The phrase “chaos is in the air” is often casually stated. However, it is extremely applicable to describe the situation that the airline industry is currently enduring. With the upcoming Memorial Day weekend frenzy of vacationing and travel, consumers will experience their own version of chaos, but beneath the surface, airlines are facing their own turbulence. Company shutdowns, attempted mergers, increasing jet fuel costs, and rocky consumer sentiment have all occurred this year and have clouded the industry outlook for both investors and the companies themselves. As a result, airline companies have faced volatile stock performance so far this year where there is a mix of companies who have positioned themselves to be resilient to present geopolitical and industry factors, and others who have not. With so much going on and new stories arising frequently, it is important to unpack what is occurring within the airline industry.

Surging Fuel Costs

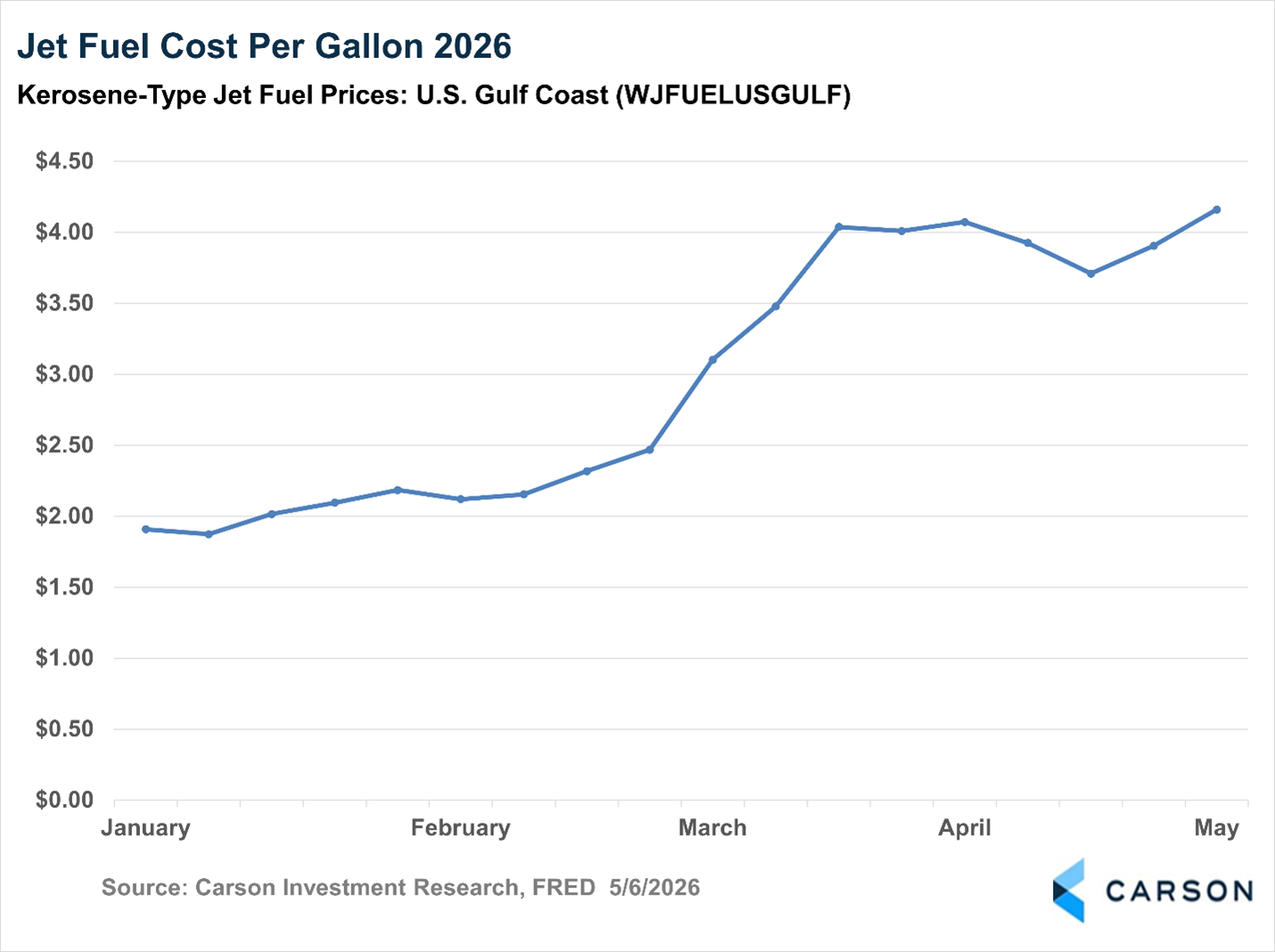

The tip of the iceberg for issues surmounting throughout the airline industry stems from the geopolitical tensions over the Strait of Hormuz, which has affected global oil supply routes and has since spiked jet fuel prices. Before this most recent rise in jet fuel, the industry was spending roughly 25% of its operating costs on fuel; an unexpected spike in this expense vastly changes the operating strategies of these companies. Some airline executives have been open to the fact that they will be looking to increase fares this year to offset the increasing fuel costs that the industry is currently facing. Executives have also alluded to a conundrum with a resilient market where higher fares have not impacted demand for tickets yet. A quote from United Airlines Chief Commercial Officer Andrew Nocella, “I think the longer the price of fuel remains in this range, and the longer consumers pay these prices — and airlines get used to this revenue stream — the more likely it is to stick,” shows some unfortunate truths to the consumer on the decision-making outlook for potential price decreases. To better demonstrate the sharp increase in jet fuel costs that are such a focal point in the industry, the chart below illustrates this current upward trajectory of the cost per gallon since the beginning of the year.

