As we get ready to release our 2025 Outlook, I thought now would be a good time to revisit our 2024 Outlook. I recognize this is rare in our world, as it’s not often you see strategists revisit and reevaluate their calls. We don’t really think of ourselves as forecasters in the strict sense of the term, in that we’re not trying to predict economic variables, or even market moves. But we manage several multi-asset class portfolios and we’re always making choices within those portfolios, i.e. “predictions” as to the opportunity cost of overweighting or underweighting one asset class versus another. That’s another difference between a lot of the outlooks you see and the ones we put out — usually, the people writing these are not managing portfolios.

If you’ve followed us over the last two years, you know that we’ve had some strong views during that time, much of it in sharp contrast to the consensus. But our views are always translated to our portfolios, and it’s within that context that we evaluate what we got right and wrong. That’s how we try to keep ourselves honest during the process. (Of course, it’s reflected in portfolio performance too.)

One knock some critics have on us is that we’re “permabulls,” which Ryan pushed back on over a month ago. Of course, if you had to be a perma-anything, a permabull would be the way to go (though it may sell fewer newsletter subscriptions). As Ed Yardeni recently wrote (on the same topic of permabulls vs permabears), bear markets are infrequent and don’t last very long — that’s because they tend to be caused by recessions. Yardeni points out that since the end of World War II, eight of the 10 bear markets have coincided with recessions. That’s one reason why we spill a lot of ink (or keystrokes!) on discussing the economy, an area where our “prediction” for no recession in 2023 and 2024 was seen as quite bonkers at the time. It turned out to be the right call, but more importantly, we like to think we got it right for the right reasons. With that, here’s the verdict on 12 calls we made in our 2024 Outlook.

One: Upside from productivity growth means expansion will continue in 2024

Verdict: Correct

Real GDP growth will likely clock in between 2.5 – 3.0% in 2024, boosted by productivity growth that is running quite a bit higher than what we saw from 2005 – 2019.

