Well, that didn’t take long. Since the Fed’s decision to hold interest rates steady on Wednesday- presumably waiting on continued solid data supporting their case – the data confirmed otherwise. Thursday’s set of economic data saw initial jobless claims rise to their highest level in a year, alongside a weak manufacturing ISM number. Stocks fell and bonds rallied as yields fell. Unit labor costs came in below expectations as well, indicating continued fading inflationary pressures. Missed in this news flow was a stronger than expected productivity number reported Thursday, something we’ve been writing about all year.

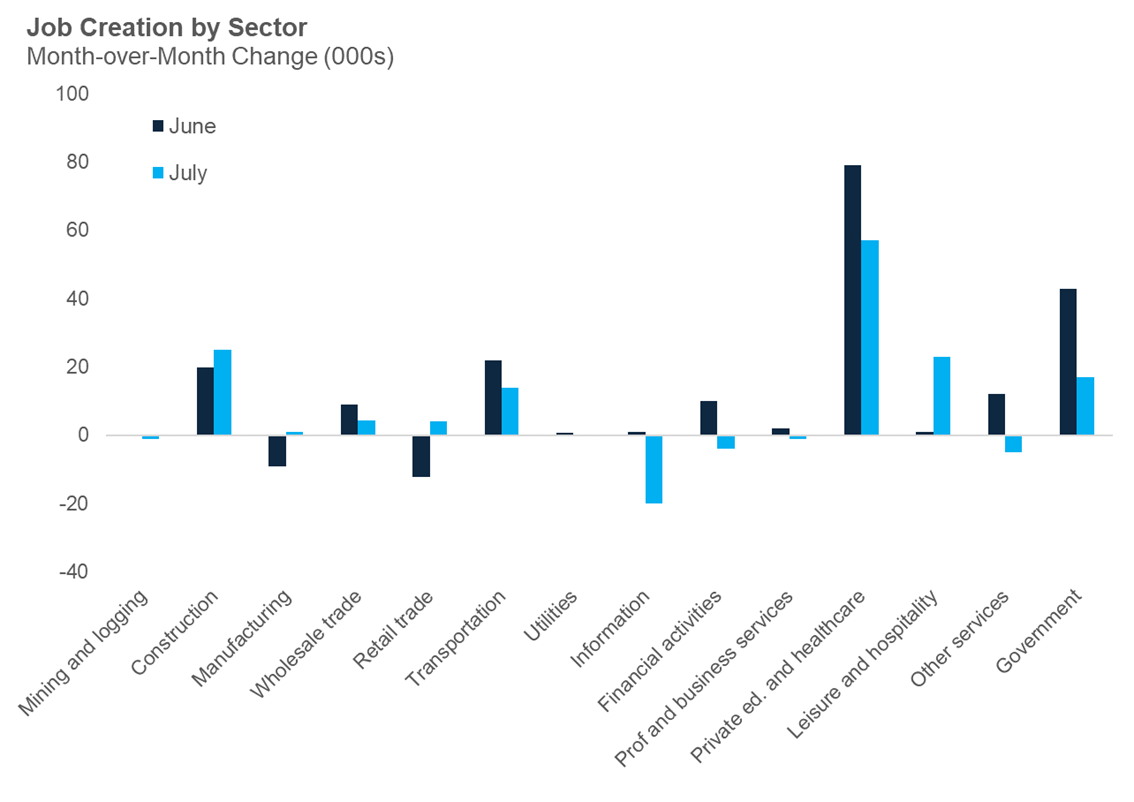

Friday’s non-farm payroll number missed expectations at only 114,000 jobs versus expectations of 175,000, with the prior month revised lower as well. Healthcare and government, which had dominated prior reports, showed less of an impact on the July numbers. While 114,000 jobs created was below expectations, the number was still positive and not the lowest we’ve seen in the past year (April came in at 108k jobs). There are also indications that hurricane Beryl impacted the number based on how the data is collected. Lastly, the increase in construction jobs was interesting, as that came in at 25,000 jobs.

