Well, this came out of the blue, but a U.S. court essentially cancelled the tariffs that set off a global trade war (technically paused until July).

The US Court of International Trade (USCIT) struck down all of the “IEEPA” tariffs imposed by President Trump. IEEPA is the International Emergency Economic Powers Act that was passed in 1977, and allows the President to “regulate international commerce” after declaring a national emergency. It was under IEEPA authority that the President imposed the following tariffs

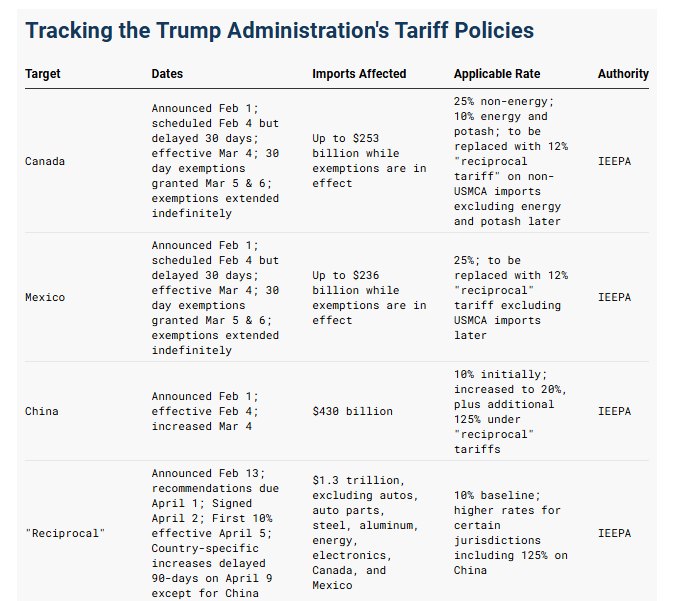

- China, Mexico, Canada tariffs in response to Fentanyl trafficking

- Liberation Day (April 2nd) “reciprocal” tariffs imposed in response to “they’re ripping us off because of trade surpluses”

Here’s a handy table from the Tax Foundation

The court’s 3-judge panel unanimously ruled that the President exceeded IEEPA authority, and that the Act does not grant “unbounded tariff authority”. Specifically, they said the emergencies used to justify the tariffs were not valid. The immigration/fentanyl tariffs imposed on Canada, China, and Mexico do not “deal with” the emergency cited by the administration. And chronic trade deficits used to justify the Liberation Day tariffs do not meet the test of an “unusual and extraordinary” threat.

Of course, the administration has already appealed, and ultimately it’s going to come down to the Supreme Court. So, it’s anyone’s guess whether this ruling is reversed or not.

