Second-quarter bank earnings are around the corner, and expectations are perhaps correctly elevated across the board. Many of the larger firms in the sector may have just seen record-breaking quarters thanks to robust capital markets activities driven by equity issuances. And many of the smaller firms may be benefitting from robust lending and banking activity as the macroeconomic backdrop remains constructive.

Playing Catch Up

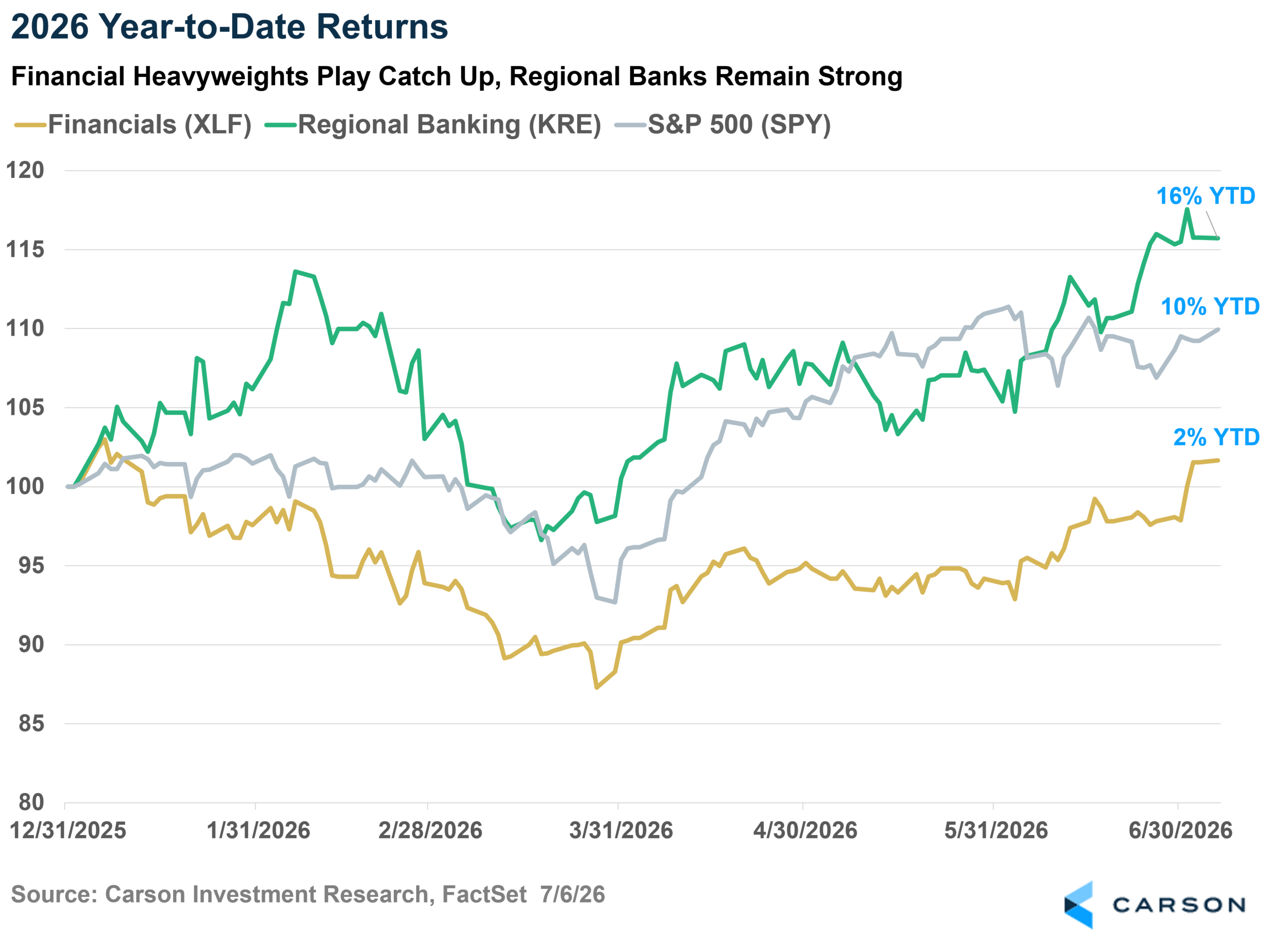

Investors in the financial sector have lagged so far in 2026, as the Financial Select Sector SPDR ETF (XLF) has underperformed the broader market year-to-date. As shown below, the XLF is up a measly 2% so far in 2026, though in the last month it has narrowed its gap relative to the S&P 500 by a substantial margin. This relative catch up may have been driven by a record-breaking quarter in equity issuance, as my colleague Sonu Varghese wrote about. Gross equity issuance – equity issuance minus repurchases – had already turned positive in the first quarter which represents a stark turnaround from recent history. And many high profile equity issuances across the technology sector likely means this data had turned even more positive in the second quarter. All told, these fundamental drivers for many businesses in the financial sector appear to be the most supportive in years and may be driving investors expectations for robust results this coming earnings season.

Regionals Remain Strong

A continuing industry of strength in the financial sector remains the regional banks. The SPDR S&P Regional Banking ETF (KRE) has been outperforming the S&P 500 for much of 2026, and has recently extended its outperformance as shown above. Regional banks are often seen as a better gauge of underlying credit conditions than the broader sector as these companies generate earnings from more traditional banking activities than the tech-related activities of the sector’s heavyweights. So, the outperformance of the regional banks this year suggests investors are growing confident that lending conditions remain favorable rather than deteriorating.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

The macroeconomic data reinforces that view. According to the Federal Reserve’s H.8 banking data, loans and leases held by U.S. commercial banks recently climbed to nearly $13.9 trillion, reaching another record high after expanding steadily throughout the year. This data represent growth in credit of over 6% year-over-year throughout the course of the second quarter. Credit creation remains one of the clearest indicators of economic activity, so continued expansion in bank lending suggests both borrowers and lenders remain confident in the economic outlook.

The Financial sector’s resurgent performance during the second quarter was built on two strong fundamental trends: record-breaking capital markets activity, and strong credit conditions. Although expectations and stock prices across the sector are now higher than they have been recently, perhaps the expectations are well founded as capital markets and lending conditions remain encouraging.

For more content by Blake Anderson, CFA®, Director, Portfolio Management, click here.

9007663.1. – 6JULY26A