Source: Bureau of Labor Statistics 8/2/2024

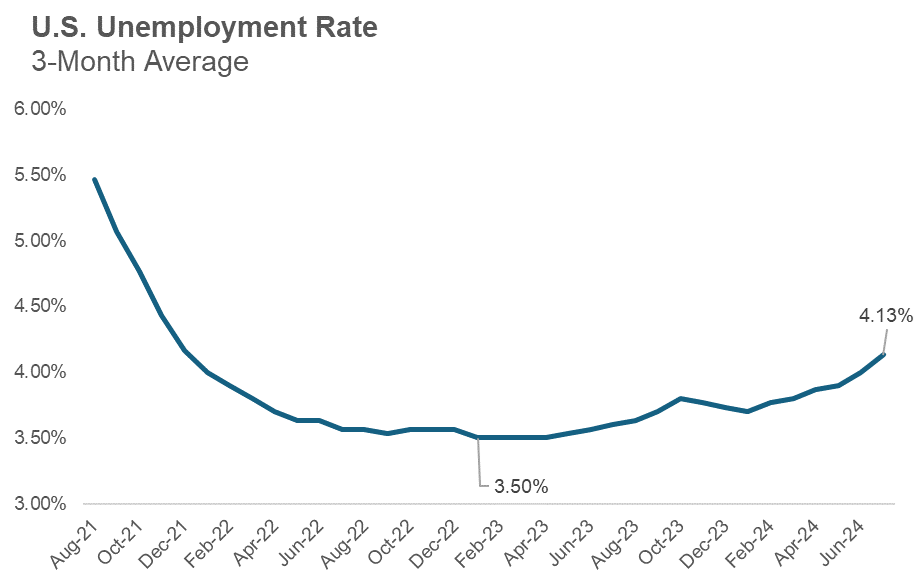

In this report, all eyes were on the unemployment rate, which has been creeping higher over the past several months. The unemployment rate came in above expectations at 4.3%, triggering the Sahm rule (she said it herself on radio) and immediately unleashing the pundits to opine on the state of the economy and the Fed’s decision (or lack thereof) on Wednesday. With the benefit of two days of data and hindsight, all signs indicate that the Fed should have already begun cutting interest rates.

Source: Factset 8/2/2024

The Good News

While the initial reaction to the news has not been positive for risk assets, the world isn’t ending quite yet! Bond markets are doing the Fed’s job on its behalf, with interest rates across the curve falling substantially, easing overall financial conditions. Data this week on employment costs and hourly earnings have come in cooler than expected, and rental inflation has been negative year-over-year for nearly a year now. Inflation is no longer an issue, and with signs of a cooling labor market, the Fed has every reason to cut interest rates. September is all but certain, and now many are pointing to the potential for a 0.50% cut to play catch up, as Friday morning showed more than a 70% chance of a 0.50% cut in September, up from the teens the day before.

Speaking of bonds, they have been on fire lately thanks to yields dropping. It wasn’t that long ago that bonds and stocks both dropped together, so diversified investors are once again getting some protection out of bonds when stocks fall.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

That is the good news – while the very hot labor market has now cooled some, the economy is still on good footing as we saw in the preliminary GDP numbers earlier in the week. There are very few, if any signs, of excesses and corporate America is in a strong financial position. The biggest issue currently is too tight of monetary policy – this is the longest the Fed has ever kept their target rate above 5% with unemployment below 4% – and the Fed has plenty of ammunition to make that adjustment and do so quickly. The Fed’s Economy Policy Symposium in Jackson Hole, WY later this month will be the next major event to watch. Historically, monetary policy shifts have been strongly signaled at this meeting, and indications of the size of the September interest rate cut will be highly scrutinized.

For more content by Grant Engelbart, VP, Investment Strategist click here.

02350226-0824-A