Carson Investment Research released our 2025 Outlook: Animal Spirits on Tuesday. As we highlighted there, we think that economic strengths clearly outweigh areas of weakness in the year ahead, and the opportunities likely have a higher probability of coming to fruition than the threats. We believe that economic momentum, an easing Federal Reserve (Fed), and pro-growth fiscal policy will continue in 2025, but we may also get a lift in the national mood that economists call animal spirits.

We see an opportunity for a virtuous cycle of economic activity that can help sustain strong economic growth, but the opportunity is also easily squandered, making a potential policy mistake a key risk for the expansion not achieving its full potential. That could result in more volatile markets in 2025 than what we saw in 2024.

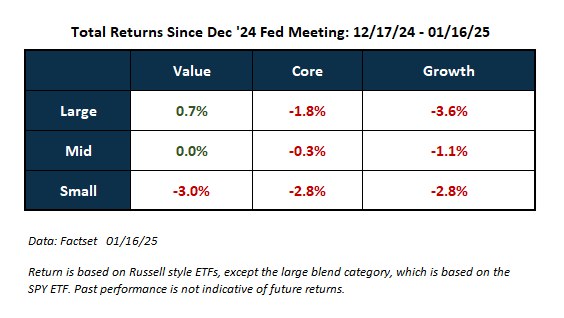

We got bit of a taste of this over the past month, since the Fed’s December meeting. Without belaboring the gory details of that meeting (which I wrote about a month ago), the upshot was that the Fed is really worried about inflation uncertainty, with risks now seen as weighted to the upside. Even though they didn’t admit it directly, it’s clearly driven by expectations of tariff policy by the incoming Trump administration. The hawkish tone put a dampener on stocks over the past month, with weakness across the style and cap spectrum, in what should typically be a strong seasonal period for markets. This was driven by a pickup in Treasury yields, as markets priced in just one rate cut across 2025.

Adding to the volatility was a strong December payroll report, which was seen as another factor that lowered rate cut expectations further. I wrote about this “good news is bad news” dynamic last week. Suffice to say, good news ultimately is good news and, as we wrote in our 2025 Outlook, we expect economic good news (however it’s interpreted by markets in the short-term) to outpace bad news in 2025.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

One thing driving the “good news is bad news” dynamic is the notion that a strong labor market will push demand for goods and services higher, driving inflation higher, forcing the Fed to keep rates elevated. We’ve also been hearing the refrain “How can the Fed cut when GDP growth is running at 3% and the unemployment rate is near 4%?”

What I think is being missed is productivity growth: with productivity growth, you can have strong wage growth with low inflation. And a strong labor market is also key to strong productivity growth. We have written about this positive feedback loop in our 2025 Outlook (as well as our 2024 outlook). We think this dynamic should let the Fed take its foot off the brake more than markets currently expect. The good news is this may already be playing out, as we got some positive inflation data from the December data.

The Inflation Picture Looks Good

The December consumer price index (CPI) data came in below expectations, with headline CPI rising 0.4% and core CPI (excluding food and energy) rising just 0.2%. This was a big relief for markets, with the S&P 500 rising 1.8% on the release day (January 15, 2025). But let’s dig into the details a bit, as there’s even more good news there.