Tariffs Aren’t Going Away for Good

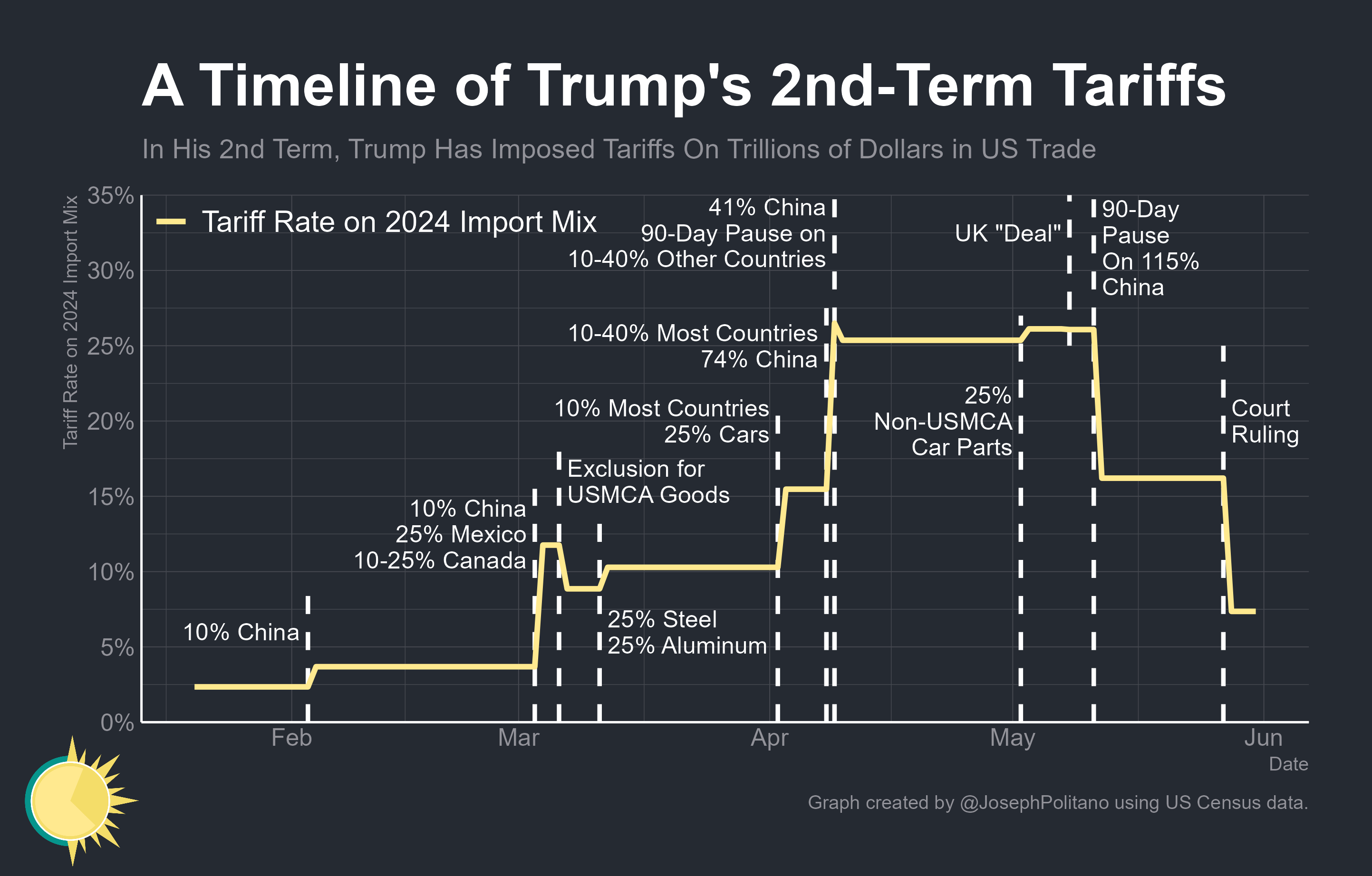

The court ruling against the IEEPA tariffs would lower US average tariff rates by about 10%-points, leaving behind tariffs on cars, steel and aluminum after everything we’ve seen over the past four months.

At the same time, the ruling doesn’t mean the President cannot impose tariffs anymore. He can, but he’ll have to use other authority.

In fact, the court directed the President to use non-emergency authority in “Section 122” to respond to an imbalance in trade that results in a trade deficit. However, this authority is much more limited. Under it, the President can impose tariffs of as much as 15 percent for up to 150 days against one or more countries that have “large and serious” balance-of-payment surpluses with the US. After 150 days, it’ll have to be authorized by Congress.

The President can always use other authority to impose tariffs – there’s an entire number soup of tariff-related sections for this

- Section 301 (Trade Act of 1974) – for retaliatory tariffs on unfair trade practices

- Section 232 (Trade Expansion Act of 1962) – for national security-based tariffs

- Section 201 Trade Act of 1974) – for safeguard measures

In fact, these are the authorities the President used during the 2018 trade war (with tariffs imposed on steel and aluminum, washing machines, solar panels, and a broad array of Chinese imports).

Even this time around, the Trump administration is using the national security-based Section 232 authority for implementing sectoral tariffs, including steel and aluminum, autos, pharmaceuticals, chips, electronics, lumber, etc. There’s less legal uncertainty related to the use of Section 232 tariffs, and we could see the President starting to refocus on these. Though these do require an investigation that could take up to nine months.

