Federal Reserve (Fed) Chair, Jerome Powell, just gave us the most detailed description of how they’re thinking about policy in the face of massive tariffs. He was speaking at the Economic Club of Chicago, and participated in a Q&A after, with the former head of India’s Central Bank and University of Chicago professor, Raghuram Rajan. Rajan asked really insightful questions, drawing out more of Powell’s thinking than anything I’ve seen or read in the past.

Powell’s prepared remarks started off by saying the economy was/is in good shape, including labor markets and the inflation picture. He emphasized that the labor market is in a solid place

- Job growth has slowed, but lower layoffs and lower labor force growth has kept the unemployment rate low.

- Wage growth has moderated while outpacing inflation.

- The labor market is not a source of inflationary pressure.

I’m not sure if I’d paint as pretty a picture of the labor market as Powell, especially since hiring has been weak (payroll growth has been steady because layoffs are low). But ultimately, the last bullet is what is important because it tells you that all else equal, the Fed should be cutting now. There is no point keeping rates “meaningfully restrictive” (their own description) when higher rates tend to push inflation lower by lowering demand, which creates more unemployment and less income.

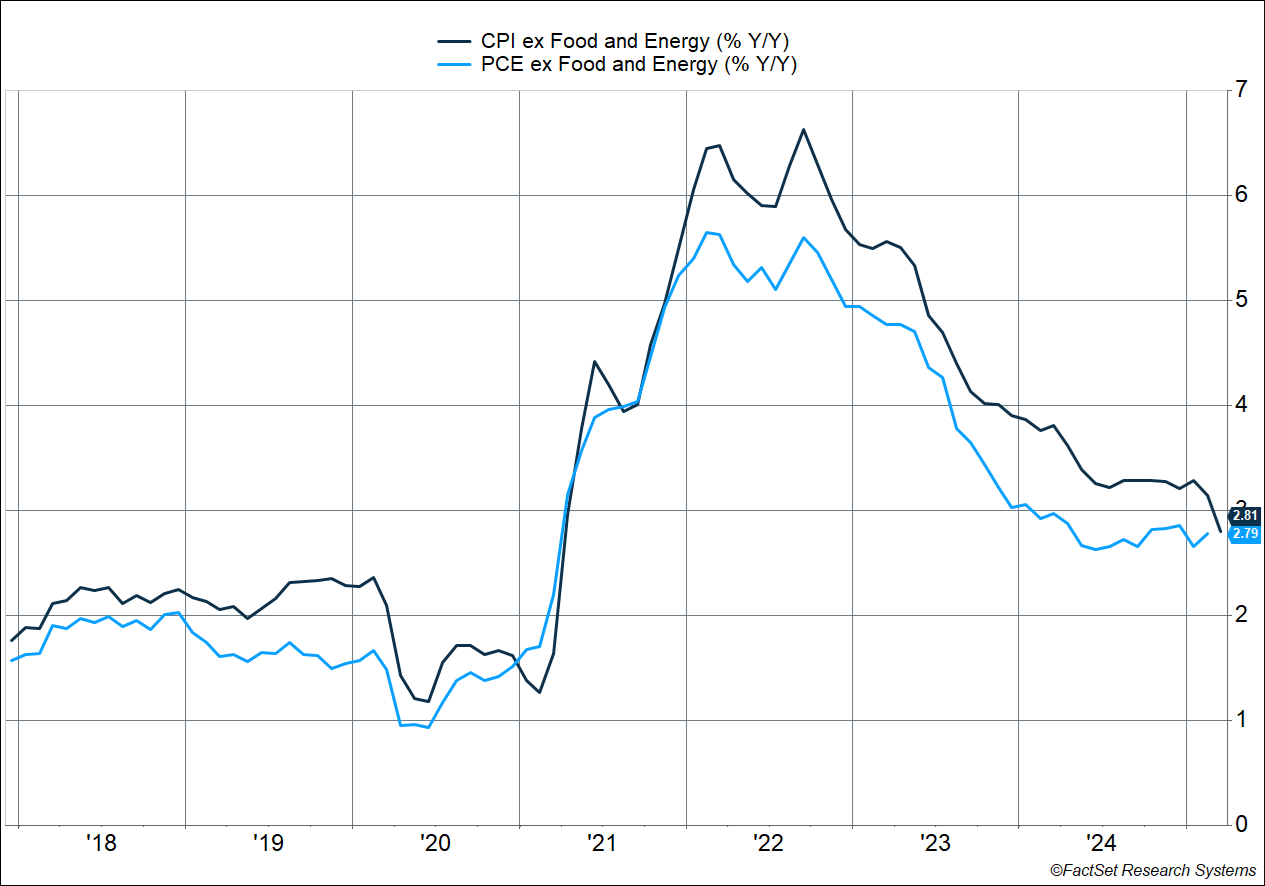

Moreover, the inflation data coming out has also been really positive, even though it’s still running a bit above 2%. Core Personal Consumption Expenditures (PCE), which is the Fed’s preferred inflation metric, is expected to rise just around 0.1% in March and clock in at 2.6% year over year. That would be the slowest pace since March 2021. The core CPI (Consumer Price Index) metric was really soft in March, rising just 0.06%, and is up 2.8% year over year, also the slowest pace since March 2021.

