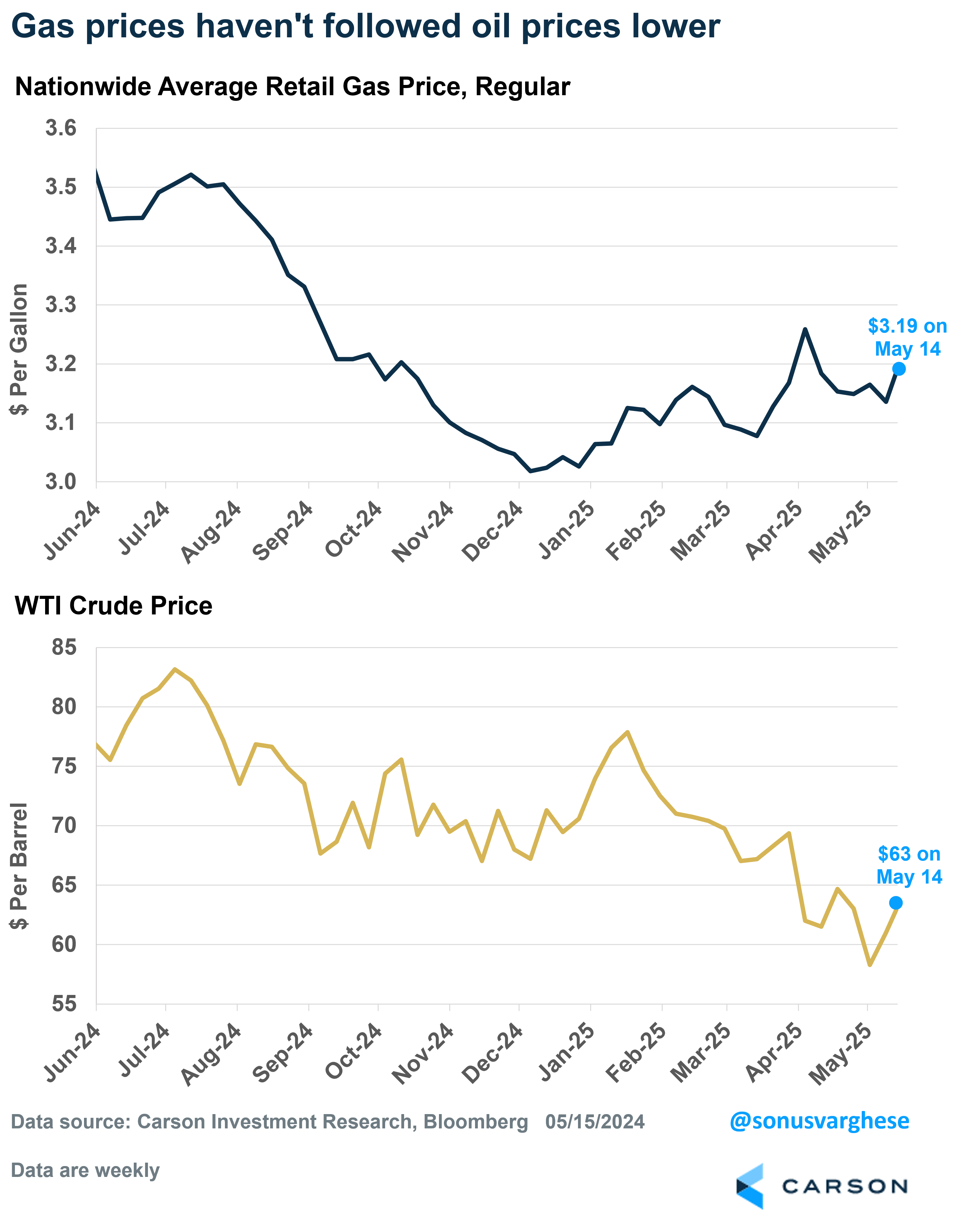

Oil prices have collapsed in recent months, with WTI crude oil prices now closer to $60/barrel after hitting $80/barrel in mid-January. Prices are down over 10% from the beginning of the year, and over 20% from peak levels in January. Normally, you’d think this would translate to lower prices at the pump. But that’s not been the case.

Nationwide, average gasoline prices are currently at $3.19/gallon, about 5% higher than where they were at the start of the year. You can see on the chart below how oil prices have fallen since January, but gas prices have gone the other way.