The President could also direct the US Trade Representative to launch “Section 301 investigations” on key trading partners. Now, this is a more drawn-out process and would probably take months to be fully completed. At the same time, the President has no limit on the level or duration of these tariffs.

There is also something called Section 338 authority. It’s from the Smoot-Hawley 1930 Tariff Act and allows the President to impose “proportionate” retaliatory tariffs on imports from a country that is imposing unreasonable tariffs and restrictions on US goods, or discriminating against the US. It’s not been used since WWII, since new trade laws (like Section 301) were authorized. But the Trump administration is likely looking at this authority at this very moment.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Court Ruling is a Big Deal But It May Just Prolong Uncertainty

At the end of the day, the big difference between IEEPA and these tools is that the latter impose significant procedural hurdles. Which is why the court ruling could be a fundamental blow to the Trump agenda. Not least because it also rules out the use of a tariff dial by the President during negotiations, allowing Trump to ratchet tariffs up and down by Oval Office (or Truth Social) pronouncement.

We’re also unlikely to see any trade deals before July. The court ruling will probably shift other countries approach to trade negotiations with the US. trade deals take a lot of time anyway, but expect most countries, if not all, to start dragging their feet. Even the UK, which is the only country that reached any sort of “trade deal” with the US recently is in a better position – they no longer face the 10% baseline tariff, and they have the option of slow walking finalization of their proposals to the US side (like opening up their market to US ethanol and hormone free beef produced in the US).

Ultimately, the tariff mess, and ongoing uncertainty, is only going to be prolonged. The final destination may still be significantly higher tariffs – with the average effective tariff rate ranging from 15-20% versus 2-3% last year – but getting there is going to take longer, with even more curves and u-turns.

We’re likely going to become really familiar with the entire number soup of tariff authority, assuming the court’s decision is not reversed by higher courts. Keep in mind that if the President ends up using authorities like Section 301 and 232, they’re going to be more enduring and able to withstand future legal challenges (assuming they go through the required procedures).

At the same time, the court ruling significantly reduces the tail risk of tariffs going from 10% to 50% over the course of a day (and reversed again). We’re probably done with that, unless the ruling is reversed.

More Revenue for Business, Less Revenue For The Government

The court gave the administration 10 days to halt tariff collection, but made no provision for refunds of tariffs collected to date. Businesses can file claims with US Customs but expect these to be trapped in bureaucratic red tape (especially because there are fewer workers across the federal government right now). Even though the administration is appealing to the US Court of Appeals (and after that the Supreme Court if things don’t go in their favor), a decision is unlikely in 10 days.