In short, things were going well. Until tariffs.

“Life Moves Pretty Fast” -Ferris Bueller

Powell quoted Ferris Bueller to summarize how the new administration’s policy has completely upended their picture of the economy as we move forward, including policies around 1) trade, 2) immigration, 3) fiscal policy (taxes), and 4) regulation.

The level of tariffs has been much higher than expected, and as a result the expected economic impact is likely to be higher too. In short, Powell said they expected higher inflation and slower growth ahead. The only good news there is that long-term inflation expectations, including within markets, appeared to be well-anchored around their 2% target. This is actually another way of saying investors believe the Fed will do what it takes to tame inflation. More than anything else, central bankers worry about losing credibility as inflation expectations surge, which is what happened in the 1970s. That loss of credibility itself could push inflation higher.

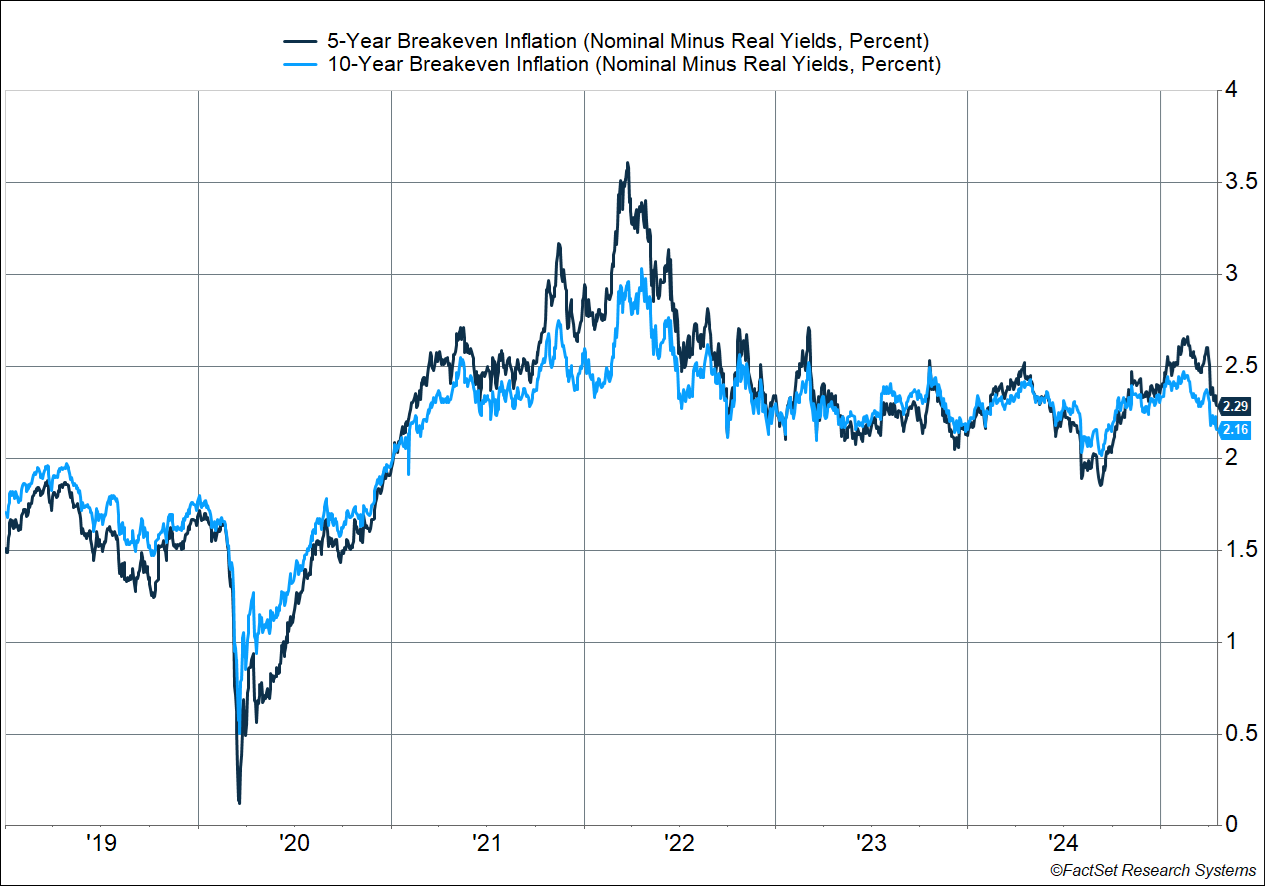

Currently, inflation expectations, as measured by breakeven inflation (the difference between nominal yields and real yields taken from TIPS securities), is running consistent with the Fed’s 2% target. 5-year breakevens are at 2.3% and 10-year breakevens are below 2.2%. Note that these track CPI, which tends to run 0.3-0.4%-points below the Fed’s preferred PCE metric. As I said, markets think the Fed can and will bring inflation under control. (This could also mean higher rates in the future.)