Zooming out, this surge in price per gallon within a five-month period can be put into perspective by comparing it to the $2.09 average cost per gallon over the last 10 years. Today’s $4.10 price per gallon is nearly twice the 10-year average. The only other timeframe over the last ten years in which the cost per gallon broke the $4 threshold was between April and the end of June in 2022, which aligned with the conflict between Russia and Ukraine. Geopolitical tensions in both 2022 and 2026 have resulted in the elevated costs of this fuel, and in turn resulted in higher ticketing and ancillary costs from the airlines onto the consumer.

Bankruptcies and Blocked Mergers

Such energy and other operating costs have recently shown to be too much of a financial strain for some companies to survive. On May 2nd, Spirit Airlines filed for bankruptcy for the second time since November of 2024 and grounded all flights and canceled all future operations. This shock occurred after the airline failed to acquire a government bailout of $500 million. Spirit is working to repay customers who have paid for more than 4,000 scheduled flights that have since been canceled, which has seemingly sent travelers scrambling for alternative options to fulfill their scheduled plans, which could lead to higher fare costs from other airlines due to surging demand. Prior to their bankruptcy, Spirit served an important role in the airline industry as being known as a budget-friendly airline; with its absence, a company may try to capture this existing market share if it is able to, due to operational and financial constraints. If one airline jumps to mind for a new low-cost alternative, Frontier Airlines sees themselves as the next footing for customers searching for lower fares. Frontier’s parent company projects that the absence of Spirit Airlines will contribute to an estimated 3-5% increase in revenue per seat on their flights.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

Spirit is not unique in its struggles; however, they were not approached for a potential merger recently, as was American Airlines. United Airlines recently approached American to initiate talks of a potential merger. American Airlines has been lackluster in its recent financial performance with high amounts of issued debt and a first-quarter net loss of $382 million. Despite this posted loss, first-quarter revenue totaled $13.91 billion and represented the company’s highest-ever revenue in a first quarter. American Airlines Chief Executive Robert Isom rejected further dialogue from United Airlines after they were propositioned for a potential merger, viewing the potential deal as “anti-competitive” and bad for both the industry and the consumer base. If these two companies were to have come to an agreement and viewed this as a mutual interest and pursued the merger, the combined market share would encompass roughly 40% of domestic airline travel in the United States. Due to the vast size of that newfound market share and consumer reliance on one single airline, it was speculated that courts would not allow this merger to go through due to potential impact on pricing and antitrust hurdles under U.S. law.