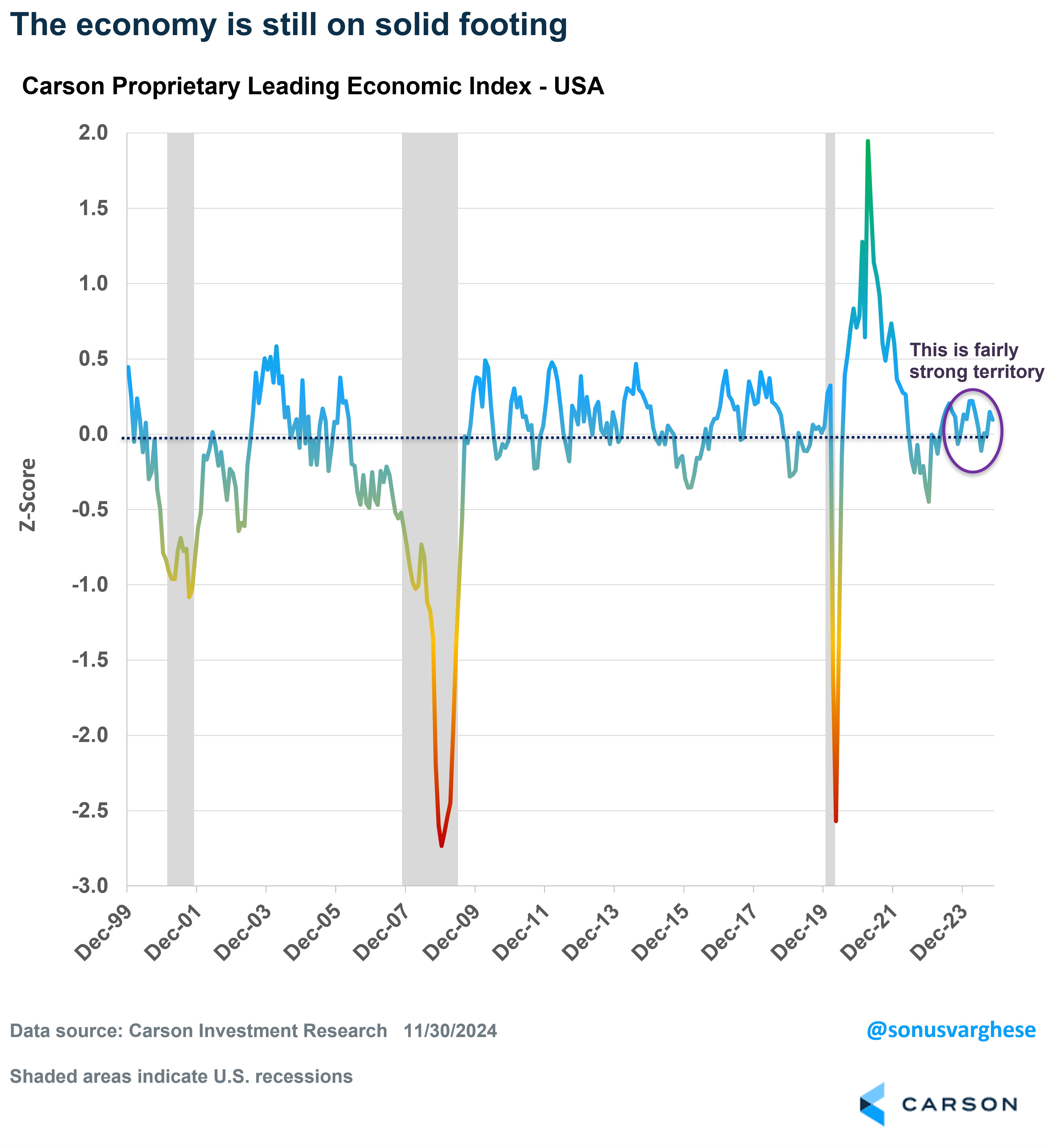

Two: Our Proprietary LEI suggests expansion continues. Consumption strong amid real income growth.

Verdict: Correct

Our proprietary leading economic index (LEI) for the US never indicated a recession in 2023 or 2024. (We populate a similar measure for 30 countries, and wrap it up into 5 regions, and the world.) This was mostly on the back of consumption driven by strong income growth, and strong household balance sheets. Real income growth was also boosted by falling inflation and lower energy prices. Employee compensation rose 5.8% over the past year, while headline PCE inflation (personal consumption expenditures) was up 2.4%.

By the way, our US LEI remains in a fairly solid place as we move into 2025.

Three: Cyclical headwinds from fixed investment fading, especially amid easing rates.

Verdict: Mixed

We expected headwinds from the investment side of the economy to fade as interest rates eased in anticipation of Fed cuts, especially housing. We thought business sentiment would improve as rates pulled back and also expected continued growth in manufacturing construction and equipment spending on the back of fiscal programs like CHIPS and IRA. Housing was positive in Q1 but started to fade as mortgage rates stayed elevated. We didn’t get much of a boost in business sentiment (except post-election), but we did see manufacturing adding to GDP growth after the first quarter.

Four: Inflation continues to pullback

Verdict: Mostly Correct

Inflation measured by the Fed’s preferred metric, core PCE, was running at 3.2% year over year 12 months ago, and it’s at 2.8% now (core CPI pulled back from 4% to 3.3%). Strictly speaking, we were “right,” but in all honesty, we expected shelter disinflation to drive inflation even lower than its current pace (along with goods deflation, including vehicle prices). I’m taking away some points for that.

Five: Expect the Federal Reserve to cut interest rates 3-4 times in 2024

Verdict: Correct

We kind of nailed this. Technically, the Fed cut 3 times, but by a total of 1%-point. Note that markets were pricing in 6-7 rate cuts a year ago, and so calling for 3-4 cuts was not exactly “consensus”. We did expect inflation to pull back, allowing the Fed to cut, but we also expected economic growth to stay strong (thus avoiding recessionary cuts).

Six: Forward earnings continues to grow, along with profit margins

Verdict: Correct

Next 12-month earnings for the S&P 500 were at $242/share a year ago, and it’s currently around $272. Forward margins are also at record highs of around 13.5%.

Seven: Bull market should continue in 2024

Verdict: Correct

This was supported by all of what came above — a strong economy, rate cuts, and earnings growth — but also the fact that historically, election years do better. All of this ended up being right, and we positioned our portfolios close to maximum equity overweight across the year. Now we did expect low double-digit returns for the S&P 500 in 2024, but strong momentum over the first six months led us to up that to around 20% in our Mid-Year Outlook. We adapt! Yes, 2024 total returns are likely to be quite a bit higher than that, but I’m still giving us full points for this. As I pointed out at the top, at the end of the day, it’s the portfolio decision that counts, not just the “call.”

