Liberation Day is here, but we’re still waiting to for the exact nature of our liberation.

- Will it be reciprocal tariffs, with the US reciprocating other countries’ tariff rates on US goods? These will be enormously complicated to implement.

- Or will it be President Trump’s preferred approach of imposing a blanket 20% universal tariff on all imports? This will be a lot simpler to implement, but will mean that US tariff rates surge to the highest levels since the 1890s.

- Or will it be a new, middle-ground option that the US Trade Representative’s Office is prepping at the 11th hour amid pushback from businesses, labor, and Republican politicians?

There’s probably a reason the administration chose April 2nd as Liberation Day and not April 1st. It’s all very uncertain. And even after we get the announcement, things will remain fluid. America’s trading partners are likely to respond with retaliatory tariffs as well. The Trump administration has indicated that other countries can negotiate their way out of tariffs, and that likely applies to businesses too. Meanwhile, they’re also looking at possible bailout packages for those hurt by retaliatory tariffs, like American farmers. Farmers got a bailout in 2018-2019 as well, but, in my opinion, the bill for any package is likely to be much bigger this time around.

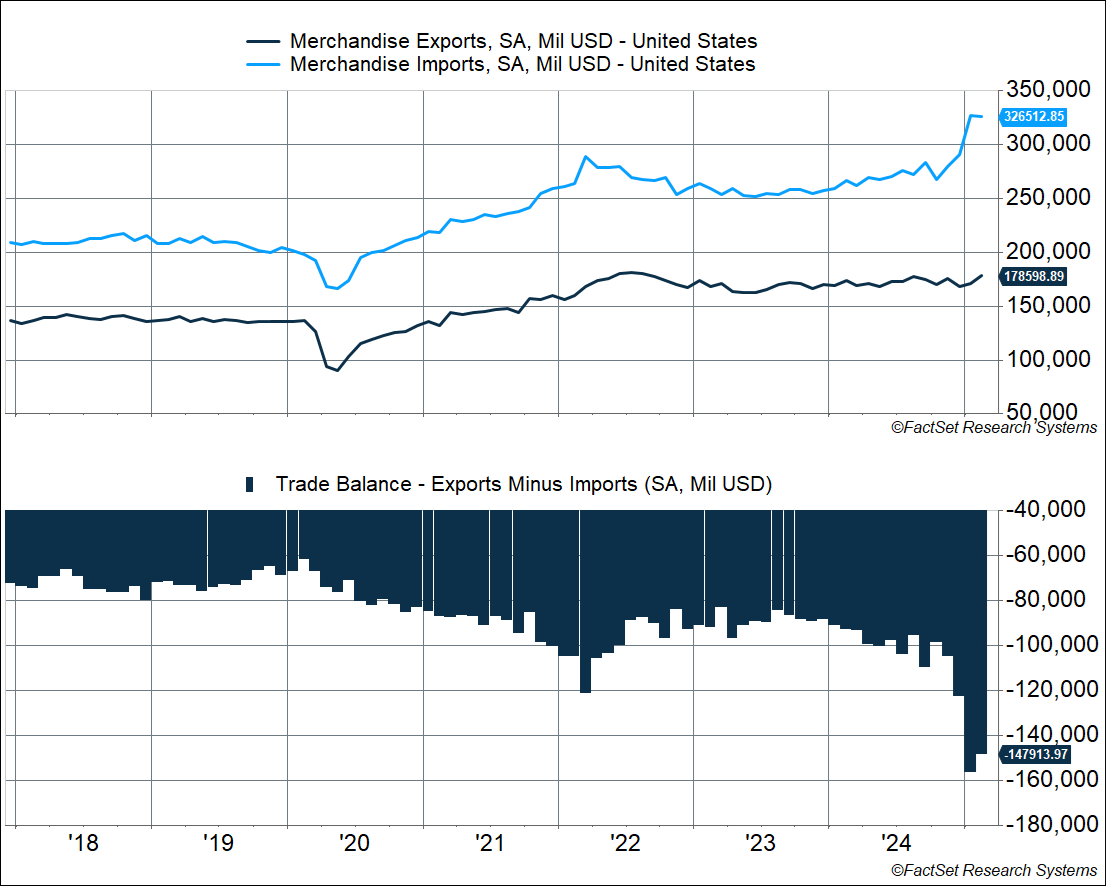

Of course, consumers and businesses aren’t waiting around for policy to be clarified. They’re already acting to get ahead of tariffs. Goods imports have surged to record levels of over $320 billion over the last two months, especially from China, Canada, and Mexico. Meanwhile, exports remained below $180 billion, close to where they’ve been for two years now. That means the trade deficit for goods (exports minus imports) has surged. The goods trade deficit clocked in around $148 billion in February, over 60% higher than what it was a year ago. This ostensibly defeats the very purpose of the tariffs, which is to reduce the trade deficit by forcing Americans to buy more American goods.

