The February employment report was a bit mixed. It didn’t tell us much that is new about the US economy, but that in and of itself is a story, depending on your expectations:

- If you were expecting near recession-like conditions, we don’t have that

- If you were expecting GDP growth to be closer to 3% (like the last two years), you have to re-rate that expectation to something much closer to 2% (if not slightly lower in the near term)

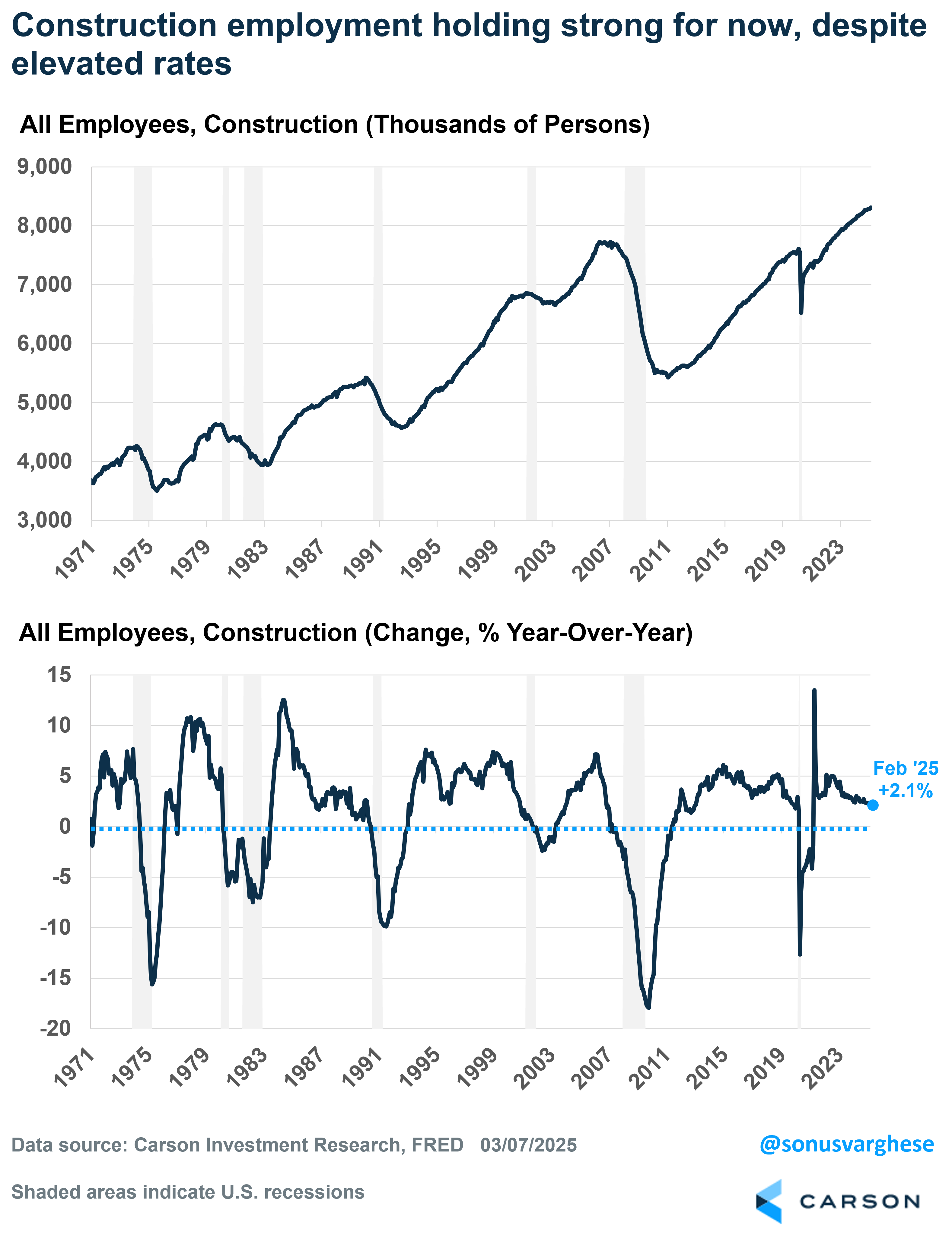

The economy created 151,000 jobs in February, more or less along expectations. Of course, as I’ve pointed out in the past, monthly data can be noisy and that’s why a 3-month average is useful. That’s running at strong 200,000 pace right now, thanks to a massive 323,000 gain in December. In reality, job growth is likely running between 140,000 – 180,000. That’s not bad, and slightly ahead of what’s needed to keep up with population growth. The big picture is that we’re not anywhere close to a recession. In fact, job growth in the construction industry, which typically foreshadows broad weakness in the labor market, is at cycle highs and up 2.1% from a year ago. That’s a slower growth pace than a year ago, but nothing close to what would be concerning. This is especially notable, given the drag on residential investment from high interest rates. Yes, the Atlanta Fed GDP Nowcast currently has Q1 real GDP growth at -2.4%, but I discussed why this is a flawed metric in my previous blog.

But … The Economy Has Slowed Down

The US economy grew at an annualized pace of almost 3% (2.9% to be exact) over the last two years, after adjusting for inflation—faster than the 2010-2019 pace of 2.4%. Even as recently as six weeks ago, it seemed like the market narrative, and sentiment, was expecting a rerun of this pace: stocks had risen to record highs and more tellingly, interest rates were really elevated as investors expected the Federal Reserve (Fed) to hold rates “higher for longer” amid a strong economy. In fact, there was a notion that the Fed even “got it wrong” by cutting rates as much as they did (they cut policy rates 1%-point from September through December). I’ll note that we were decidedly not in this camp. We’re optimistic about growth, and markets in 2025, but not overly so. As we wrote in our 2025 Outlook, we thought (and still think) interest rates are still too restrictive and a drag on cyclical areas of the economy (like housing and investment) and that tariffs are a threat that could create volatility (which is being manifested now).

Cue to today, and there’s been a big swing in sentiment. It’s not just the uncertainty from tariffs. Economic data has been coming in on the softer side (but not recessionary), and the February payroll data confirm the slowdown.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

