Three weeks can feel like eons when you don’t get any official macroeconomic data (thanks to the shutdown), and so this morning’s release of the September Consumer Price Index (CPI) was more than welcome. The shutdown continues but this was a “special” release because the government needs this data to make cost of living adjustments for seniors’ social security payments next year.

Inflation remains elevated. Headline CPI rose 0.3% in September, which translates to a 3.8% annualized pace. Over the last three months, inflation has risen at a 3.6% annualized pace, and over the last year, it’s up 3.0%.

The headline data was boosted by higher gasoline prices in September (+4.1%). Energy prices are typically volatile, as are food prices, and so the Fed focuses on “core CPI,” which excludes both. There was a tad bit of good news there, because core CPI rose “only” 0.2%, which translates to a 2.8% annual pace. Over the last three months, core CPI is also up 3.6% annualized, and it’s up 3% over the past year. That’s far away from the Fed’s 2% inflation target.

The big picture is that inflation remains stubbornly elevated. Core CPI has been running above 2.8% year over year for four-and-a-half years now (54 months).

The details aren’t too comforting.

Tariffs Hitting Goods, but Services Hot Too

Think of the CPI basket as having five broad buckets: energy, food, other goods, shelter/housing, and other services (excluding shelter).

Energy prices are volatile and while gas prices rose in September, those have generally been on the softer side recently—gasoline prices are down 0.5% over the past year. This has helped offset the upside shock to electricity and utility prices (thank you, AI datacenters), which are up 6.4% over the past year (though they’ve eased in recent months).

Food prices are another visible source of inflationary pressure for consumers. Over the past year, grocery prices are up 2.7%, while restaurant prices (including fast food) are up 3.7%.