Note that we already have several rounds of tariffs imposed on a variety of imports, including those from China, along with tariffs on steel and aluminum. A massive tariff of 25% is set to be imposed on imported finished automobiles and parts on April 2nd (which will be on top of any reciprocal tariffs).

All this is likely to create distortions in the way Americans purchase goods over the next month or two, or maybe longer if the tariffs keep getting postponed. They’ll rush to buy goods to get ahead of tariffs, and it looks like that’s already happening, from Canadian-made granola to vehicles.

Vehicle sales surged in March to a seasonally adjusted annualized pace of 17.8 million—that’s the highest level since April 2021 and well above the pre-pandemic pace. March retail sales are going to come in hot just on the back of auto sales. Of course, if most of these vehicles are imported, it’s not going to count to GDP. Neither will Canadian granola.

Uh Oh, Prices!

Auto dealers likely have inventory of non-tariffed vehicles for about two months or so (inventories are already running well below what they were pre-pandemic). The problem is that as demand rises, prices are likely to rise too—even ahead of tariffs, let alone if they’re never implemented.

The latest ISM manufacturing survey showed that firms are building inventories at current prices to get ahead of tariffs and related cost increases (including retaliatory tariffs from other countries). At the same time, the survey indicated that raw materials prices increased in March at the fastest pace since June 2022.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