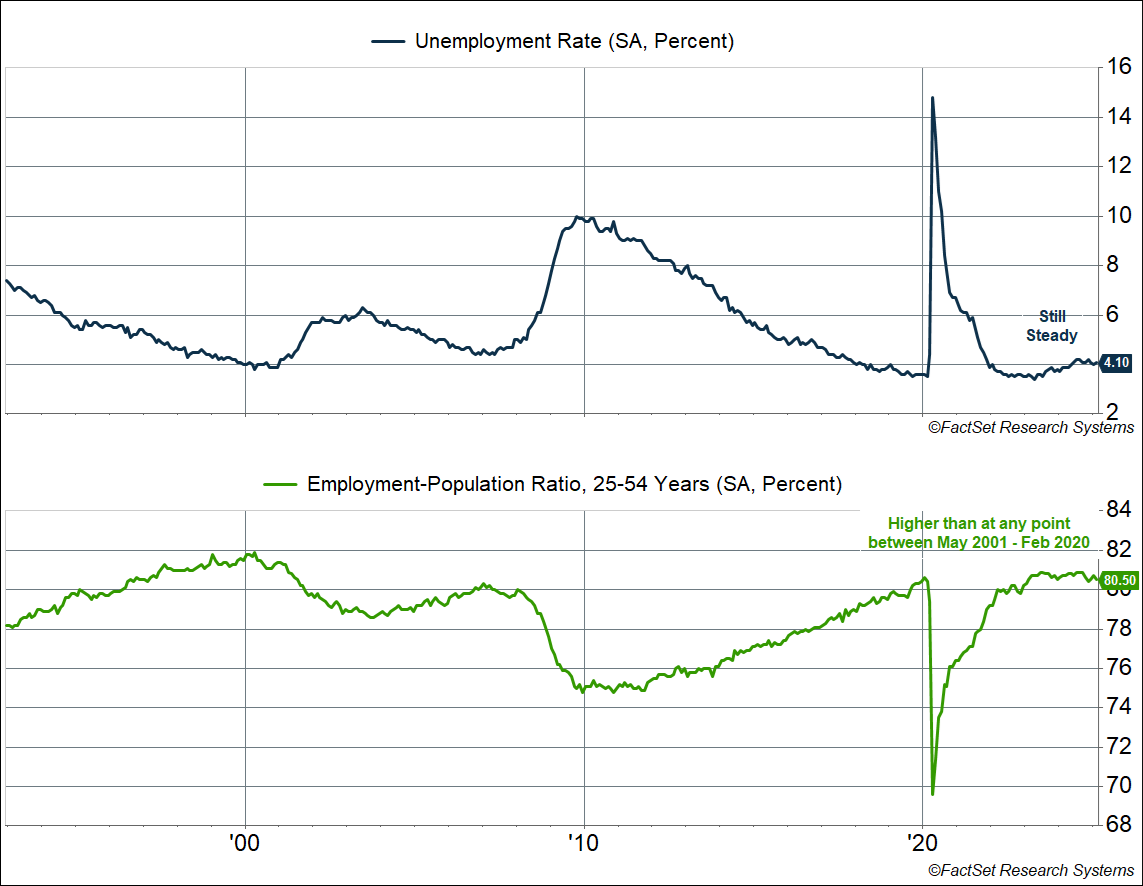

The unemployment rate rose to 4.1%, though that’s lower than historical averages. Even the prime-age (25-54) employment-population ratio, which corrects for an aging population and definitional issues around “who is unemployed,” pulled back from 80.7% to 80.5%, but that’s still higher than anything we saw over the last two expansion cycles (2003 – 2007 and 2009 – 2019). Other data show that layoffs remain low, but it’s getting a little harder to find a job.

Also, the composition of job growth tells us that we’re not getting the cyclical acceleration needed to take GDP growth above 2.5%. About 49% of jobs created in February were in health care and social assistance (+63,000) and government (+11,000). The DOGE is likely making its presence felt at the federal level, where jobs fell by 10,000, but this was more than offset by net job creation of 21,000 at the state and local level. (State/local government employment is almost 8-9 times larger than at the federal level.)