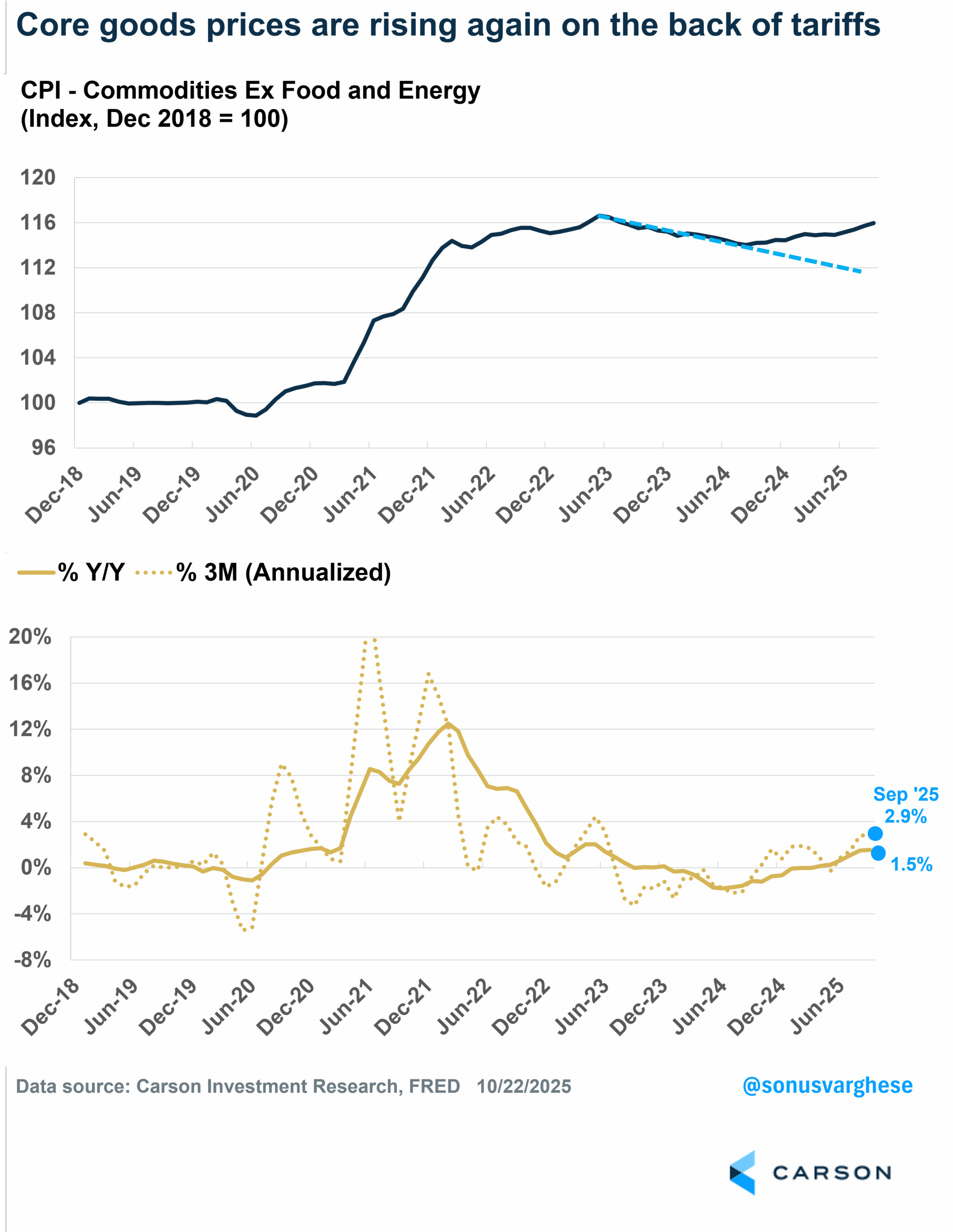

The big question on a lot of people’s minds is the impact of tariffs on inflation. The short answer is that they are having an impact, but it’s early days yet with companies eating more of the tariffs rather than passing it to consumers. (This may be because they’re still working off lower cost inventory for now.) The place where you would expect to see the tariff impact is in core goods prices (like furniture, appliance, and apparel), and the tariff impact is showing up there. CPI for core goods (commodities excluding food and energy) is running at a 2.9% annualized pace over the past three months, and 1.5% over the past year. That doesn’t seem like a lot, but keep in mind that prices for core goods were actually falling prior to March, reverting to their pre-pandemic trend after the big spike in 2021–2022.

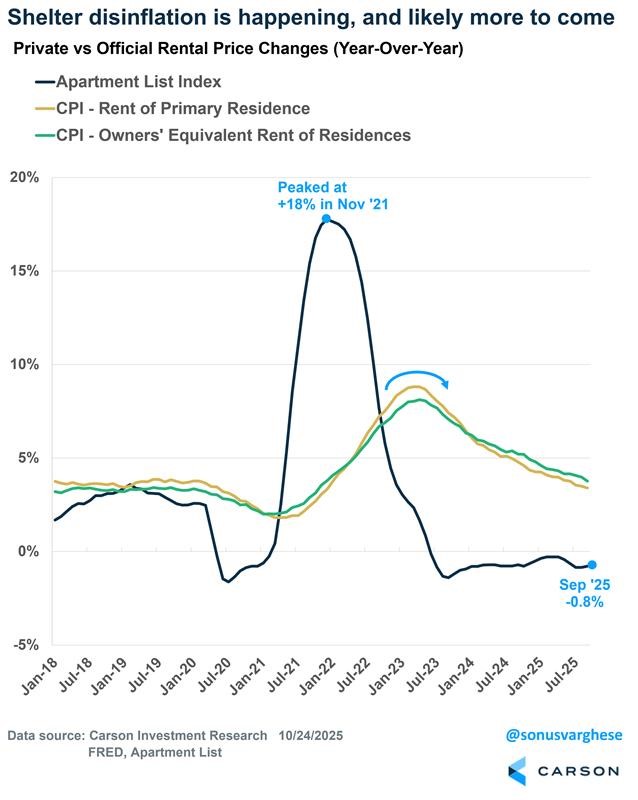

You could argue that core goods inflation is “transitory,” and the Fed is indeed making that argument. But there’s problems outside this as well. The good news is that the single biggest category within CPI, shelter, is still experiencing disinflation as rents ease. And based on private market rents, it looks like there’s more disinflation in the pipeline. Shelter matters a lot because it makes up about 33% of headline CPI and 44% of core CPI. (It matters less for the Fed’s preferred inflation metric, the Core Personal Consumption Expenditures Index, where the weight is just about 17%).