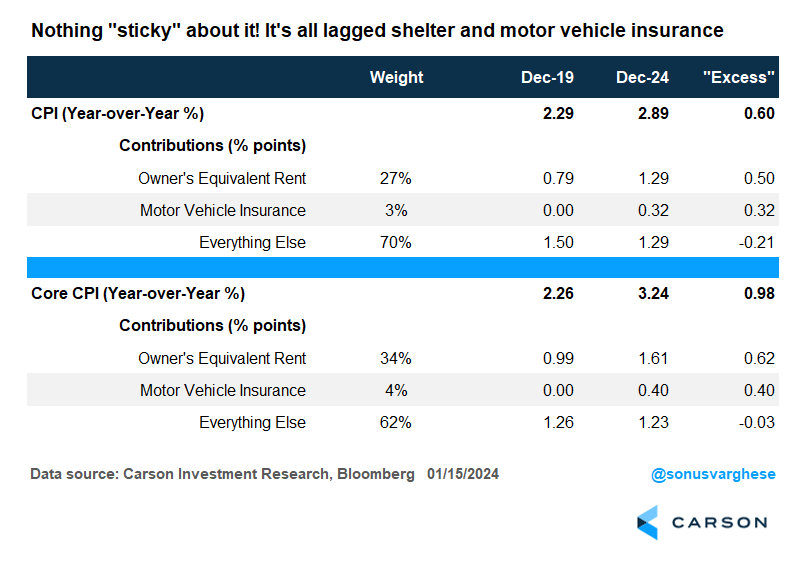

Headline CPI is up 2.9% across 2024 (year over year), and core CPI is up 3.2%. These numbers are clearly over the Fed’s 2% target. Cue the cries that “inflation is sticky” and that the Fed is erring by cutting rates. This couldn’t be further from the truth.

Note that the Fed targets the personal consumption expenditure (PCE) inflation metric, and I recently wrote a blog on why this metric (both headline and core PCE) shows no signs of concern if you look under the hood. Still, let’s focus on where “excess inflation” is coming from for CPI and compare the 2024 data to 2019 (when headline and core CPI were up 2.3% year over year). There are two main drivers of excess inflation: shelter and motor vehicle insurance.

Within shelter, it’s really “owner’s equivalent rent” (OER), which is the “implied rent” homeowners pay, and is based on market rents as opposed to home prices. OER makes up 27% of the headline CPI basket, and a whopping 34% of core CPI. It’s now up 4.9% year over year (y/y), versus 3.3% in December 2019. That’s adding 0.50-%-points to “excess” headline CPI relative to December 2019, and 0.62%-points to “excess” core CPI.

The other component is motor vehicle insurance, which makes up 3% of the CPI basket (and about 4% of core CPI). Motor vehicle insurance is adding 0.32%-points to excess headline CPI and 0.40%-points to excess core CPI (relative to December 2019).

Together, OER and auto insurance fully account for the entirety of excess CPI inflation, both for headline and core. Everything else put together is making a negative contribution.

Another important point here: the December 2019 levels of CPI actually coincided with PCE and core PCE (the Fed’s preferred metrics) running below their target of 2% — at 1.5% and 1.6% y/y, respectively.

All this is year-over-year data, which is impacted by what happened last year to a degree. But things are looking up when you look at more near-term data.

For one thing, motor vehicle insurance inflation is pulling back in a hurry. Car insurance costs surged in 2023 due to lagged effects of higher car prices post-pandemic (and more car crashes), rising 26% y/y at its peak in August 2023. But the pace has eased to about 11% y/y, and just under 2% annualized over the last three months (through December).

There’s also better news on the docket that is key for the inflation outlook.