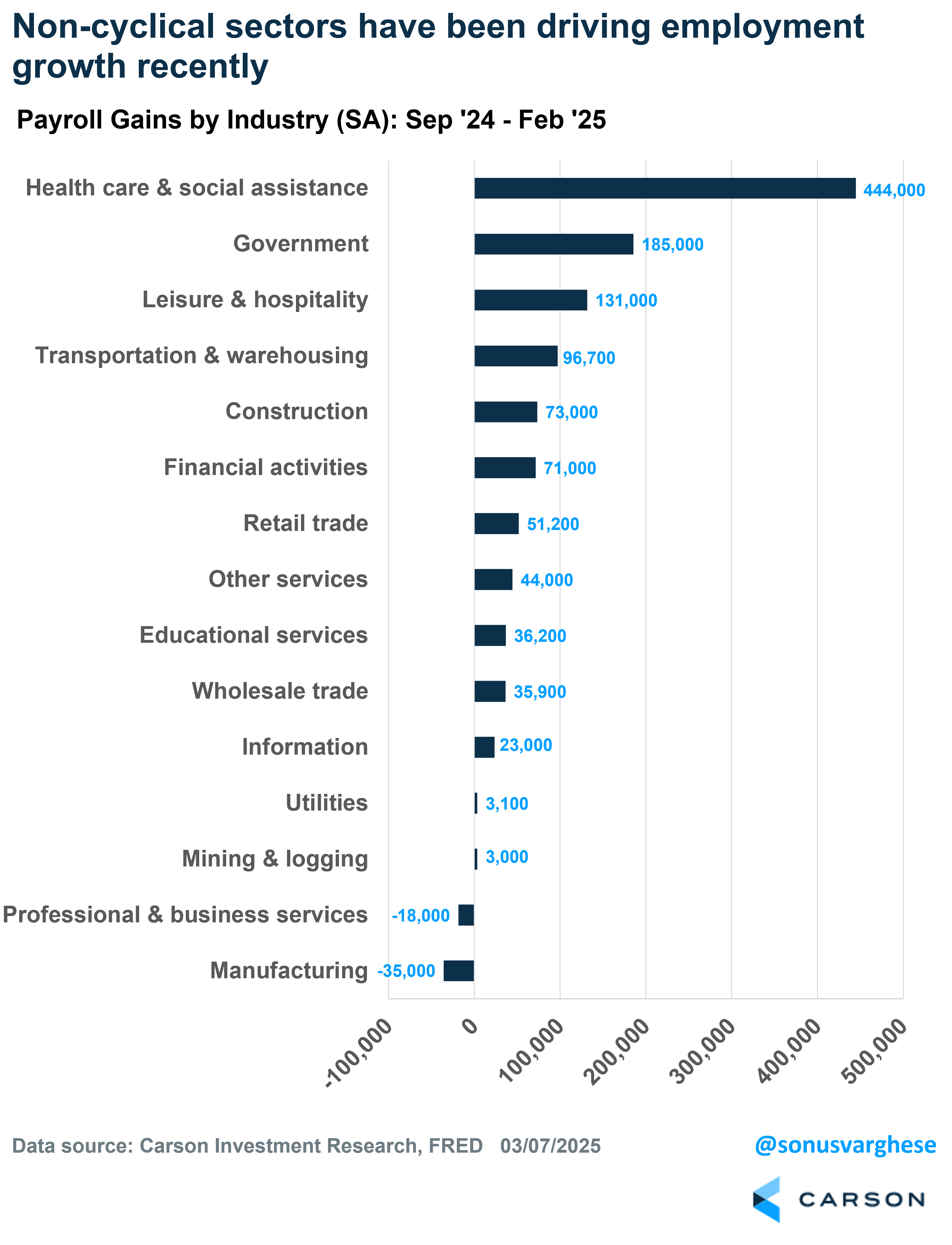

The support from non-cyclical areas of the economy in February continues a theme we’ve seen over the past six months to a year. Over the past six months, payrolls have grown by 1.14 million, of which health care and social assistance accounted for 39% (+444,000) and government accounted for another 16% (+185,000). The cyclical economy wasn’t completely dead, with another 26% of jobs created within the leisure and hospitality, transportation/warehousing, and construction sectors. But these were partly offset by a loss of 35,000 jobs in manufacturing and 18,000 lost jobs in professional and business services. Not what you want to see if you’re looking for an acceleration in economic growth.

