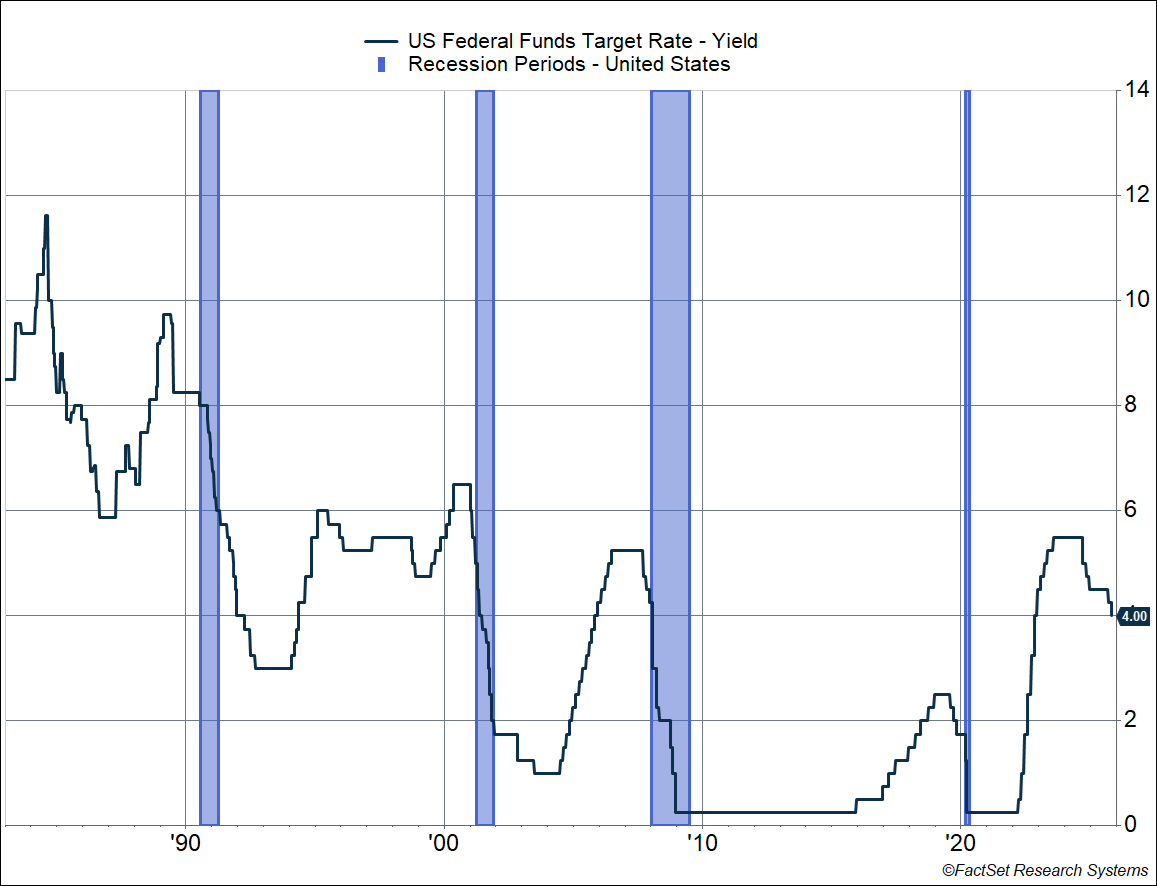

The Federal Reserve (Fed) cut rates by 0.25%-points at their October meeting, as expected. The target federal funds rate is now in the 3.75–4.50% range, 1.5%-points below the peak of this cycle, and the second cut in consecutive meetings. The chart below shows the upper end of their target. This is now the largest set of cuts we’ve seen outside of a recession since the mid-1980s. Even in the 1995–1999 period, the Greenspan Fed only cut rates by 1.25%-points (though they raised it by 0.25%-points in 1997). But keep in mind that this is following the most aggressive rate hikes since the 80s.

We’re in the dark with respect to economic data because of the shutdown, and so the status quo from the Fed’s prior meeting held:

- Economic activity is now expanding at a moderate pace, versus a slowdown in the first half of 2025, mostly on the back of strong consumer spending and business investment.