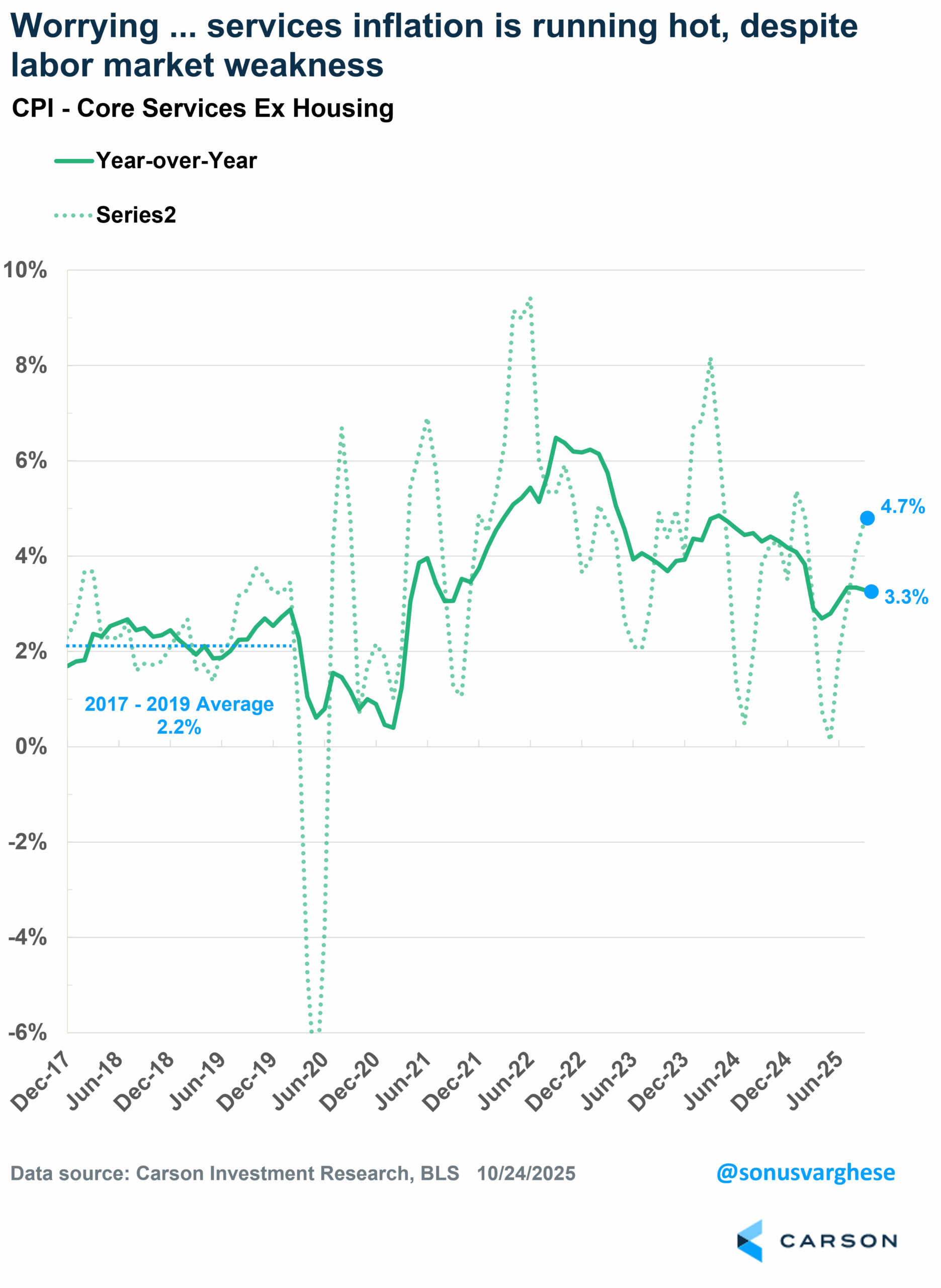

That begs the question: if shelter, which is a large category, is easing, what’s keeping inflation elevated? The answer is core services (services excluding shelter). Core services inflation is running hot, to say the least:

- September: +4.3% annualized pace

- Last 3 months: +4.7% annualized pace

- Last 12 months: +3.3%

For perspective, the pre-pandemic trend (2017–2019) for core services inflation was 2.2%. We’re well above that. Even if you argue that core goods inflation is transitory, the fact that core services inflation is as elevated as it is very problematic for the Fed. But for now, the Fed is going to look past it.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

How Much Does This Inflation Report Matter?