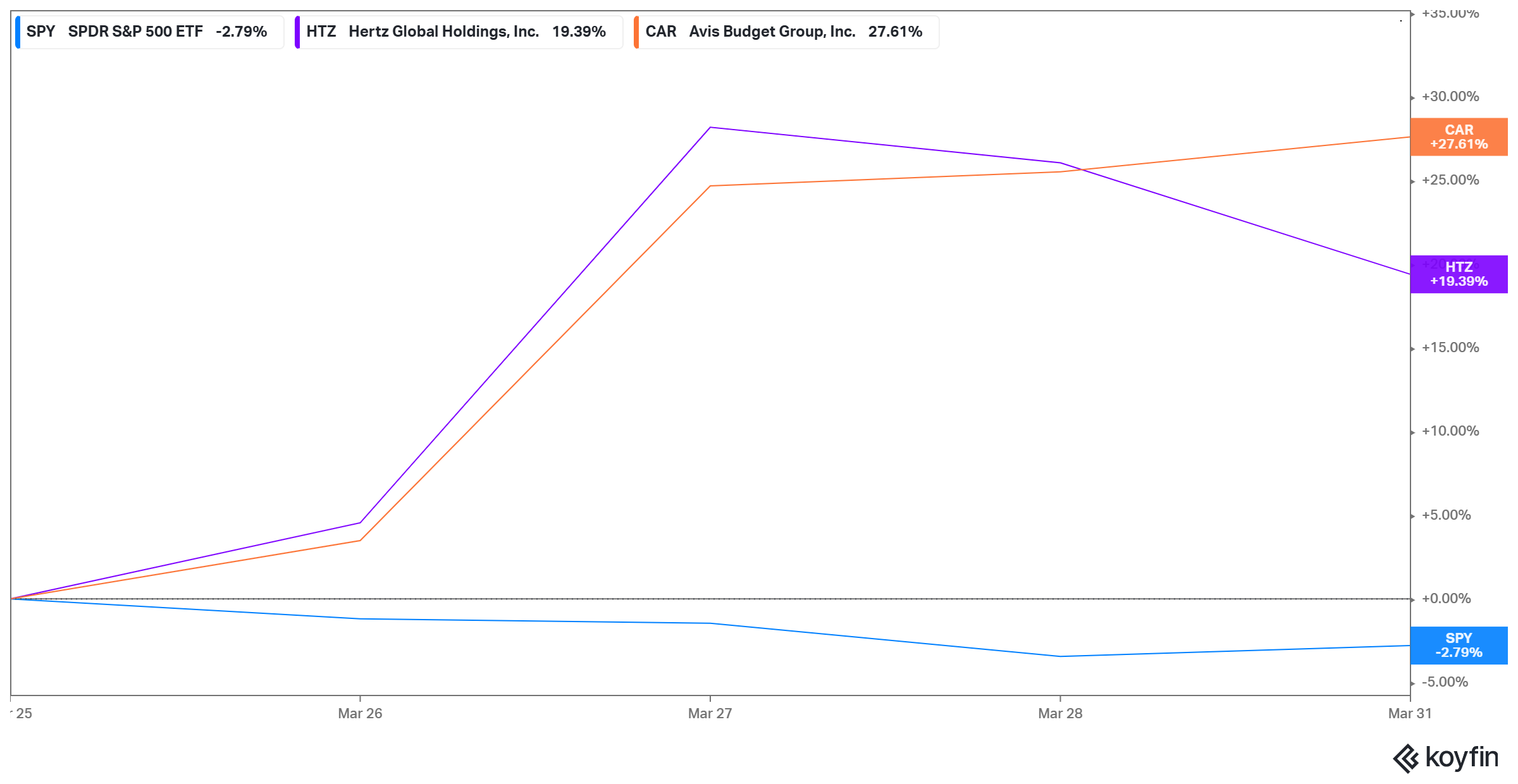

By the way, it’s not just foreign-made vehicles that will face tariffs, as a lot of vehicles assembled in the US use parts from abroad, parts which will also be tariffed at 25%. We could see consumers moving to the used car market after that, leading to a rise in used car prices. Stock prices for rental car companies like Avis/Budget and Hertz, who own massive used car fleets, surged 25% after the auto tariff announcement.