- The labor market is cooling, slowly. Job growth has slowed this year, and the unemployment rate has edged up but has remained relatively low. Private data is consistent with the low hiring/low firing economy, and the Fed believes lower labor supply due to immigration and lower labor force participation is leading to the slowdown.

- Inflation has moved up from earlier this year and remains “somewhat elevated” (more on this below).

It’s honestly a bit of a mixed picture if you’re a policymaker and that is leading to differing views within the committee. In fact, we got two dissents (out of 12 voting members):

- Governor Stephen Miran, former chair of the White Council of Economic Advisors (and currently “on loan” from his White House role), wanted a 0.5%-point cut, staying consistent with his dissent from September.

- Kansas City Fed President Jeff Schmid preferred not to cut at this meeting.

A Dovish Bias

As I noted above, the Fed has now cut rates by 1.5%-points since the peak of this cycle, including two cuts at the most recent meetings. In his press conference, Fed Chair Jerome Powell pointed out that downside risks to the labor market remain elevated, especially with slow job growth.

Inflation is certainly elevated, but Powell brushed it away. In fact, he noted that most measures of expected inflation are consistent with their 2% target. He acknowledged that core goods prices had increased due to tariffs, but that’s expected to be a one-time increase in the price level, rather than something that’s persistent.

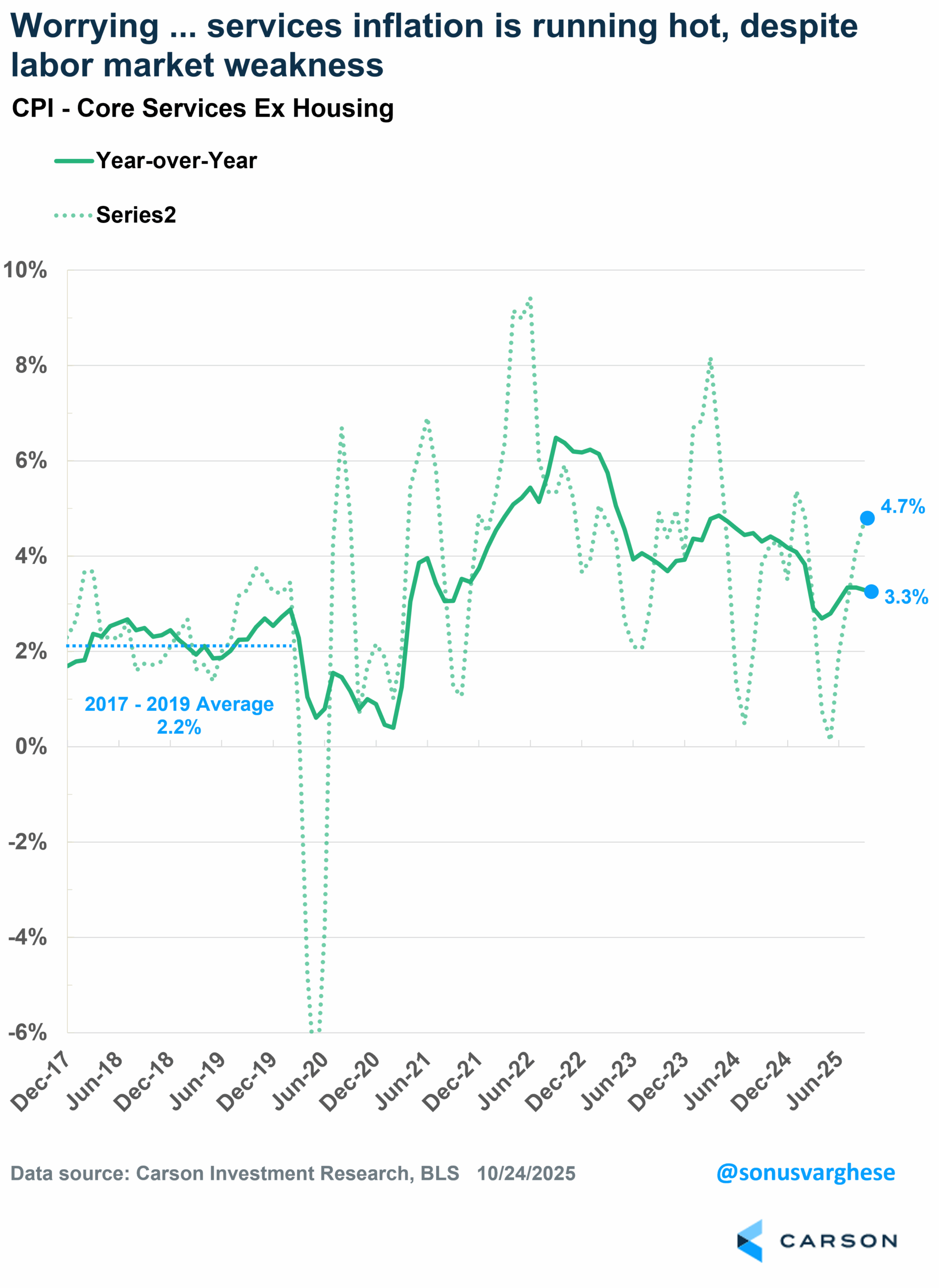

The good news is that housing inflation is easing and expected to continue. However, core services ex housing inflation is moving sideways. Powell argued that this is mostly being driven by “non-market services” (like financial services, which depend on things like stock prices). I would say that core services is quite elevated and well above normal, including services like personal care services, day care/pre-school, pet services, etc. There’s a reason why CPI for core services is up over 4.5% annualized over the last three months, and running above 3% over the past year (see my prior blog).

Putting all of this together, Powell said that inflation is running close to their target of 2%, once you exclude tariff-impacted core goods and “non-market based” core services. Admittedly, that is quite a few cuts to the inflation number. (As someone online joked, inflation ex-life is 0.)