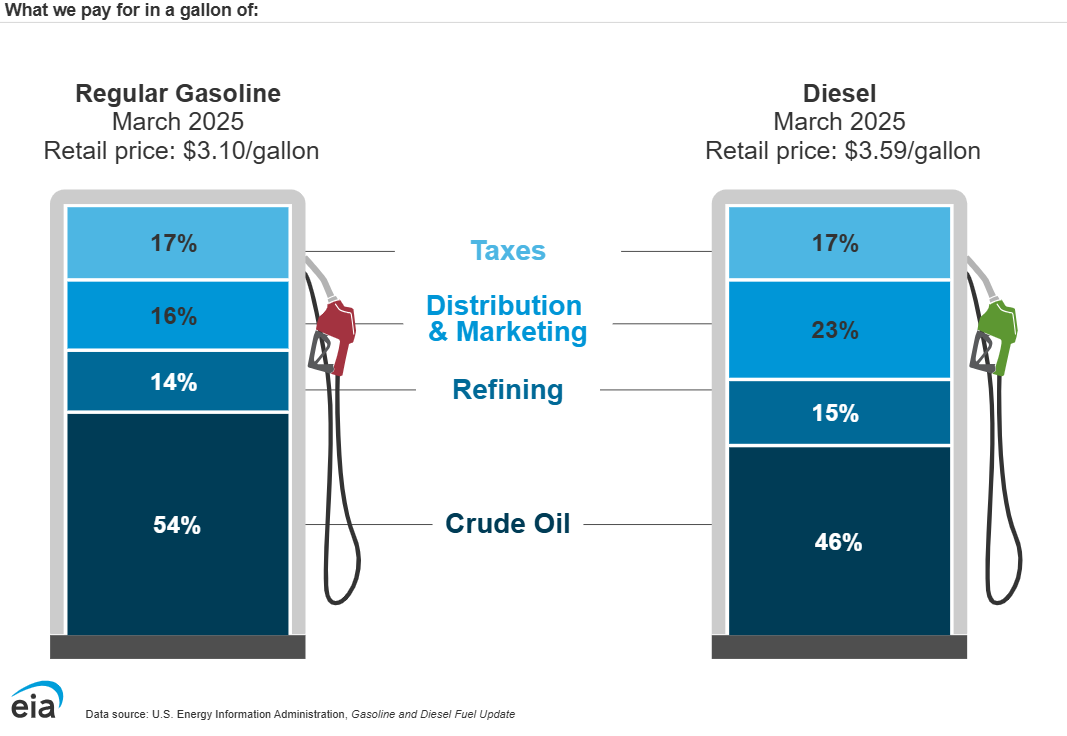

As it turns out, oil prices are not the only thing that determines gas prices, or even diesel prices. Another major factor (and a volatile one) is refining spreads, which is directly tied to refiners’ margins. Refining or “crack” spreads are the price difference between crude oil and refined product. Here’s a schematic from the Energy Information Administration (EIA) showing what makes up prices at the pump. Oil prices account for just over 50%, while refining spreads make up 15% of the rest.

Stay on Top of Market Trends

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today!

"*" indicates required fields

The chart below shows crack spreads for gasoline, and as you can see, crack spreads have surged recently. Crack spreads collapsed immediately after Liberation Day, amid recession fears and a potential collapse in gasoline demand. But it’s picked up sharply over the past month. Rising crack spreads are likely due to scheduled refinery maintenance, which turns off supply. But there could be some tariff impact here as well, with higher costs for refiners to maintain operations and keep supply humming. Higher crack spreads have more than offset the fall in crude oil prices, and this is another example of how tariffs may have already translated to higher costs for households.

