicates active has outperformed in aggregate, while a red indicates passive has prevailed so far.

In short, the environment has been tougher than expected for active managers. Typically, during these periods, we see active managers start to shine through, but the trend change in February and the speed and abruptness of the decline in April has seemingly caught a few managers off guard. We’d expect the best managers to eventually rise back to the top, and we’ve seen that in a number of cases, but that can also take time.

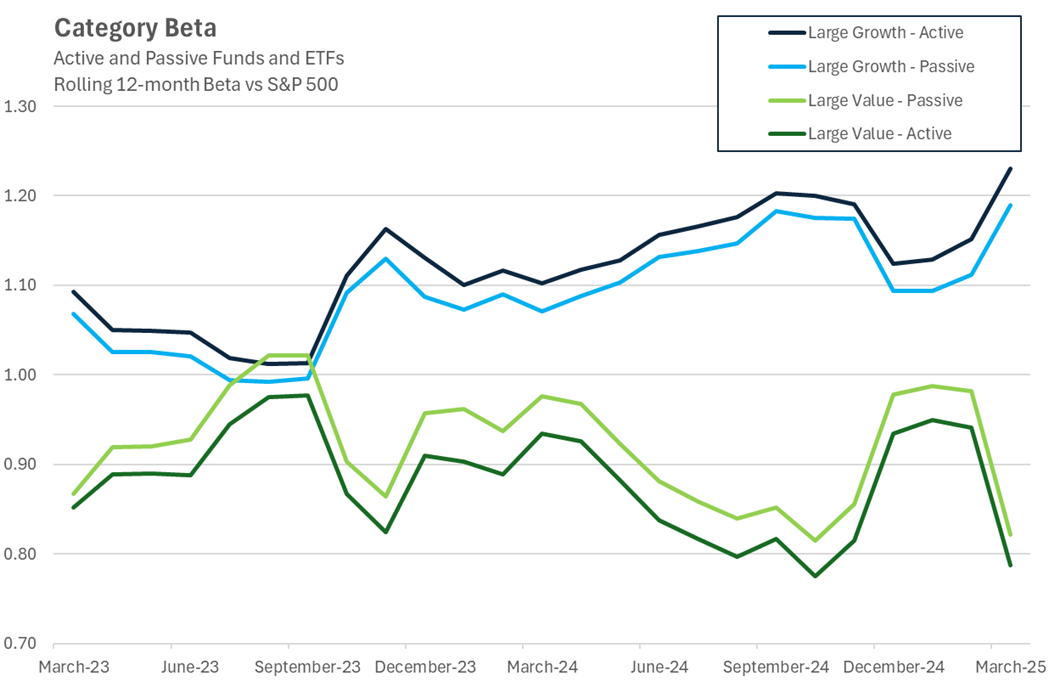

Another way to look at this in an aggregate way is to measure risk via beta. Beta is helpful because it’s two components – relative volatility and correlation – mean an increase in both will lead to a jump in beta. The chart below shows the rolling beta relative to the S&P for large cap value and growth managers, split between active and passive (mutual funds and ETFs). There are two different stories in these categories. Large growth managers have broadly been running a higher beta relative to their passive peers, and that increased in the months leading up to April. Not only that, but the beta of growth managers in general was more than 20% higher than the S&P 500 – not a great recipe to head into a sudden downturn.

Sources: Carson Investment Research, Morningstar 3/31/2025

On the flip side, active large cap value managers – generally a more pessimistic group – were running at risk levels below their passive peers, and well below that of the index. There are a number of contributing factors to this such as fund composition and cash weights that aren’t always completely manager discretion, but it still points to a much better expected return when the market heads south (all else equal).

While I would love to spend thousands of words discussing individual manager performance, the audience may trail off a bit. Below are some comments about specific asset classes and broad manager comments within to hopefully give some additional insight.

Broad manager comments:

- Large Value

Value managers that have stuck to their style, and particularly those with dividend requirements have done well this year. Naturally they avoid the high-flying tech areas that have seen volatility even before the Tariff tantrum began (think Deepseek), but they also tend to lean into more domestic-oriented businesses. For example, 70% of revenues in the Russell 1000 Value are from the U.S., versus just 53% in the Russell 1000 Growth (source: FactSet GeoRev).

- Developed International

It may be surprising to many, but overseas, value stocks have been significantly outperforming growth for over 7 years! Broad international stocks have performed well this year, both due to rebounding local share prices but also a falling dollar. Within this, value has done particularly well, up nearly 17% year-to-date on the back of traditional value sectors like Financials and Energy, which both hold higher weights abroad. Active foreign large value managers have been able to add even more value, up nearly 18% in aggregate as they navigate the global changes we’ve seen or anticipate so far in 2025.

- Core/Core Plus Bond

Core managers that have leaned into high quality areas of fixed income have generally been rewarded. We have seen a couple managers with ‘curve steepener’ trades (long the short end of the yield curve, short the long end), and those have worked out well this year, albeit potentially not for the reasons they were put on in the first place!

The opportunity for active managers and asset allocators grows substantially with volatility and dispersion. However, volatility is typically accompanied by uncertainty. Those who are able to stick with their process, be nimble yet controlled, and pay careful attention to risk have great opportunities to add value. We will continue to do our best at making those decisions as well as including active managers that do the same.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

For more content by Grant Engelbart, VP, Investment Strategist click here.

7921269.1-0525-A