Nvidia released its latest earnings report after market close on Wednesday, delivering results that beat expectations. The company has had anything but a smooth start to the year, most recently having to manage through a ban on selling product to Chinese customers. Yet, these latest results show the company keeps executing as guidance implies a strong quarter to come amidst the AI Boom. Investors have many reasons to cheer.

Nvidia reported revenue of $44.1 billion, an increase of 69% from the same period last year, and beat FactSet consensus estimates of $43.3 billion. These results were dampened by a few billion dollars of lost revenue from product destined for China that the company was unable to ship due to regulatory changes. Including these missed revenues, the company would have even shown an even stronger growth rate. The company guided for $45.0 billion of revenue in the coming quarter which includes an additional $8 billion headwind from China-bound product the company has scrapped. Investors may be well served to adjust Nvidia’s anticipated revenue higher by this lost amount and see that the company’s guidance implies revenue growth would accelerate from this quarter’s result. Accelerating revenue growth for a company of this size is an impressive feat.

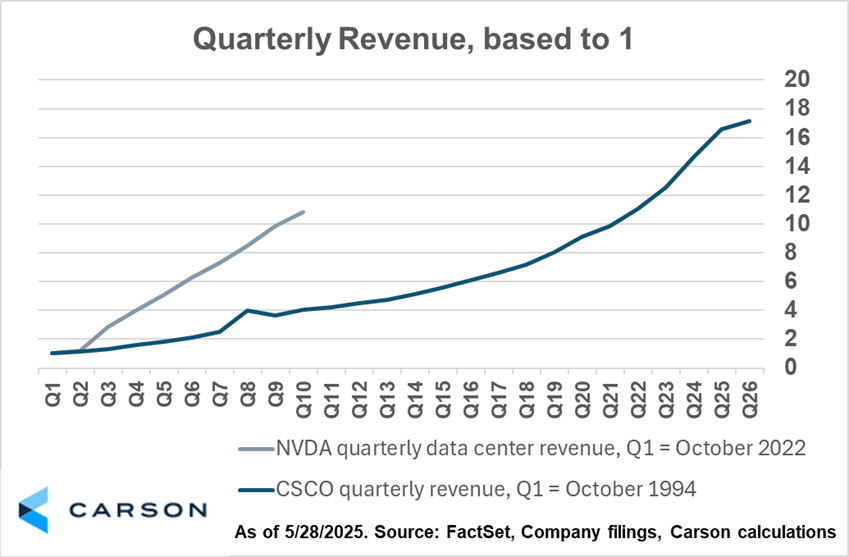

Nvidia’s financial trajectory continues to outpace that of Cisco’s growth during the DotCom era. While technology skeptics have questioned the sustainability of the AI Boom – likening it to a speculative bubble akin to the late 1990s period – Nvidia’s financial results remain substantially better than what Cisco, a posterchild of the DotCom era, produced during the time. As shown below, Nvidia’s quarterly data center revenue has grown nearly tenfold since the AI Boom began ten quarters ago in the fall of 2022. By contrast, ten quarters into the DotCom boom, Cisco’s quarterly revenue had ‘only’ grown by 3.1x. Nvidia’s impressive financial results underscore how critical the company’s chips are to AI development in this new technological revolution.

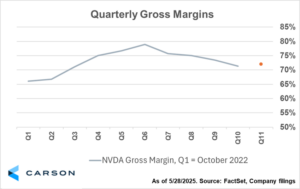

Investors may also be cheering the earnings report for Nvidia’s gross margin result and guidance. Gross margin, which may be an investors’ indication of pricing power and customer demand, declined for a third consecutive quarter, from last quarter’s 73.5% result to 61.0% this quarter. However, this result includes a $4.5 billion one-time charge from the earlier mentioned China sale restriction. It may be appropriate to adjust this result to exclude these charges, which produces in a 71.3% gross margin as shown in the chart below. Nvidia guided for next quarter’s gross margin to be 72.0% (shown as the orange dot in the chart below) which represents the first gross margin increase in four quarters if achieved. Most encouragingly, CFO Colette Kress noted “the company is continuing to work towards achieving gross margins in the mid-70% range late this year” and implies the company is gaining pricing power. Talk of increasing gross margins is welcome news for investors.

Forward looking commentary from Nvidia and industry participants remains strong and may bode well for future results. While Nvidia only provides financial guidance on a quarterly basis, CEO Jensen Huang on the company’s earnings call noted “We’re just in the beginning of the buildout [of these AI factories], and there should be many more announcements in the future.” Further, DeepSeek-induced worries may be turning to opportunity for Nvidia as Stacy Rasgon, Senior Analyst at Bernstein, noted on a CNBC interview that “The only thing we’ve seen since DeepSeek debuted is compute demand go through the roof.” Additionally, some of the largest CEOs in the cloud computing industry acknowledged during their earnings call that demand for compute remains robust, as I covered in my Tech Earnings Takeaways. With many key industry players investing behind robust demand, the future may continue to be powered by Nvidia.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Taken as a whole, Nvidia’s results and guidance beat expectations. Excluding certain one-time revenue headwinds and charges driven by a regulatory change, the company’s financial performance continues to surprise. Their guidance implies revenue growth excluding China may be accelerating, and that gross margins may expand in the coming quarters, both of which are key clues investors may interpret as strong demand and robust pricing power. Forward-looking commentary from large customers and industry observers alike suggests that AI application development and scaling continues at a rapid pace, and were even accelerated by reasoning breakthroughs such as DeepSeek. Nvidia’s ability to beat expectations amidst a turbulent 2025 is a testament to the central role they play in the AI Boom.

Separately, I was honored to join Ryan Detrick, Chief Market Strategist, Sonu Varghese, Vice President Global Macro Strategist, and Dan Ives, Global Head of Technology Research at Wedbush Securities, on stage during their live Facts vs Feelings podcast at Carson’s Partner Summit! Fast forward to the 28:30 mark to hear my question. Dan is incredibly knowledgeable about the technology supply chain, infrastructure, and applications. His research about many major technology companies often helps investors, myself included, to see years into the future and understand the trends driving demand. I asked Dan about Microsoft – why the company’s stock has largely gone nowhere in the previous year despite them “seeming to have it all,” and what might help reignite shares higher. His response was insightful, particularly his point that “Microsoft is only 8% through their installed base in terms of [AI monetization],” in their estimates. That may mean there’s more revenue growth to come and give investors a reason to cheer. Thanks again for the time, Dan!

8022359.2-6.2.25A

For more content by Blake Anderson, CFA®, Associate Portfolio Manager click here