Powell believes tariffs are highly likely to generate a temporary rise in inflation through a one-time upward shift in the price level. But he thinks inflationary effects could also be persistent, and that’s going to depend on

- How large the tariffs are.

- How long the tariffs take to pass through to consumer prices.

- How long the Fed keeps long-term inflation expectations remain well anchored.

Powell said their main obligation is to keep inflation expectations well anchored, and to make sure a one-time increase in the price level does not become an ongoing inflation problem. They’re going to balance their two mandates, maximum employment and price stability. But he then added:

“Keeping in mind, without price stability we cannot achieve long periods of strong labor market conditions”

My translation: They’d like to achieve both sides of their mandate, but if forced to choose between taming inflation versus avoiding higher unemployment, they’re going to do what it takes to tame inflation first.

The language is very similar to what Powell used to say back in 2022 and 2023, when they were raising rates. At the time, they even said that a recession may not be avoidable, as they expected the unemployment rate to rise from 3.5% to above 4.6% (thankfully, it didn’t go higher than 4.2%). Powell and co were willing to do what it takes in 2022 – 2023 to tame inflation, even at the expense of the labor market. And Powell just sent a loud and clear message that they’re willing to do so again.

This is incredibly hawkish. The only way to be more hawkish is to explicitly say they’ll consider rate hikes once again.

Powell is also worried that extremely high tariffs, such as those proposed, could result in a supply shock that further lifts inflation, similar to what happened in 2022, when supply chains got clogged and led to more persistent inflation. Powell pointed out that in his discussion with several CEOs, they said that high tariffs on imported goods that are used as inputs into their processes are a big issue. Supply disruption can take years to solve and result in higher inflation for longer. An example: car supply chains may be disrupted and could take a few years to get fully resolved. And that assumes we have certainty about the level of tariffs, whether over the next year or even after the current administration.

This is where it would actually be beneficial for Congress to mandate the tariffs into law, as it would give a bit more certainty. The problem is Congress is not even close to being involved at this point.

Markets Expect Cuts That May Not Be Forthcoming

For the time being the Fed is going to wait for more clarity, i.e. more data. Keep in mind that the status quo is not a good place. Powell has repeatedly said that rates are meaningfully restrictive right now, and if income growth continues to ease, that means policy is actually getting tighter if they don’t do anything. That’s not good for cyclical areas of the economy, including housing and manufacturing, which are also going to be hit by the weight of tariffs.

We wrote in our 2025 Outlook that elevated interest rates are a risk. Since the tariff mess started, I’ve been writing that the biggest risk is actually the Fed pausing and sitting on their hands for longer. We still have no idea where tariffs will end up, let alone the economic impact. But what I suspected was that it would force the Fed to wait to cut rates again, and Powell just confirmed that.

It’s no surprise that the stock market did not like Powell’s message, with the S&P 500 dropping 2.2% on Wednesday (April 16th). One thing that was positive on the surface was that bond prices rose (as yields fell), providing diversification to stocks. But the message from the market seems to be that the Fed’s hawkish posture is going to drive the economy into a recession. In fact, Powell explicitly said they’re not going to do anything with rates until they see data, and if they’re going to wait to see the unemployment rate at an uncomfortably high level, it’s likely going to be too late.

And once the economy is in trouble, the market is betting that the Fed will cut fast, and cut deep.