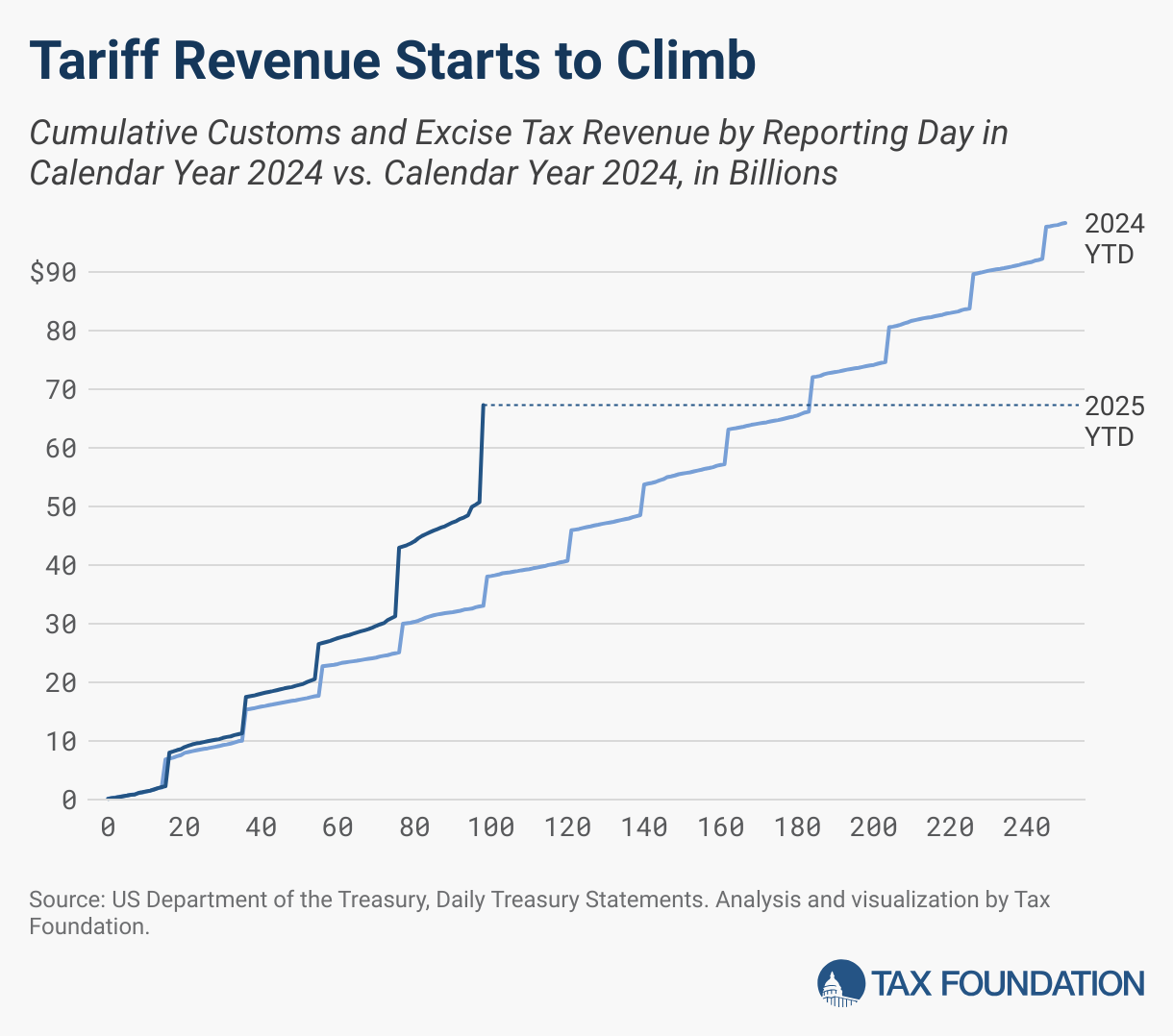

So in all likelihood, tariff collection will be halted. That’s going to have an impact. Not surprisingly, the federal government has seen a surge in tariff duties on imports this year. Over the first 98 days of the year, the federal government has collected $67 billion in tariff revenue, significantly higher than the $38 billion collected a year ago across the same period. Over the full year the Tax Foundation estimates that tariff revenue will increase by about $150 billion, followed by $180-$190 billion in 2026 and 2027. And about $1.5 trillion over the next ten years. More than two thirds of this is from the tariffs imposed using IEEPA authority, which is now in doubt.

It also provides less revenue offset to the massive deficit-financed tax bill that is moving through Congress right now. Tariffs were never going to completely offset the deficit increase from the tax bill, but even about $1.5 trillion over the next ten years would provide a reasonable offset to a tax bill that is likely going to increase deficits by $4-5 trillion over the next decade.