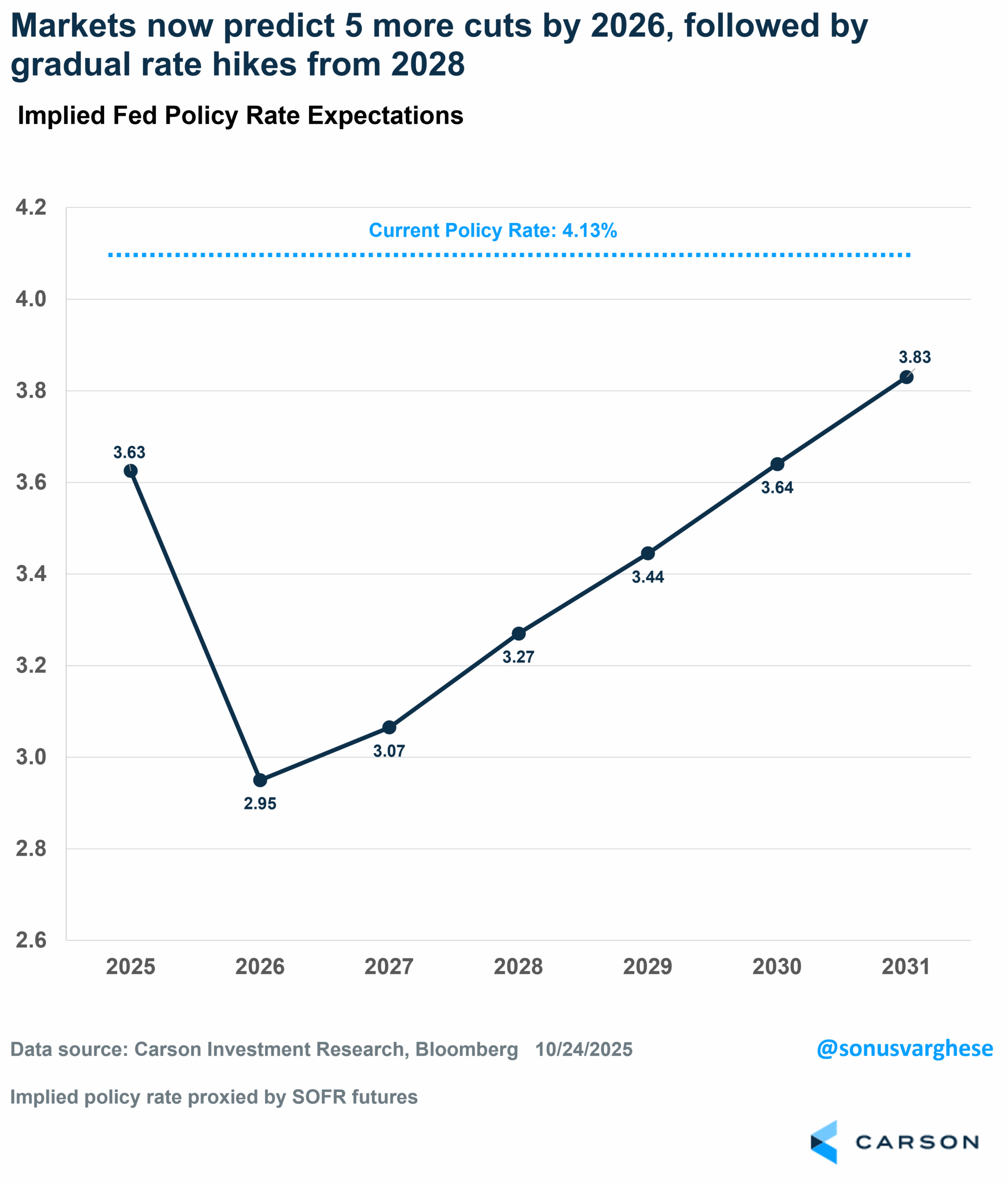

While it was a relief to get some official data, or any data, this CPI report was never going to matter too much. The Federal Reserve already told us that they’re more worried about weak payroll growth and will tip quite heavily toward protecting the labor market over fighting inflation, which is why markets are pricing in a slew of rate cuts over the next year:

- Two more 25 bps (0.25%-point) cuts are expected this year.

- Three more 25 bps cuts are expected next year.

If all this materializes, and right now Fed officials are not exactly pushing back on these expectations, the Fed’s policy rate will move from its current level of around 4.13% to 2.95%. This is even lower than where expectations were after Liberation Day, when economic growth expectations were much weaker amid the tariff chaos. This is significant.

A 3% policy rate is what the Fed considers “neutral”—a policy rate that’s not too accommodative nor too tight. But now we’re expected to get below that even as inflation remains well above the Fed’s target. In other words, Fed policy is expected to run quite dovish over the next year, and even beyond. Investors expect the Fed to raise rates from 2028 onwards, but only gradually. This is a tailwind for the cyclical economy, like housing and manufacturing, and even risk assets like equities. A dovish Fed that essentially keeps “real rates” low (nominal rates minus inflation) is a tailwind even for assets like gold. (I recently wrote about gold being buttressed by a dovish Fed and lower real rates.)

On the other hand, if all these rate cuts don’t materialize, that would imply the labor market is not deteriorating and the Fed can pull back from rate cuts. But a stronger labor market means the economy is in better shape than most realize. That’s a tailwind for companies and profit growth.

The risk is that the economy is already weak, and the Fed is too late in cutting. But it doesn’t look to be the case. In the face of official economic data deprivation, the macro picture coming out of company earnings calls takes on more importance. And the news is good. As I told the Wall Street Journal, the big takeaway is that everything looks fine. So far, 86% of the 130 S&P 500 companies that have reported earnings have topped analysts’ estimates. That’s well above the historical average.

So going into the tail end of this year and into 2026, the set up looks good for stocks, including strong momentum over the last six months, positive seasonality, a dovish Fed, less uncertainty around tariffs, and tax cuts at the start of 2026. Our proprietary leading economic index for the US also points to an economy that continues to grow along trend, with a relatively low probability of recession in the near term.

For more content by Sonu Varghese, VP, Global Macro Strategist click here

8537935.1.-24OCT2025A