Recent Airline Stock Performance

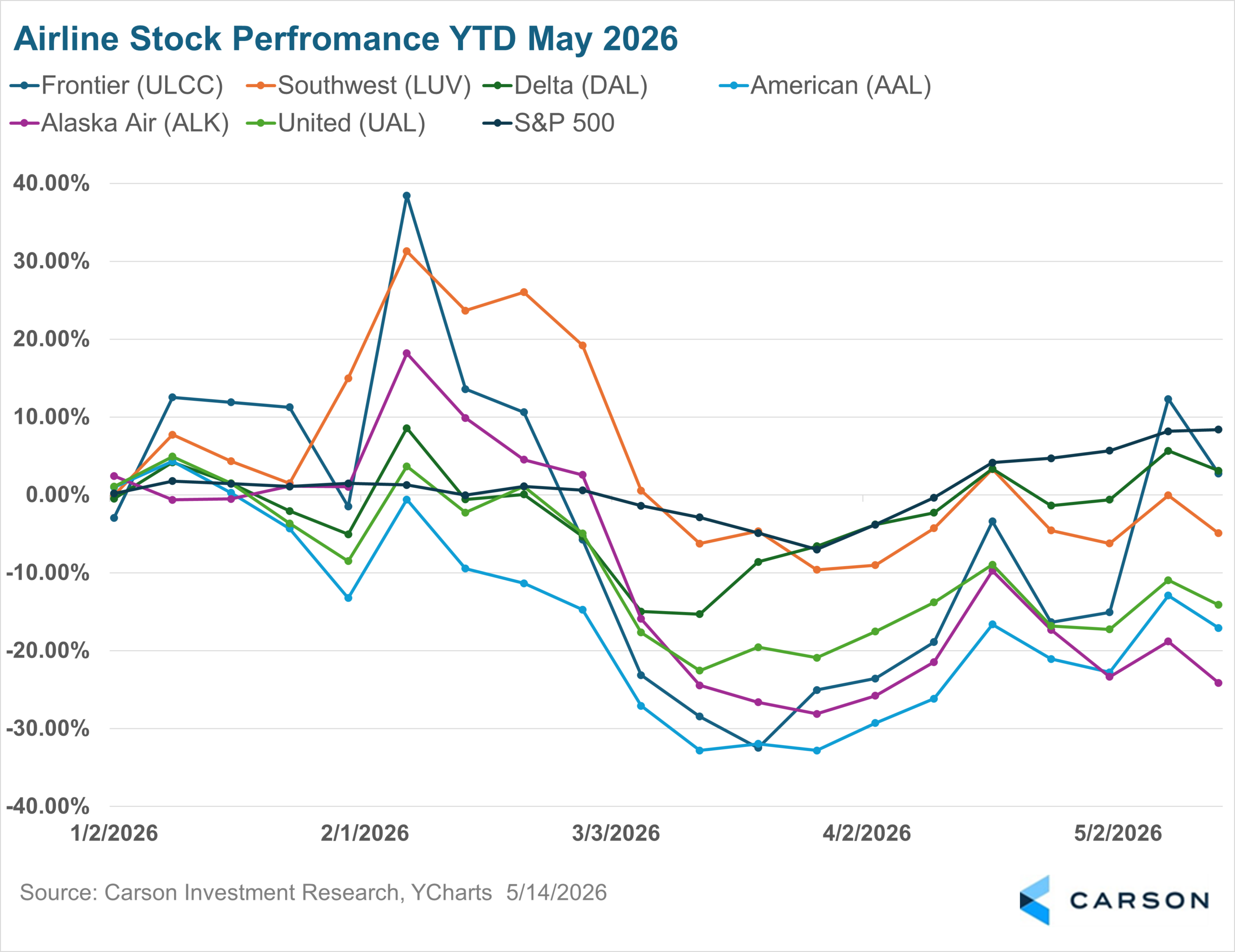

Like all things, any disruption can lead to downstream effects for a company or an entire industry at once. Since the beginning of 2026, airline stocks have felt the impacts that have stemmed from fuel costs, government shutdowns impacting TSA screening, and individual companies present in the headlines for bankruptcies or potential mergers. Shown below is a year-to-date performance chart of the major domestic airlines, which demonstrates the market behavior associated with the industry impacts they are facing.

There was excitement for airline stocks at the beginning of 2026, shown in the chart above some companies had Q4 earnings calls and other strategical intangibles that elevated their early 2026 performance. Most notably by mid-February, Frontier almost surpassed a 40% YTD return after they delivered strong earnings beat. Frontier reported that their EPS of $0.23 beat projected forecasts by 91.67%. Another exciting early 2026 leader was Southwest Airlines, who drew much attention from their stark change in seating and baggage policies of the past. Their strategical repositioning of charging for the ability to assign your seat as well as now charging for checked bags may have led to a high jump of adjusted EPS from 2025 ($0.93) to 2026 ($4). Southwest eclipsed 30% YTD performance shortly into February that may have come from this strategical pivot and revenue growth.

Fast forwarding through recent geopolitical tensions to today, there are two positive YTD performers even after such momentum earlier in the year, Delta and Frontier. Frontier reported the highest revenue in their company’s history in Q1 of $1.1 billion adjusted and a 17% increase year-over-year. Pivoting to Delta, which most notably is the only U.S airline that owns its own oil refinery, which may help the company with a provided hedge in times of high energy costs. Delta reported earnings for Q1 in early April which detailed that they beat earnings with a record revenue of $14.2 billion adjusted amidst the burden of high fuels costs on the industry. As mentioned earlier, United Airlines CCO Andrew Nocella stated that due to a persistent demand, even with rising fares, companies may be comfortable with maintaining their price points in the future, regardless of potential fluctuation in energy costs that the companies bear. It presents a point to monitor for how companies like Delta, Frontier, and even American mentioned earlier who have achieved record revenues will strategize their pricing structure if fuel costs are to lower. If there is an unshaken demand for their services even with higher fares, it boils down to basic economic theory of inelastic demand. Obviously, there are other means of travel for certain trips, but for many, there is truly a lack of alternatives for the consumer due to time constraints of travelers and the necessary mode of transportation needed to reach their destination. With that principle, it could be expected that prices at least remain, if not increase, to the consumer.

In my opinion, volatility is not something new to the Airline industry. Watching how companies handle, adapt, and navigate recent volatility brought on by high operational and energy costs, amongst noise from big players in the industry, will ultimately separate those companies that are prepared and able to take on such challenges, and those that are not. Even though the airlines are facing intense operational pressures, the consumer demand has remained resilient, leading to record revenues and a potential point-of-no-return from a pricing standpoint. The foremost data points to keep an eye on from an investor’s perspective while reviewing the airline industry are monitoring the price of jet fuel and how that develops, coinciding with government tensions, and if they diminish to create breathing room for these companies and their operational costs. As of now, the captain still has the ‘fasten seat belt sign’ illuminated above investors’ heads amidst the current volatility in the industry.

By Joel Riha-Aldrich, Analyst, Investment Research

8933451.1.- 18MAY26A