Still, what Powell says is what matters and the reality is they’re cutting rates while inflation is elevated. Powell explicitly said risks to the two sides of their mandate (inflation and employment) are now balanced and as a result “policy needed to be roughly at neutral” Instead of modestly restrictive.

I’d say the outlook for policy remains dovish just based on the picture Powell laid out. This could shift if we get data showing the labor market is in a much stronger place, but given the shutdown it looks like we’re going to be in the dark on official government data for a while longer.

Furthermore, Powell didn’t seem worried that lower interest rates would further accelerate the AI investment boom. He said that AI investments, like data centers, are not interest rate sensitive, unlike other sectors of the economy. Investment in the AI space is driven by longer run views, including expected demand for AI workloads.

Powell Refuses To Be Pinned to a December Cut

Despite the dovish outlook, and dovish actions, Powell explicitly refused to be pinned down to another cut in December. In fact, he looked to be playing up the divisions within the committee, and when asked about a rate cut in December, he pointedly said that a rate cut in six weeks was not a “foregone” conclusion.

Powell repeatedly mentioned “strongly differing views” within the committee when it comes to continuing to cut, saying:

There’s a growing chorus now of feeling like maybe this is where we should at least wait a cycle, something like that or some part of the committee. It’s time to maybe take a step back and see whether there really are downside risks to the labor market, or see whether, in fact, the stronger growth that we’re seeing is real.

The problem is we’re likely not going to get much data between now and the Fed’s December meeting to meaningfully assess where the labor market is. My sense is that Powell needed to acknowledge the hawks on the committee who are worried about cutting into an economy that seems to be rebounding from a poor first half. Note that the September dot plot showed the median projection implying three cuts this year (a cut in December on the back of cuts in September and October).