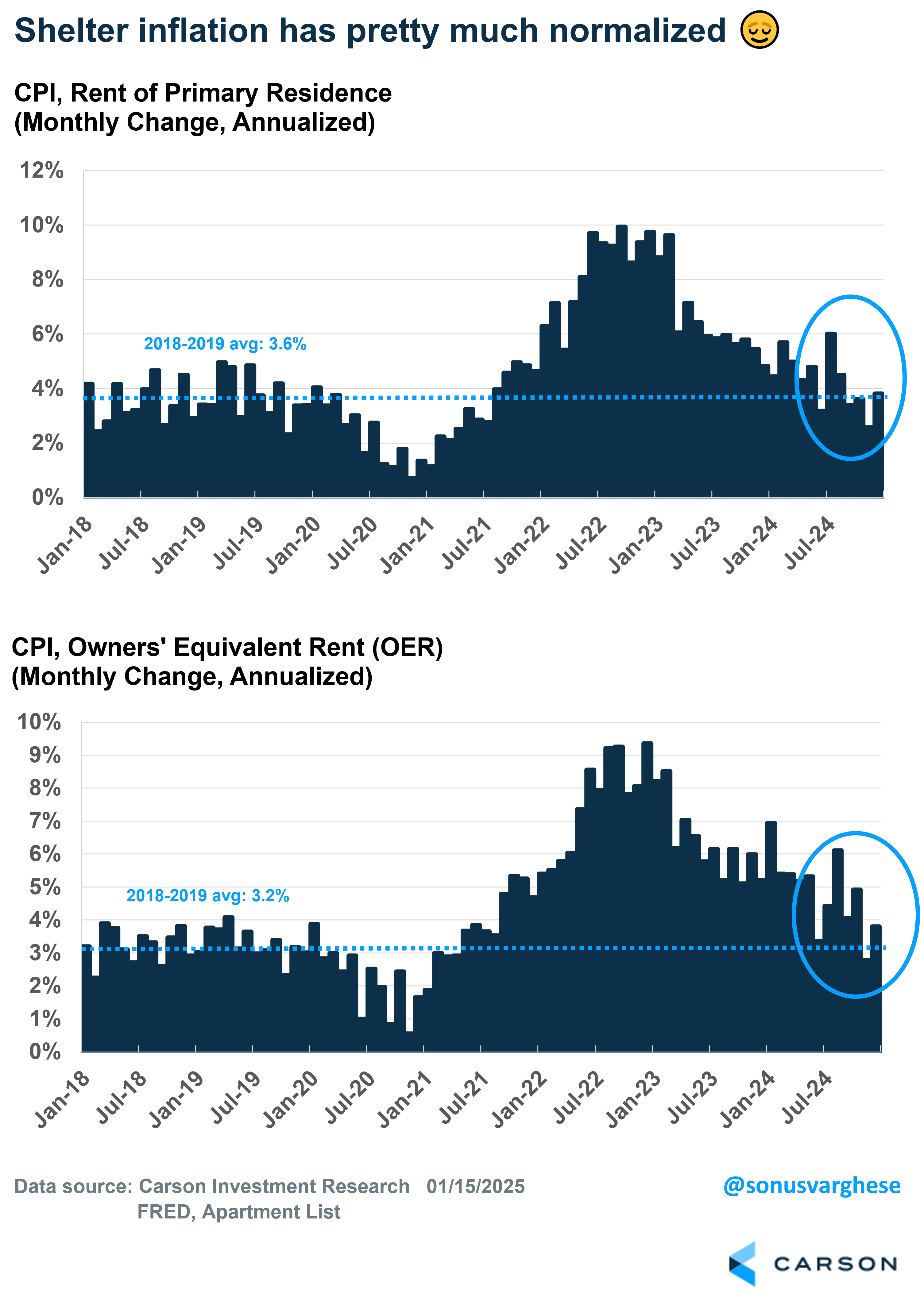

Shelter Inflation Has Normalized

Shelter inflation is made up of two components, rents of primary residences and OER. On a year-over-year basis these are still elevated:

- Rents are up 4.3% y/y versus the 2018-2019 average of 3.6%.

- OER is up 4.8% y/y versus the 2018-2019 average of 3.2%.

However, more recent numbers look even better. On a 3-month annualized basis, rents are up 3.2% and OER is up 3.8%.