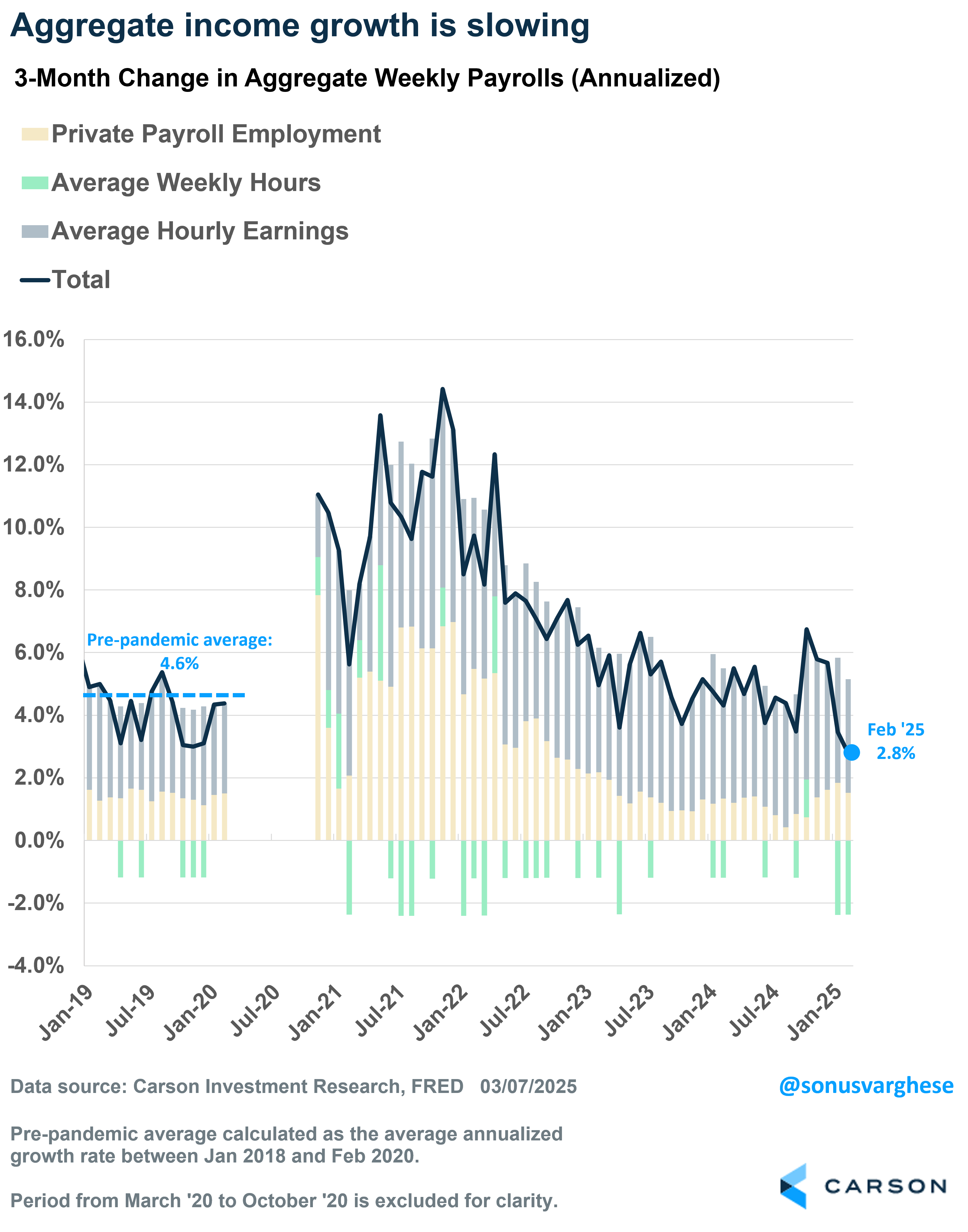

Ultimately, what matters for the economy is aggregate income growth across all workers in the economy, since that’s what drives consumption. That’s a combination of employment growth (running ok), wage growth (strong), and hours worked (weak). Aggregate income growth has slowed to a 2.8% annualized pace over the past 3 months. That’s an alarming slowdown on the face of it, but it’s partly driven by a drop in hours worked due to weather-related issues over the past two months, which will likely reverse soon. Again, this is not recessionary, but income growth is likely running well below the 4.5 – 5% pace we saw last year.

Of course, the question on everyone’s mind is tariffs. I wrote an extensive piece earlier this week on tariffs, and its potential impact on the economy, markets, and our general outlook in the face of this threat. As I wrote there, it’s hard to gauge the precise impact of these tariffs. For one thing, we don’t even know what the tariffs will be. But therein lies the uncertainty.

The largest, and perhaps adverse, impact of the tariff overhang is that it keeps the Fed waiting on the sidelines for longer before continuing with rate cuts. Elevated rates are clearly hurting parts of the economy, but the Fed doesn’t look ready to provide relief anytime soon—they’re going to want to wait to see what happens with tariffs. The Fed would likely act sooner rather than later if they thought the labor market was deteriorating, but the February data tells us that’s not the case. That takes away any urgency for further rate cuts. But that also raises the probability of something actually breaking before they act. (I’ll note that the housing market in particular is not going to function well with near 7% mortgage rates.) It comes back to the biggest risk we highlighted in our 2025 Outlook, the risk of interest rates staying too high, which could cause a break in the cyclical economy that drags everything else lower. There’s also a risk that the big drivers of recent employment gains (health care and state/local governments) start to see headwinds amid federal government cuts that result in less money being sent to the states (including for Medicaid, particularly in rural areas).

Ryan and I talked about the “growth scare” on our latest Facts vs Feelings podcast. Take a listen below.

For more content by Sonu Varghese, VP, Global Macro Strategist click here.

7718871.1-0325-A