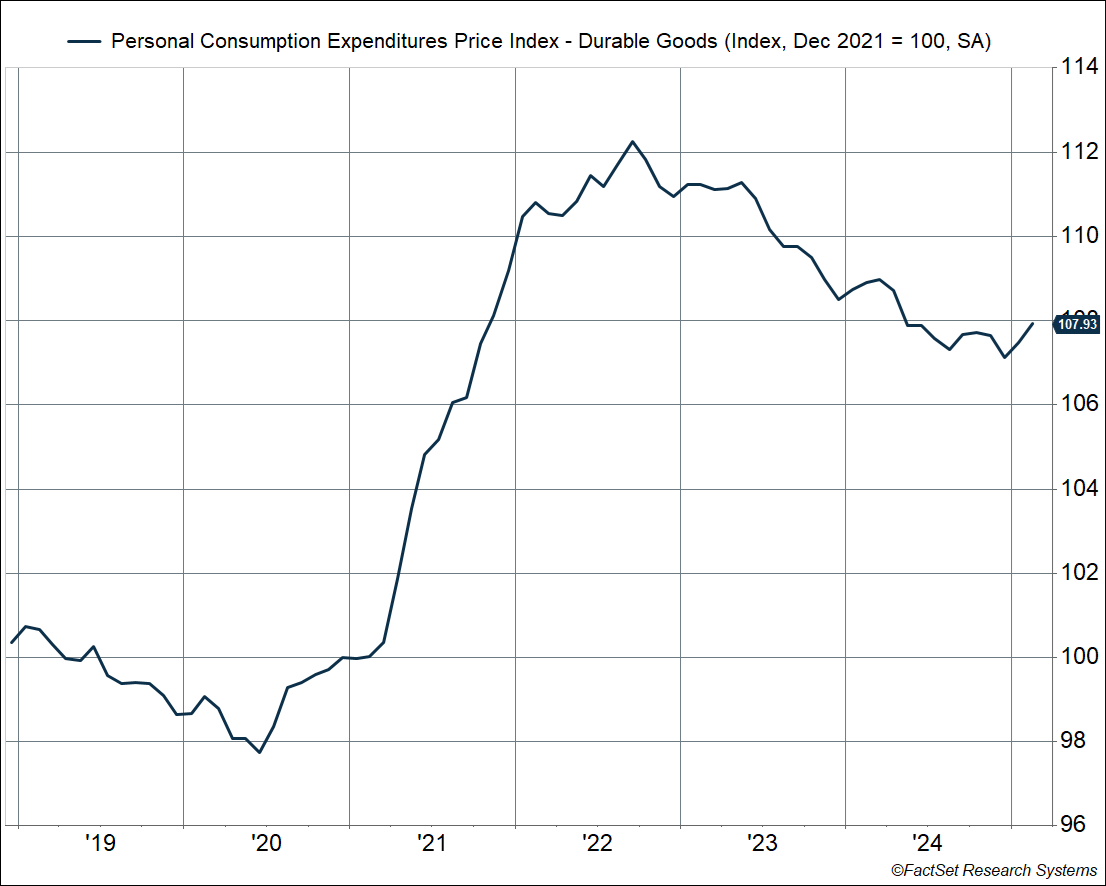

We could very well see prices increase for durable goods in general—items like vehicles, furnishings, and appliances—as consumers rush to get ahead of tariffs. A lot of this may be driven by vehicle prices, a throwback to 2021 – 2022 when inflation surged as used car prices climbed 50%. The Personal Consumption Expenditures (PCE) price index for durable goods jumped over 12% over the eighteen months through June 2022, which took the price index to a peak of 7%. It’s very unlikely we see price increases of that magnitude again, but it could be more than enough to send core inflation above 3 – 3.5% by the end of 2025. In fact, we’ve already seen an uncomfortable rise in durable goods prices over the last couple of months (January – February), arresting the decline we saw in 2023 – 2024.

The Fed May Have a Big Problem on Their Hands

A jump in car prices could result in car insurance prices also jumping further down the road, which means the impact on inflation data could be staggered. We saw this dynamic play out over the last three years as well, when vehicle prices jumped in 2021 – 2022 and then car insurance prices took off in 2023 – 2024, keeping inflation elevated for longer.

This could be a big, big problem for the Federal Reserve.

The Fed could argue that the price increase is “transitory” (again!). After all, unless tariffs are continuously ratcheted higher, we should see prices jump one time and not much after that. That’s a shift in the price level, as opposed to persistent inflation. Of course, that is not to say it’ll be a pleasant experience for consumers (and businesses).

Over the last year, the Fed has been biased towards easing rates, as they looked to protect labor market gains. However, they were helped by the fact that the inflation outlook was positive, with goods deflation and shelter disinflation on the cards. That’s unlikely to be the case going forward, and we could be looking at one of these two scenarios:

- Prices increase on the back of tariffs, sending core inflation towards 3 – 3.5% by the end of 2025, but the unemployment rate doesn’t move higher. Under this scenario, the Fed is unlikely to cut rates in 2025.

- Prices increase, but the unemployment starts to rise above 4.5% or so. In this case, the Fed will need to make a very tough decision. Do they ease rates to protect the labor market even in the face of inflation data going in the wrong direction (even if they think it’s transitory)?