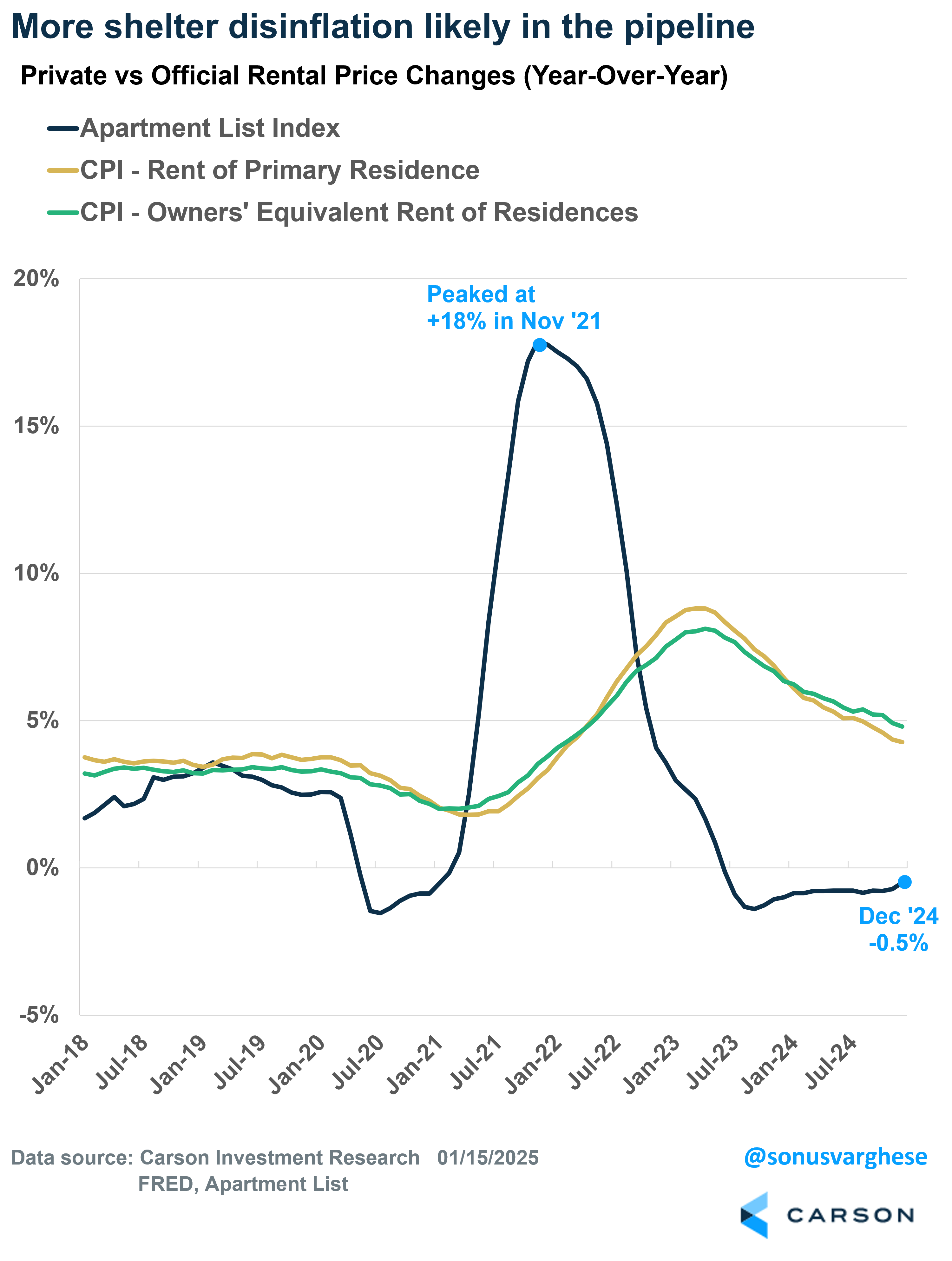

Shelter inflation is inching ever closer to the pre-pandemic average. And there’s likely more disinflation in the pipeline, as we discussed in our 2025 Outlook. Apartment List reports that median rents are down 0.5% y/y, the 19th straight month with a negative y/y reading.

It’s early days yet but the overall picture we painted in the Outlook still holds. The economy has a lot of strengths going for it, including strong income growth and solid household balance sheets. But there are potential tailwinds from the policy front as well, with the path of monetary policy being key. We do see the Fed as likely to cut 2-3 more times in 2025, as the inflation data moves in a more favorable direction.

In fact, after the December CPI report was released, Fed Governor Chris Waller, who is one of the more influential members on the committee, said that rate cuts are possible in the next few months. He noted that the inflation data so far indicate that their preferred metric, core PCE, will come in at or close to the Fed’s target for the sixth time in the last eight months. And if this continues, it’s “reasonable to think that possibly rate cuts could happen in the first half of the year.” Music to the market’s ears. Now we just need the data to come in favorably, which we believe is likely.

Chief Market Strategist, Ryan Detrick and I discussed a lot of the opportunities, and risks associated with policy (monetary and fiscal) when we talked about our 2025 Outlook on our latest Facts vs Feelings podcast episode. Take a listen.

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

7543809.1-0125-A