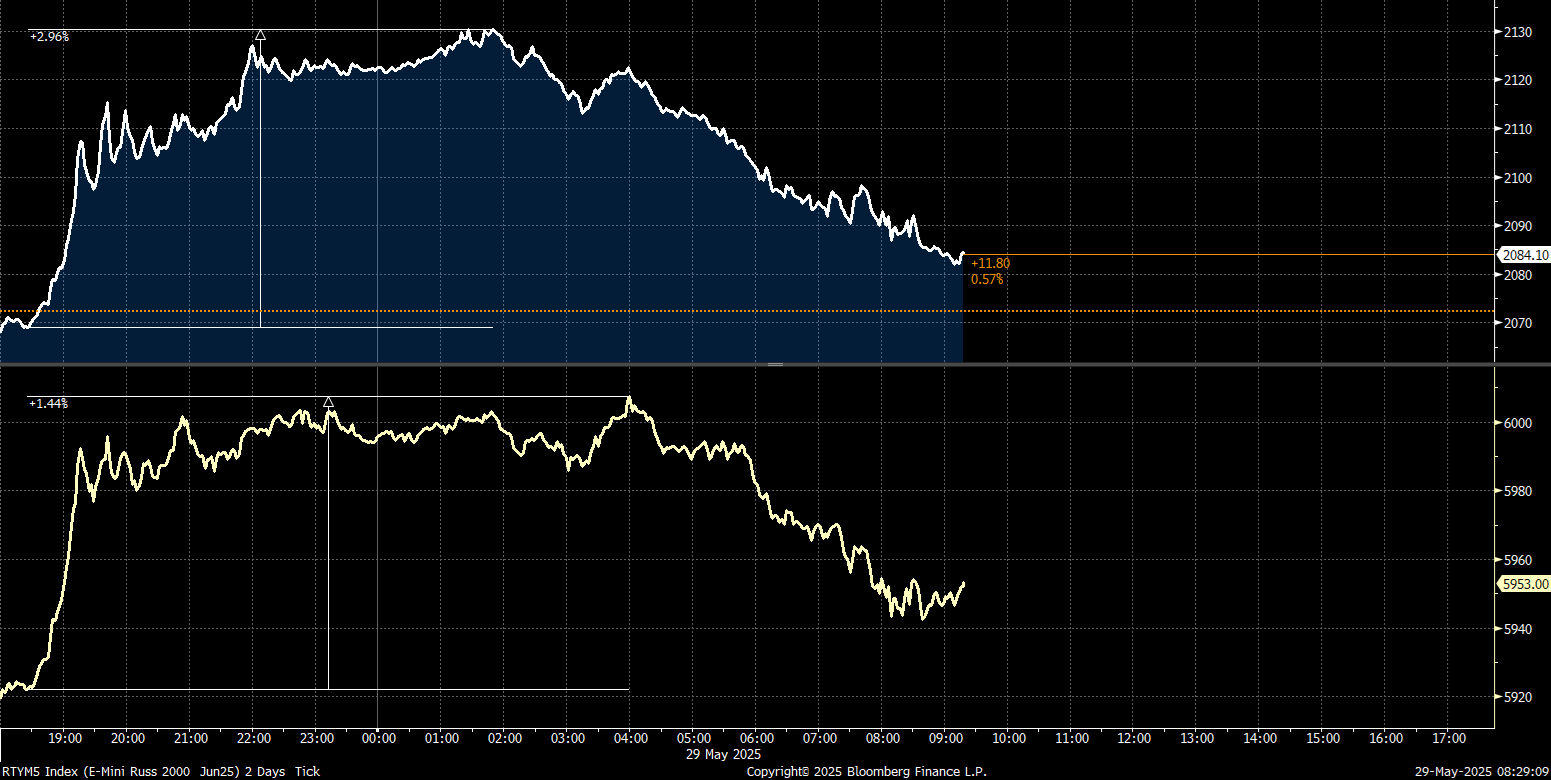

Markets Loved the News, At First

Markets reacted very positively to the news right off the bat, with equity market futures breaking higher on Wednesday night after the news broke. Another sign that markets are extremely reactive to any news around the tariff issue – a key theme of the last two months.

The small cap Russell 2000 index futures raced to a 3% gain overnight (top panel in the chart below). However, most of those gains reversed by market open on Thursday. S&P 500 futures gained as much as 1.4% overnight before losing about half of it by morning (bottom panel in the chart).

Small cap stocks will be a major beneficiary of the possibility that the tariff mess is behind us, and so it’ll be interesting to watch if the Russell 2000 holds on to gains and manages to outperform its large cap counterparts over the next few days. That’ll tell us how investors in aggregate are assessing the ruling, let alone the possibility of it being reversed and/or the administration finding workarounds.

Irrespective of how things move forward from here, and there’s a lot of uncertainty around that, the court ruling is a reminder that the bedrock American principle of checks and balances still exist.

8017326.1. – 5.29.25 A

For more content by Sonu Varghese, VP, Global Macro Strategist click here