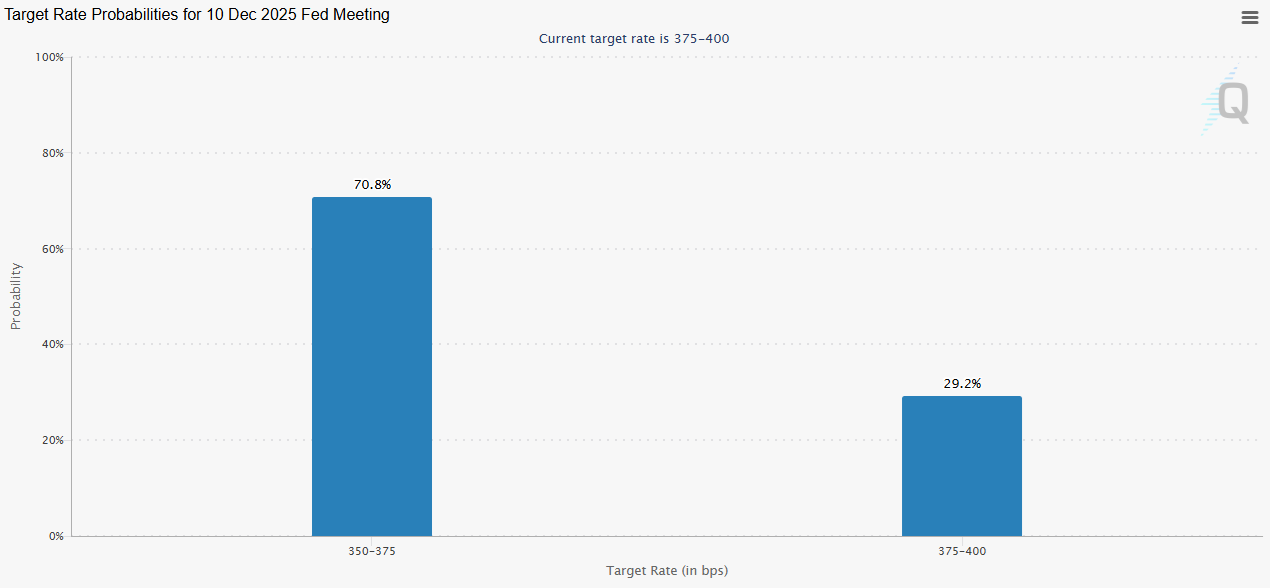

Investors were quick to reprice the odds of a December cut. The probability of another cut in six weeks fell from over 90% to about 70%.

Big Picture: More Cuts Are Coming, If Not Now Then Later

It’s notable that the odds of a December cut didn’t fall even further, closer to 50%. It’ll be interesting to see what Fed officials say over the next few weeks. Do most members continue pushing back against another cut, or do they clarify current market pricing and push the odds of a December rate cut back up over 90%? In the absence of economic data, there’ll be a more careful parsing of speeches by Fed officials.