Eight: Mid and small caps favored on the back of more favorable valuations and easing rates

Verdict: Wrong

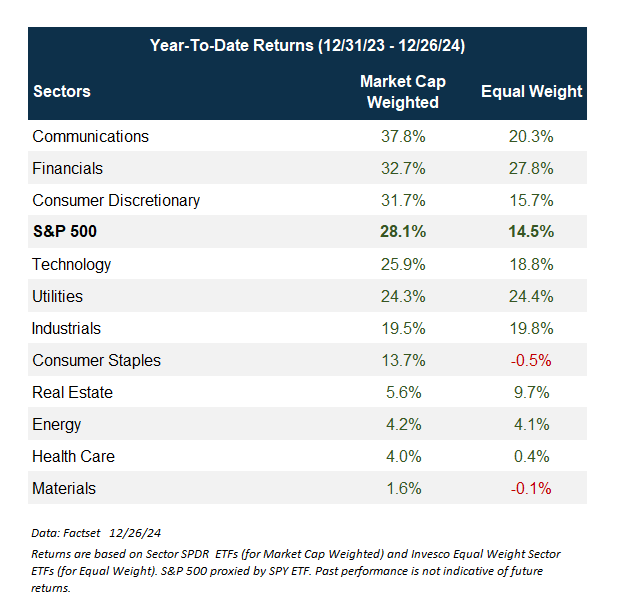

This one hurts. An above-trend economy, easing rates, growing earnings, and more attractive valuations is what led us to make this call and overweight mid and small caps in our portfolios, although it was only a moderately sized bet. One thing people say when small caps underperform is that the Russell 2000 index has a lot of negative earners. However, we use the S&P indices, which screen for positive earnings, so that’s not an excuse. In fact, year to date (through 12/26/24), the Russell 2000 index is up almost 14% on a total return basis, versus 10.7% for the S&P 600.

Another argument here is that it’s all about the Magnificent Seven stocks. But this would be bit of lazy analysis on my part. What’s interesting is that in 8 of 11 sectors, the market cap-weighted sector index outperformed the equal-weighted sector portfolio — industrials and utilities were the exception (the returns were close), along with real estate. So, this wasn’t just about Technology, or Tech-adjacent stocks. In almost every sector, returns favored the largest companies. This is something we’re thinking deeply about and will discuss in the future.

Nine: Financials and energy sectors favored

Verdict: Mixed

Financials ended up being the second-best performer amongst the sectors, but our energy call was off. Though full disclosure: we removed our energy overweight early in the year, and overweighted communication services and industrials (along with financials). We do reserve the right to change our minds.

Ten: Intermediate maturity bonds outperform short maturity as Fed cuts

Verdict: Wrong

We got this wrong, plain and simple. At the same time, we were heavily underweight fixed income, and Treasuries, in our portfolios. So, we weren’t too unhappy to maintain duration close to that of the Bloomberg Aggregate Bond Index, even though it would have literally paid better to be in cash (short maturity Treasuries). Having longer duration did help during the bout of volatility we had in August, when treasuries rallied. Also, we diversified our diversifiers, with exposure to gold and managed futures throughout the year. That more than overcame any drag from holding onto longer duration bonds (relative to Cash). But I’m still going to rate this “call” as something we got wrong.

Eleven: Credit likely to outperform Treasuries, but we prefer equity risk

Verdict: Correct

We got this right, and it was based on a strong economy with no recession in sight. Here are year-to-date returns for bond indices as of 12/26/24:

- Bloomberg US Aggregate Bond Index: 1.1%

- Bloomberg US Treasury Index: 0.4%

- Bloomberg US Corporate Index: 2.2%

- Bloomberg US Corporate High Yield Index: 8.1%

However, as I noted at the top, what matters is not the just call itself but portfolio construction. And from that perspective, credit’s strength versus Treasuries is irrelevant. We had better exposure to the driver of that credit component through equities. And that’s why I rate this is as correct.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Twelve: US over international equities, due to a stronger dollar amid stronger relative economic growth

Verdict: Correct

You may be saying “Duh! Of course, you should underweight International given the last decade of outperformance by US stocks.” But again, we’d rather be right for the right reasons. The US economy did outshine everyone else in 2024, as we expected (and gave us enough reason to overweight US stocks). But we also saw dollar strength (even prior to the election), which ended up being an additional headwind for international equities. The MSCI All-Cap World ex US index rose 13.1% in local currency terms (through 12/26/24) but was up just 5.5% in USD terms.

Here’s the final count:

- 7 Correct and 1 Mostly Correct

- 2 Mixed

- 2 Wrong

Once again, I want to stress that it’s not about the calls, but how they translate to the portfolios we manage. And from that perspective, the verdict is actually better than what I summarized above. We obviously did get some calls wrong, but that’s also where portfolio construction matters, along with risk management. An important point here is that we do have broadly diversified, risk-based benchmarks for all our portfolios. As my colleague Barry Gilbert wrote, selecting a benchmark is not a trivial affair. It serves as our effective starting point for portfolio construction, but it’s also the neutral point we’re comfortable sitting at when uncertainty is high and we don’t see opportunities to add differentiated value.

Keep an eye out for our 2025 Outlook, which will be released soon. In the meantime, take a listen to our latest Facts vs Feelings episode where Ryan and I talked about the Fed and Santa Claus!