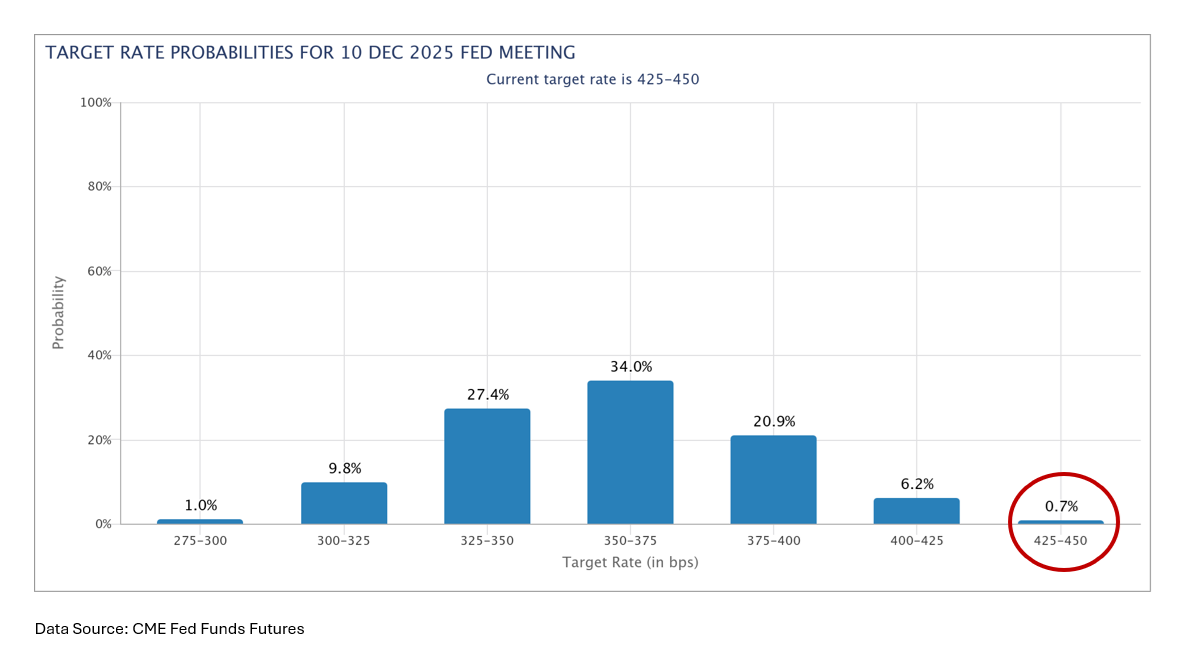

Markets are currently expecting about three rate cuts in 2025, starting in June. It looks like investors believe the unemployment rate is going to move sharply higher and the Fed will respond with rate cuts, irrespective of what happens with inflation. In fact, the probability of no cuts at all in 2025 is less than 1%, going by fed funds futures data. That seems really low. I still believe we’ll see about two cuts in the back half of the year, but the probability of no cuts this year is rising and is certainly much higher than 1%. If investors start to raise the probability of no cuts in 2025, expect to see more equity market volatility.

As we’ve repeatedly pointed out over the last couple of months, the biggest impact of the tariffs is that it pushes the Fed to pause on rate cuts. Elevated rates are already having a negative impact on the cyclical areas of the economy, including housing and manufacturing, and a prolonged pause from the Fed is likely to make matters worse. Note that if the Fed is forced to cut rates in the face of deteriorating labor market conditions, it’s very likely they’re behind the curve already, which means we’ll have an actual economic growth problem on our hands.

For now, we’re still in the camp that the economy will avoid a recession, but increasingly restrictive monetary policy will increase the risk of one over the next 12 months. At this point all we can do is keep a close eye on the data, while also looking under the hood to get beyond temporary distortions. It could be a messy few months.

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

7811157-0425-A