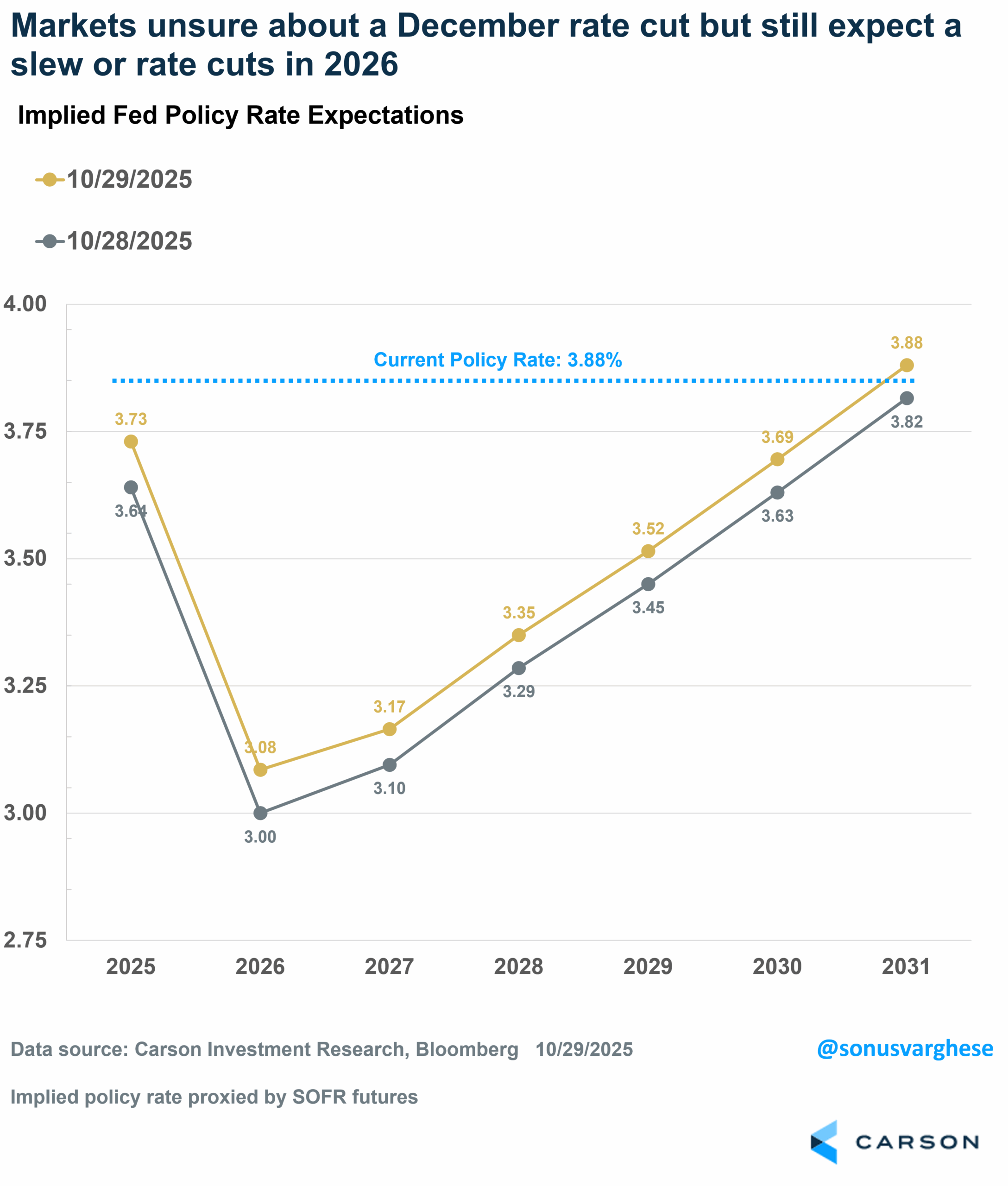

At the same time, markets still expect a near 3% fed funds rate at the end of 2026. So while there’s more uncertainty in the very near term, investors still believe the Fed is going to continue rate cuts next year. Some of this likely reflects Powell’s term ending next May, when President Trump will appoint a new Fed Chair who will push the committee to cut rates further, a la Stephen Miran.

As I mentioned above, even Powell seems to think that rates should be at neutral, i.e. 3%, when risks to both sides of their mandate are equal. Now if the labor market looks stronger, rate cuts could get pushed out but that’s not necessarily a bad thing. But the big picture is that we’re likely to get more rate cuts—if not in December, then in 2026. and if not by a Powell-led Fed, then under a new chair. Ultimately, the rate cuts may have a downstream impact on more rate-sensitive areas of the economy (like housing and manufacturing). Combine that with the AI-side and we could be looking at an inflationary boom next year.

We believe this is going to be a tailwind for markets, in addition to the tailwinds of market momentum and positive seasonality (Ryan just wrote about this). We may also get tax cuts in the first half of 2026, and with the US reaching a trade truce with China, there’s less uncertainty around tariffs as well. To summarize:

- Don’t fight momentum – momentum begets momentum

- Don’t fight seasonality – as the chase to year end begins

- Don’t fight the Fed – more rate cuts may come, if not now then next year

- Don’t fight Congress – tax refunds in 2026 may put more money in people’s pockets

- Don’t fight the White House – and their desire to keep markets calm

Ryan and I talked about a lot of this on our latest Facts vs Feelings episode. Take a listen below:

For more content by Sonu Varghese, VP, Global Macro Strategist click here

8558943.1.-30OCT2025A