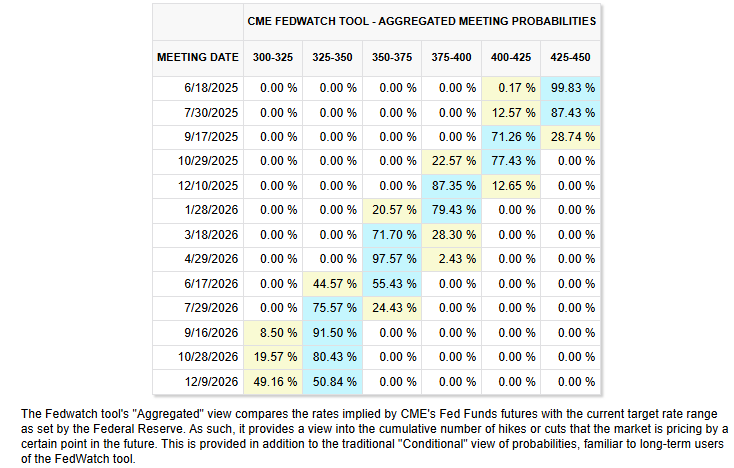

The Federal Reserve concludes its two-day policy meeting tomorrow and the market implied odds that they will not cut rates, via CME’s FedWatch tool is 99.83%. (I can’t help but hear “So you’re saying there’s a chance” in my head in reaction, but yes there’s a near zero chance of a cut since the Fed doesn’t like to surprise markets unless it’s really needed.) As you can see below, current expectations are for a cut in September and December and two additional cuts in 2026. That’s in line with Fed median projections when they were last presented in March. Outside clear signs of economic slowing, we think the market-implied view for 2025 may be too high and that one cut in 2025 is more likely, although let’s call it a range of 0 – 2.

Source: CME Group 6/17/2025

That actually places our currency policy expectations more hawkish than what we think the Fed should do given economic conditions. We believe the Fed should be a little more aggressive about cutting. That means little in itself; our job is not to propose policy. But it does play into our market views, as this means some added risk for the economy as well as potential for the market to be disappointed by the Fed not cutting as we move further into the year.

Why do we have that view? First, there are underlying signs that the economy is slowing (but not stalling) (see Sonu’s The Big Picture: The US Economy Is Losing Steam). We’re seeing damage in particular in cyclical areas of the economy, especially housing (see Sonu’s recent 11 Charts That Explain the Housing Strain) and small businesses. Yes, there is a massive stimulus bill that Republicans are aiming to pass by the end of the summer, but the full benefit of the bill’s deficit-financed economic (and profit) growth won’t fully kick in until 2026. That’s fine for markets, which are forward looking, and that by itself will likely provide the economy with an extra shock absorber, but it will still leave the economy somewhat vulnerable to an unexpected negative surprise in the near term.

At the same time, while the impact of tariffs on inflation still lies largely ahead of us, the disinflationary forces that we talked about in our Outlook 2025 have played out as expected and have been helping to keep inflation in check for now. The inflation outlook is still highly uncertainty, which is a self-inflicted would by the Trump administration, but we would still be biased toward protecting employment amidst a muddle-through economic outlook.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

By contrast, as we explained following the last Fed meeting (The Fed Is Buying Into the Tariff Bull Case, but That Pushes Out Cuts), policy uncertainty and the broad economic environment are leading the Fed to prioritize price stability over maximum employment, and that will likely leave them on hold until they have clear evidence the economy is in trouble, which probably means they’ll cut too late if trouble comes. The Fed’s gamble right now is a bias toward optimism on the employment side, which it believes gives it space to see how policy uncertainty plays out. (Powell has specifically mentioned policy uncertainty around trade, immigration, fiscal policy, and regulation with an emphasis on trade as the most salient risk.)

In a funny way, the Fed’s action is fully aligned with President Trump’s assessment of the economy, even if the president’s policy prescription is different. If you listen to the president, we’re on the verge of the best economy the country has ever seen. At the same time, no president has ever been more effective at taking down inflation. If the president’s assessment is correct, those are powerful outcomes, but they also imply that the Fed should probably … raise rates or at least not lower them. As I said, not the president’s takeaway, but the by-the-book approach to monetary policy is that a great economy with low inflation caller for higher rates.

Also keep in mind that the economy under President Biden was powering through at nearly 3% real growth over the last 2 ½ years of his term despite the highest interest rates since before the Great Financial Crisis. We give Biden little to no credit for that, but still, it would be an embarrassment if Trump could not at least match it under similar conditions. In our 2025 Outlook we even said that with thoughtful, reasonable implementation of the president’s policy priorities, an outcome like that was entirely plausible.

Unfortunately, “thoughtful and reasonable” turned out to be too lofty an expectation and America continues to watch in wonder as both major parties seem to flee being the party of American prosperity, thinking Americans are hungrier for a made-for-social-media tribal battle of ideological pouting than for a pragmatic approach to making Americans’ lives better.