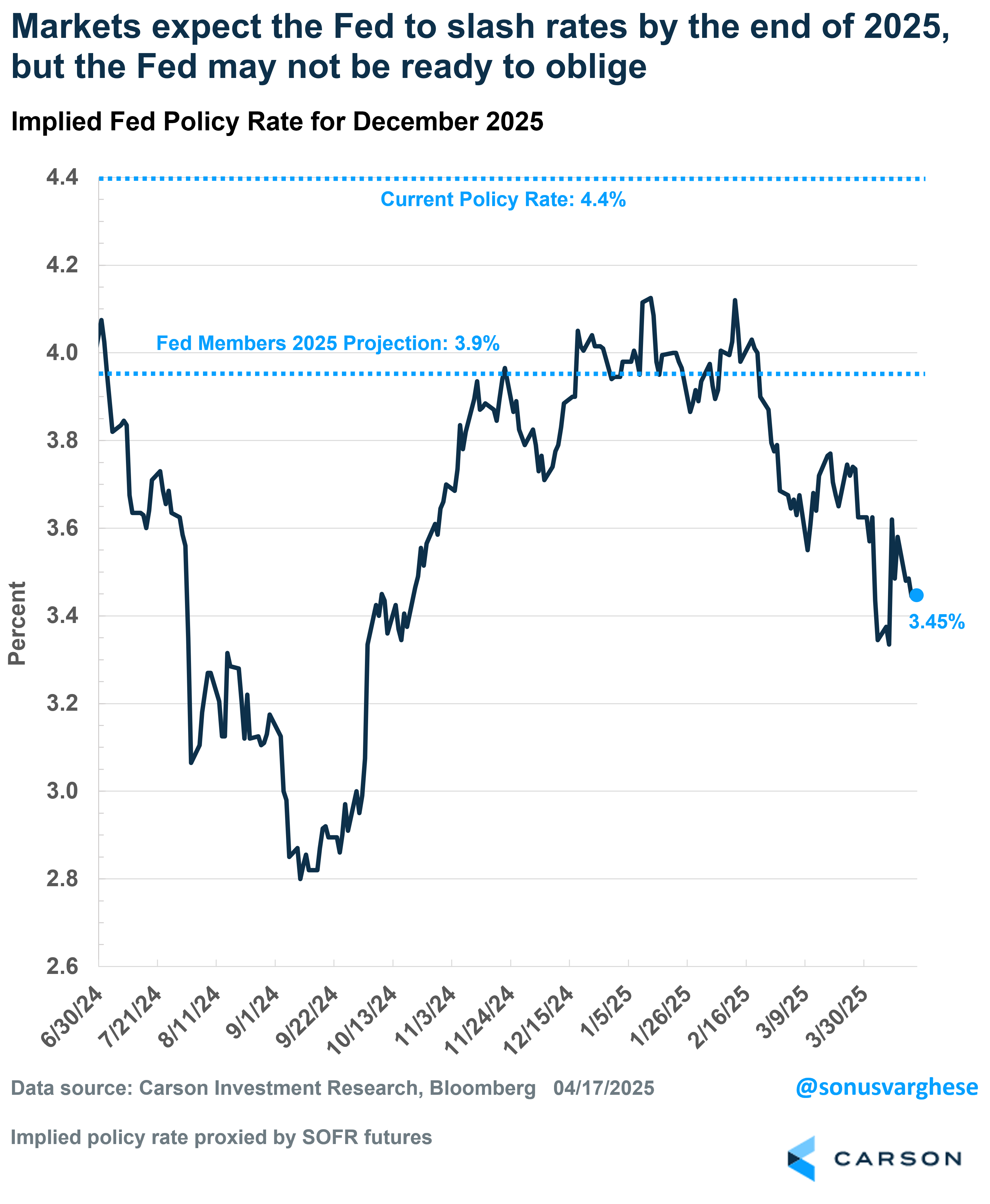

This is why the market is still betting on multiple rate cuts in 2025. Markets are currently pricing a policy rate of 3.45% for 2025, close to 1%-point below where rates are now, implying the Fed will cut at least four times (each cut worth 0.25%-points) over six months.

A Recipe for More Volatility?

I’m skeptical that the Fed cuts rates before September, if at all, in 2025. Which means the market will have to re-adjust expectations, leading to more volatility.

If the Fed does indeed cut, there are two paths, and both spell trouble, in my opinion:

- The unemployment rate surges, perhaps to over 4.5%, indicating the labor market is in deep trouble. By then cuts are likely to be too late, and that’s assuming they even cut. (Going by Powell’s comments, they may focus more on inflation.)

- Trump fires Powell “for cause” and installs his person, who will presumably slash rates at his behest. This will be a massive blow for Fed independence. Normally, I’d say the odds are close to zero, but it’s clearly much higher right now. This is what the president said on social media platform X on Thursday morning:

I’ll close with something Powell pointed out at the event. What we’re seeing now are in fact fundamental changes to long-held US policy. There’s no modern experience with this. Even the Smoot-Hawley tariffs were 100 years ago, and these are larger. That means there’s structural uncertainty as well, beyond immediate uncertainty related to tariffs (how much, on whom, for how long, etc). What’s going to happen is that businesses and households will step back from making decisions. He hopes things will become more certain, but that will depend on their understanding of what is normal, or rather, the new normal.

Ultimately, if uncertainty remains higher, it will weigh on investment and expected rates of return will have to be higher (to compensate for higher risk). If US risks are structurally higher, it will make investing in the US less attractive. Powell noted that we don’t know that this will happen, but that will be the effect. It’s incredible that the country’s chief central banker is saying this.

If you ask me, we’re clearly in uncharted waters now.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

7874650.1-0425-A