Brace for More Energy Price Volatility, and Potentially More Pain

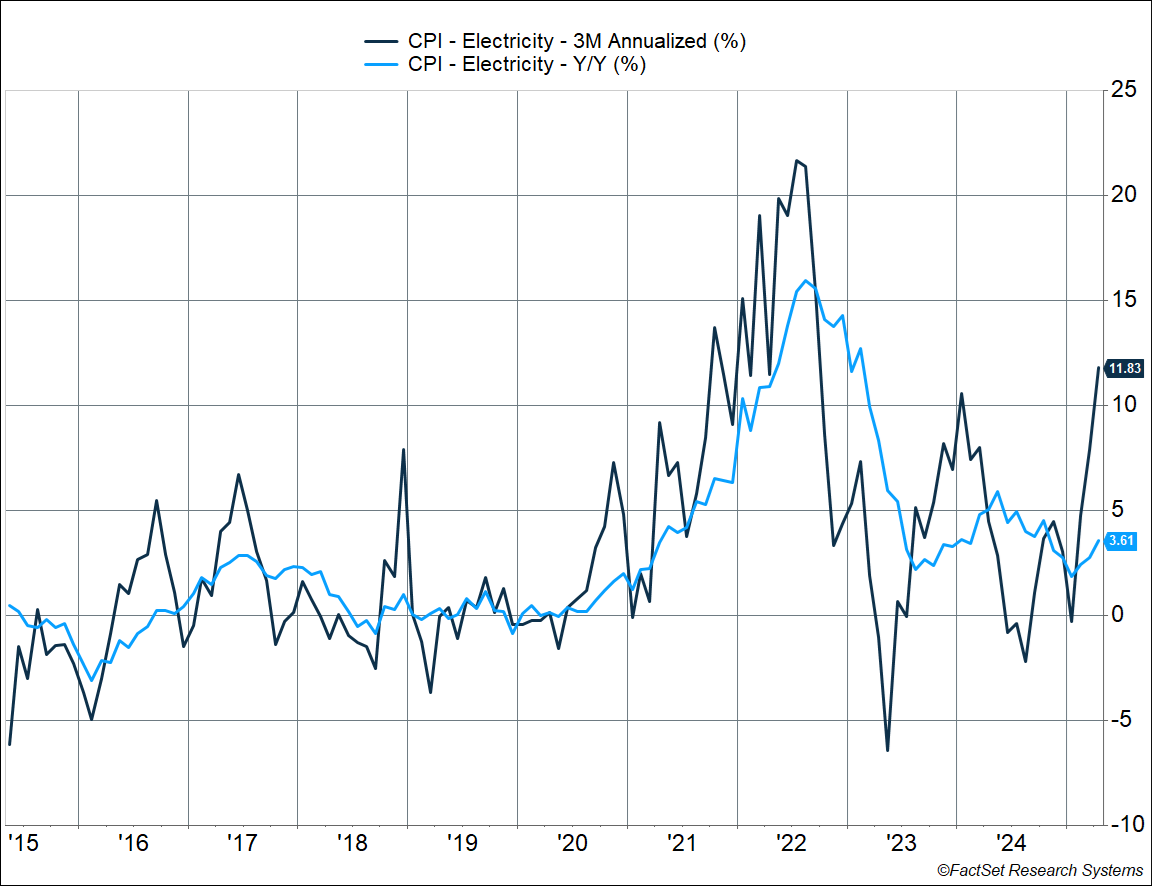

There’s a reason the Fed usually strips out energy prices from inflation data (along with food prices). Energy prices can be very volatile, especially oil prices, which are determined by global supply and demand — beyond what happens in the US. However, electricity prices have been relatively less volatile. But that may be changing.

Electricity prices within the Consumer Price Index (CPI) rose 0.8% in April, following a 0.9% rise in March and a 1% increase in February. Prices are up 3.6% since lats year, and up almost 12% annualized over the past three months. That’s the fastest three-month pace since 2022.

Meanwhile, utility prices (via piped natural gas) rose 3.7% in April, following a 3.6% increase in March and a 2.5% increase in February. That translates to a whopping 47% annualized pace over the last three months.

There’s potential for more trouble here. Via our friends at Employ America, as LNG exports and AI data centers surge, there’s much more demand for electricity along with pressure on supply for domestic use. The Inflation Reduction Act (IRA) actually went a long way towards satisfying these needs, beyond traditional sources of energy — including wind, solar, and even geothermal and nuclear. This wasn’t just a green initiative. The IRA was expanded sources of supply at a time of surging demand (and that demand is likely structural and not just temporary). If the IRA is gutted (which is a real possibility as per what the House has put forward in its tax bill), we could see persistently higher electricity prices. Also, as the Trump administration eases export controls on LNG, that leaves less supply here at home. Quoting the folks at Employ America:

“The U.S. can’t be a major gas exporter and keep electricity cheap unless we expand supply.”

Gutting the IRA, while increasing LNG exports, will leave American households susceptible to global gas price spikes. Australia found this out the hard way, as LNG exports surged, and power prices jumped because there were no protections for domestic supply.

If this indeed does happen, be prepared for a lot more inflation volatility — and CPI volatility does tend to be driven by energy, its most volatile component, anyway. Except now, in addition to volatile motor fuel prices, it’ll also be volatile electricity prices.

This has significant implications beyond higher energy costs for households (and businesses). Higher inflation volatility means the Fed is likely to keep policy rates elevated, which means interest rates will be higher for longer. That means the cyclical areas of the economy, especially housing, are not going to see any immediate relief from interest rates. Higher inflation volatility also has portfolio construction implications. It means you shouldn’t expect bonds to zig when stocks zag. There’s a reason we’re choosing to diversify our diversifiers using asset classes like managed futures — both in our shorter horizon tactical portfolios and in our longer-term strategic portfolios.

My colleague, Carson VP Asset Allocation Strategist Barry Gilbert, recently wrote about what we saw in the last month amidst the near bear market . Intermediate Treasuries worked as a (modest) diversifier over the past month when stocks collapsed. This was because recession odds surged (implying a deflationary environment). However, you don’t want to rely on Treasuries as your single source of diversification in a portfolio, especially going forward. As Barry wrote, it’s important to understand what environment you’re in, and if the environment is uncertain, as we think the current one is, having exposure to different kinds of diversifiers can be beneficial.

Ryan Detrick, Carson Chief Market Strategist and I talked about the cancellation of Liberation Day, where tariffs stand now, and potential implications for Fed policy, on our latest Facts vs Feelings episode. Take a listen below:

For more content by Sonu Varghese, VP, Global Macro Strategist click here

7973466.1 – 5.15.25 A