Trump’s actual interest rate prescription is that that Fed should cut rates a full percentage point, a recommendation that usually implies that underneath the surface the economy is in a doom cycle, although that’s certainly not the president’s reasoning. Let’s try to translate, since the president has a tendency to exaggerate for effect (and often as a negotiating stance) even when it might appear ridiculous. Let’s imagine that Google added Trump Translate to its suite of translation tools to help avoid cultural misunderstanding and forestall Trump Derangement Syndrome.

It would work something like this. In general, any time Trump says a number, Trump Translate will use advanced AI to extract the idea stripped of rhetoric. That will usually result in a translation that’s ¼ to ½ the pronounced value, although sometimes as low as 1/10 or lower (see Doge). Using Trump Translate on his Fed comments, the actual intent was probably that the Fed should cut 0.25 – 0.50% now (after all, the initial cut of this cycle was 0.50%) and more later since the economy is doing ok but could use some help. He has also said rates should be near zero, but if I put that through Trump Translate it would probably come out as 2 – 3%, lowering rates to a level that the Fed would consider unambiguously accommodative (which is about halfway from where we are now). I think that works. In fact, if we had only had Trump Translate on Liberation Day, we would have known that tariffs would probably land around 15% and the market reaction likely would have been less volatile.

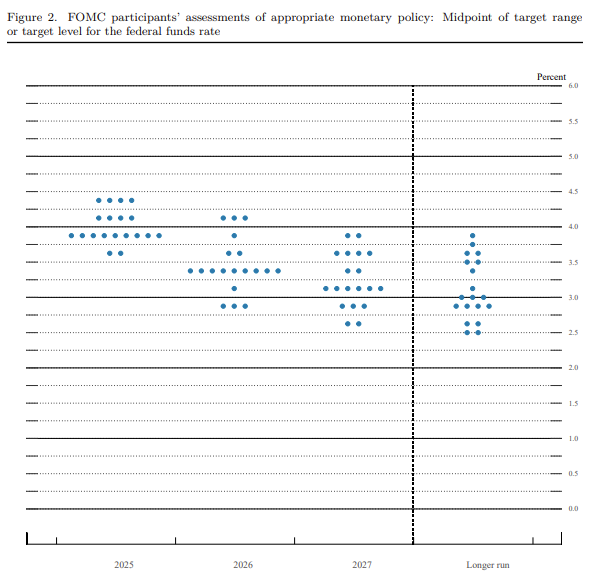

Where does that put us? With a cut tomorrow basically off the table, the focus will be on Fed Chair Powell’s press conference and the Summary of Economic Projections (“SEP”) that are released every other meeting (last release March 19). The SEP includes interest rate projections (commonly referred to as the “Dot Plot” since each projection is represented by a dot) as well as some major economic variables and an assessment of risks. (The last dot plot from March is below.) The SEP is based on individual forecasts by the participants in Federal Open Market Committee (“FOMC”) meetings. When all positions are filled, that includes the seven members of the federally appointed Board of Governors and the 12 presidents of the regional Federal Reserve Banks. Of those 19, 12 are voting members at any given time (all of the Board of Governors, the president of the New York Fed, and four of the 11 remaining regional bank presidents on a rotating basis), but all 19 participate. Markets usually take their bearings from the median value, but that’s not really a consensus forecast, since the individual forecasts are usually widely dispersed, just the forecast that happens to sit in the middle.

March 19, 2025 Dot Plot:

Source: Federal Reserve accessed 6/17/2025

In general with the SEP, additional economic weakness (growth and labor market expectations) should bias us toward more cuts; any rise in inflation expectations should bias us toward fewer. (And vice versa on both.) We expect the new SEP to reflect the Fed’s current dilemma even more intensely, with risks to both inflation and employment both increasing. The last SEP preceded both Liberation and the first reading on Q1 GDP. As a result, inflation expectations are likely to edge higher while growth expectations are expected to edge lower. That will likely leave the dot plot at two cuts this year and another two cuts next year, which would bring rates down to a target range of 3.25 to 3.5% at the end of 2026, above the long-run expected median or neutral rate of 3.0%, but equal to or lower than the long-run neutral rate for 7 of 19 members.

Overall, we expect markets to be looking for any ray of sunshine in the Fed’s brief policy statement, Powell’s press conference, or the SEP and potentially to overreact. At the same time, we expect Powell to stay evenhanded and maintain current messaging (with perhaps an added caution that the conflict in the Middle East is adding to the uncertainty). Finally, expect the president to react to the outcome with his usual grace, but don’t forget to put it through Trump Translate. But more than anything, expect everyone to be thinking about the July meeting, when we will have more data and more insight on how policy is evolving.

8084610.1.-06.17.25A

For more content by Barry Gilbert, VP, Asset Allocation Strategist click here